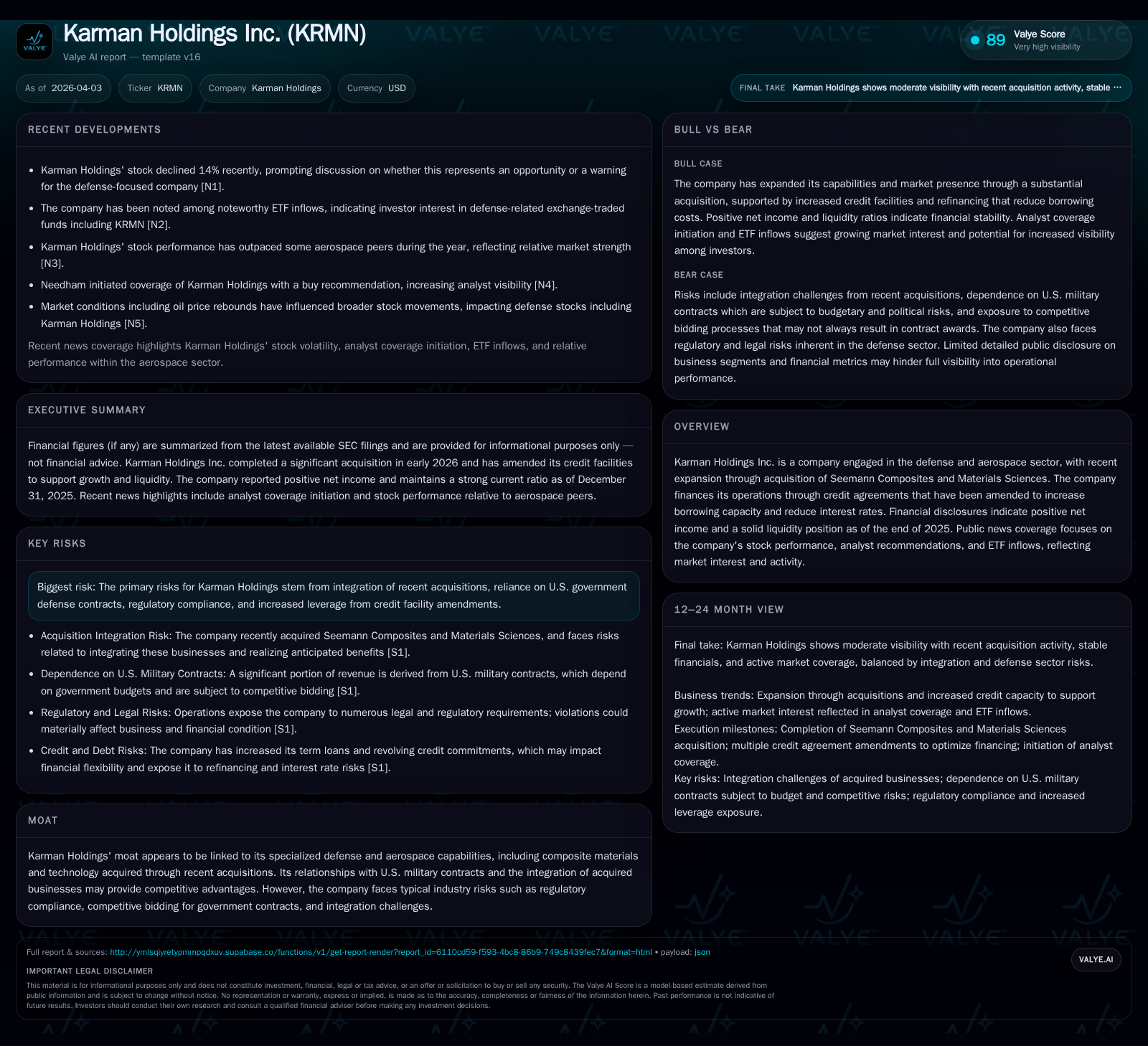

Karman Holdings Inc. Strengthens Defense Core Through Strategic Acquisitions and Credit Refinancing

The company enhances its aerospace composites capabilities and financial flexibility following a $220 million acquisition and multiple credit facility amendments.

Karman Holdings Inc., active in the defense and aerospace sectors, marked 2025 with a transformative acquisition of Seemann Composites and Materials Sciences for approximately $220 million, amplifying its composites technology portfolio. Corresponding amendments to its credit agreements lowered borrowing costs and expanded liquidity, supporting this strategic expansion. Fiscal 2025 saw solid growth in operating and net income despite a notable shift to negative operating cash flow amid increased capital expenditures. Market analysts have upgraded their outlooks, reflecting confidence in Karman's evolving competitive position, though integration risks and government contract dependencies remain key challenges.

