374Water Inc.’s Strategic Struggle: Scaling AirSCWO Technology While Facing Financial Headwinds

374Water confronts steep commercialization challenges and financial pressures as it seeks to leverage its proprietary AirSCWO technology in hazardous waste treatment.

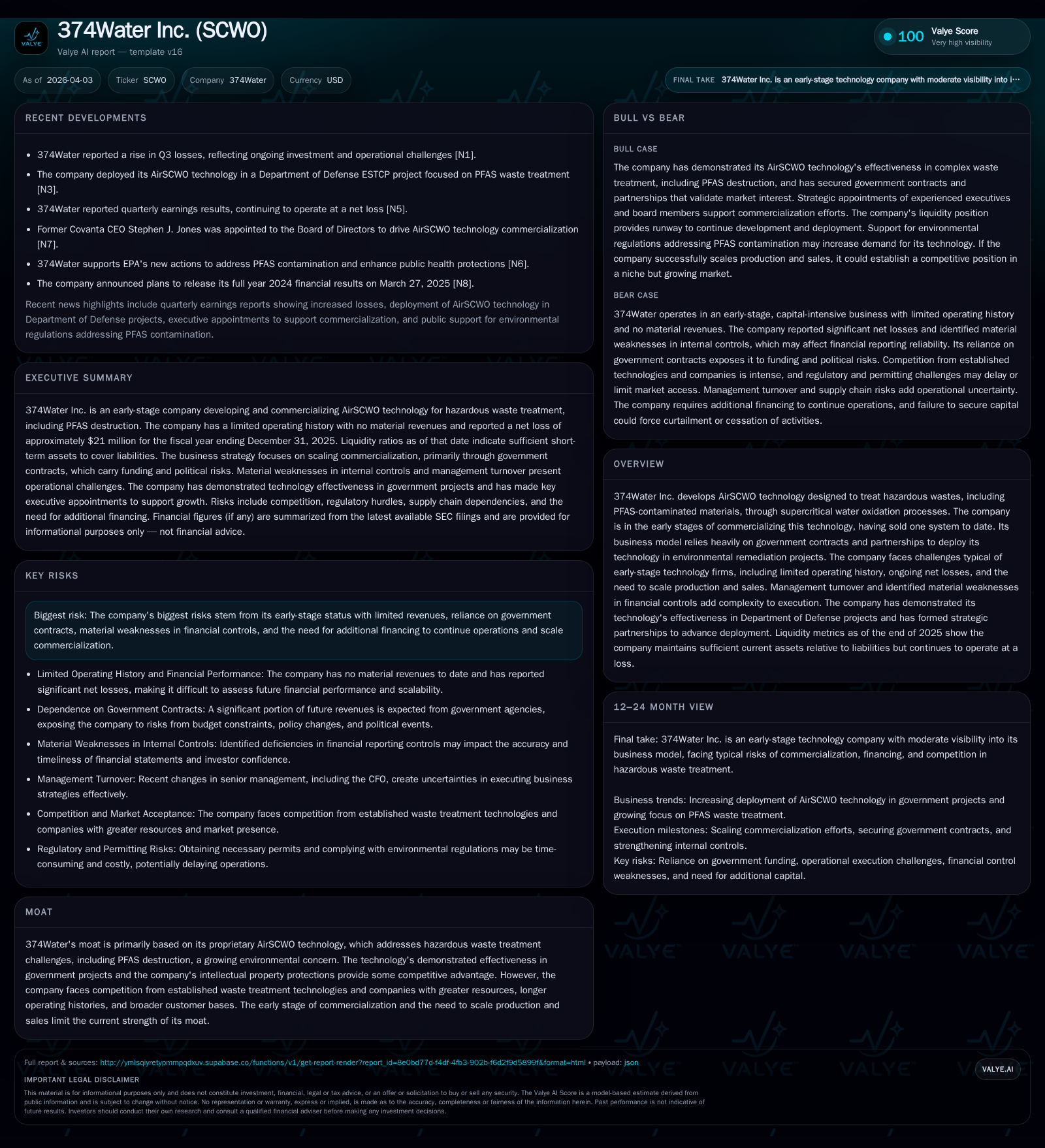

374Water Inc., developer of the disruptive AirSCWO supercritical water oxidation platform for hazardous waste, remains in early commercialization with minimal revenues and mounting losses. Despite demonstrated efficacy in Department of Defense projects and a strong IP position, the company’s growth is constrained by limited operating history, management turnover, and material weaknesses in financial controls. Its financials reveal sharp revenue declines alongside soaring operating losses and escalating capital expenditures. Success hinges on navigating competitive pressure from entrenched waste treatment technologies and securing sustained government contracts to scale production and deployment.

From Innovation to Implementation: Tracing 374Water’s Growth and Revenue Trajectory

Since FY2022, 374Water Inc. has experienced a considerable contraction in revenues alongside escalating operating losses—a hallmark of many early-stage technology firms facing commercialization hurdles. The company’s revenue plummeted from approximately $3.02 million in FY2022 to just over $215,000 by FY2025, a steep decline of roughly 51.7% year-over-year [F1]. This severe top-line compression primarily reflects the nascent state of market acceptance as AirSCWO moves from demonstration toward full-scale commercial adoption.

Meanwhile, operating losses surged dramatically—expanding by approximately 65.2% in the latest fiscal year alone—to a net deficit exceeding $21 million in FY2025 [F1]. Such loss acceleration underscores intensive investment into technical development, pilot projects, and initial deployments typical of groundbreaking environmental remediation technologies.

The company's return on equity (ROE) stands negative at an extreme level (~ -311.9%), highlighting the fundamental disconnect between invested capital and profit generation at this juncture [F1]. Furthermore, operating cash flow worsened markedly with a year-over-year decrease of over 35%, reaching nearly -$14.3 million by FY2025 [F1]. Capital expenditures ballooned by over 240% during the same period, suggesting aggressive attempts to build production capacity and infrastructure for AirSCWO systems [F1].

This financial snapshot paints a picture of a firm investing heavily ahead of sustainable sales volumes while navigating an uncertain revenue ramp.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -21 | -14 | -21 | -51.7% | -68.7% |

| 2024 | 0 | -12 | -11 | -13 | -40.1% | -53.4% |

| 2023 | 1 | -8 | -9 | -9 | -75.3% | -72.8% |

| 2022 | 3 | -5 | -5 | -5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -16 | -311.9 |

| 2024 | -11 | -80.