Transformative Growth: Acquisition of Seemann Composites and Materials Sciences

In December 2025, Karman Holdings entered into an agreement to acquire Seemann Composites, LLC and Materials Sciences LLC for a combined consideration of approximately $220 million—$210 million paid in cash plus $10 million in company stock, subject to adjustments [S13][S16]. The closing occurred in early February 2026, expanding Karman’s foothold in high-performance aerospace composite materials that serve critical defense applications. This acquisition strategically deepens the company's differentiated capabilities amidst growing demand for lightweight, durable materials integral to modern military platforms.

The deal adds proprietary composite technologies that integrate with Karman's existing U.S. military contract portfolio [N4]. The acquisition complements its core aerospace segments by advancing materials science expertise aligned with defense industry trends favoring technologically advanced components such as radar-absorbing substrates or enhanced thermal management composites. The company's disclosures underscore deliberate focus on capturing operational synergies from this vertical integration [S1]. Yet they also candidly flag typical sector-specific risks related to integrating distinct corporate cultures and systems which could temporally moderate expected benefits [S4][S5].

Historical Financial Performance: Revenue, Profitability, and Cash Flow Trends

Karman’s fiscal year 2025 results reflect significant earnings growth but also reveal underlying cash flow constraints tied primarily to increased capital investment accompanying the acquisition phase.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 17 | -22 | 73 | 20 | +36.7% |

| 2024 | 13 | 27 | 64 | 15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | -42 |

| 2024 | 11 |

Source: SEC companyfacts cache [F1].

Operating income rose robustly by nearly 15%, driven likely by higher margins resulting from both organic defense contract growth and initial contributions from acquired entities [F1]. Net income outpaced operating income growth—up almost 37%—suggesting effective cost control or favorable non-operating items.

However notable is the stark reversal from positive operating cash flow in FY2024 ($26.6 million) to a negative $22.1 million in FY2025. Elevated capital expenditures (+33%) signal investment into facilities or technology necessary for scaling composite production post-acquisition [F1]. This increase caused free cash flow (operating cash flow less capex) to turn negative at roughly -$42.5 million—an important metric indicating funding needs beyond operational earnings.

Liquidity remains solid as reflected by the current ratio of approximately 3.29 (current assets $291 million vs liabilities $88.7 million), suggesting short-term obligations are well covered despite cash flow pressures [F1].

Evolving Capital Structure: Credit Agreement Amendments and Leverage Implications

Karman has proactively reshaped its capital structure to fund acquisition-driven expansion while optimizing borrowing costs.

In February 2026’s Third Amendment to its credit agreement dated April 2025 (already modified twice before), the company refinanced approximately $503 million of existing term loans reducing interest rates by a substantial seventy-five basis points — aligning term loan pricing at SOFR plus 2.75% [S10][S12]. Concurrently it upsized term loans by an additional $265 million — swelling total principal availability to approximately $768 million — providing funding liquidity for the Seemann acquisition alongside working capital needs and transaction fees [S10][S13][S16].

March’s Fourth Amendment further extended financial flexibility by boosting revolving credit commitments from $50 million increment caps previously capped at total commitments of $50 million up to now an uncapped amount totaling $150 million overall revolver capacity [S11][S28]. This removal of fundraising ceiling anticipates future liquidity needs amid acquisition-related outlays.

This restructuring enhances Karman’s leverage capacity critical given seasonality and lumpy defense contracting revenue streams; however it elevates funded debt levels significantly implying increases in leverage ratios—as disclosed within their filings—that will require careful management relative to EBITDA generation going forward [S8][S29]. The lower SOFR spread refinancings mitigate some interest expense impact but overall leverage remains an area investors need to monitor closely amid ongoing operational scaling.

Future Growth Drivers and Integration Challenges Post-Acquisition

Operationally the newly acquired composites businesses align with expanding U.S. military platform modernization efforts requiring advanced materials solutions embedded within next-generation aircraft and missile defense systems [S1][N4]. These enhancements complement Karman’s existing government contracting base which remains heavily weighted toward U.S. Department of Defense spending mandates.

Growth will stem both from leveraging proprietary composites technology into new program awards as well as cross-selling opportunities within Karman’s broader portfolio including avionics and electronic warfare subsystems [N1][S5]. Yet these prospects are tempered by acknowledged risks inherent in large-scale integrations such as disparate ERP system harmonization delays or cultural integration friction which could temporarily disrupt performance expectations or margin accretion pathways [S4].

Dependence on government budgets subjects Karman’s pipeline visibility to political appropriations processes impacting contract awards timing and scale—typical dynamics across the sector—but heightened here given concentration in few large customer programs [S5][N1]. Moreover regulatory compliance protocols relating to government contract audits impose ongoing compliance overhead.

Market Sentiment and Analyst Perspectives on KRMN’s Aerospace Positioning

Market commentary reveals growing investor interest fueled by analyst upgrades reflecting optimism around the acquisitions’ transformative potential.

Needham initiated coverage with a Buy rating explicitly praising synergy potential from composites incorporation into Karman’s industrial base [N4]. Similarly Piper Sandler upgraded their outlook citing improved competitive positioning versus aerospace peers evidenced by incremental revenue traction since acquisition announcement [N6]. ETF inflow data corroborates rising institutional participation focusing on defense subsectors such as XAR where KRMN holds weighting among select names [N2].

Stock performance through early Q1 2026 has outpaced select aerospace comparables pointing toward market validation of strategic moves despite short-term fiscal headwinds borne out from capital expenditure drawdowns highlighted prior [N3]. However some coverage notes caution due to the typical lumpy nature of aerospace supply chains amid geopolitical uncertainties affecting contract renewals [N1].

By balancing enthusiasm with rigorous scrutiny of execution risks investors appear pricing increasing confidence while maintaining guarded parallel vigilance toward delivery against announced milestones.

Capital Allocation Strategy: Dividends, Buybacks, and Return on Equity Dynamics

Karman’s approximate return on equity for FY2025 stands near 4.5%, derived by relating net income of roughly $17.4 million over shareholder equity figures reported [F1]. While positive ROE signals foundational profitability supportive of shareholder value creation ambitions under CEO Rambeau’s leadership tenure commencing March 2026 [S25], financial flexibility is tempered by free cash flow deficits intensified via an aggressive investment profile.

Recent SEC filings evidence modest dividend distributions accompanied by limited share repurchases underscoring conservative allocation given leverage considerations [S17][S18][S19][S25][S26][S27]. The firm appears prioritizing debt reduction capability alongside funding operational expansion over immediate capital returns—a common stance within mid-cycle consolidation phases particularly where technological asset bases are being integrated.

This approach reflects pragmatic stewardship aiming to optimize balance sheet strength against prevailing macroeconomic headwinds including interest rate environment sensitivity influencing overall cost of capital strategy execution.

Risks Intrinsic to Defense Contracting and Regulatory Compliance

Karman surfaces an extensive risk disclosure framework underscoring exposures fundamental across federally dependent contractors:

- Integration hurdles may delay realization of expected cost savings impeding margin improvement trajectories,

- Heavy concentration on U.S. Department of Defense contracts exposes revenue streams directly to budget fluctuations subject to congressional appropriations cycles,

- Competitive bid landscape remains intense necessitating innovative product advancement coupled with disciplined pricing strategies,

- Intellectual property protection challenges could restrict competitive positioning absent robust enforcement mechanisms,

- Legal proceedings disclosed involve typical contractual disputes or regulatory compliance audits that could impose financial or operational impacts if adverse outcomes materialize [S4][S5][N1],

- Regulatory complexity extends beyond procurement rules into environmental compliance associated with composite manufacturing processes requiring permanent vigilance [S14][S15].

These factors collectively complicate forecasting precision despite steady order book visibility articulated through official windows.

Key Performance Indicators to Monitor for Investment Assessment (Analysis)

Absent explicit forward guidance detailed within current disclosures or news releases,[N9] potential indicators merit close observation:

- Speed and effectiveness of the Seemann/MCS entities’ operational integration including production scaling timelines,

- Trajectory of leverage metrics following refinancing initiatives relative to adjusted EBITDA performance reflecting organic vs acquired growth mix,

- New contract awards especially multi-year program wins augmenting backlog stability amidst government procurement cycles,

- Quarterly analyst re-ratings or consensus estimate revisions tracking updated market sentiment surprises or disappointments relating to execution progress,

- Changes in cash flow dynamics particularly any inflection back toward positive free cash flow signaling capital expenditure normalization,

- Judgments stemming from ongoing/risk litigation developments potentially affecting legal contingencies exposure profiles.

Together these KPIs offer granular windows into whether Karman transitions successfully from acquisition-fueled expansion toward sustainable margin-enhanced growth anchored upon stable defense subcontract revenues.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments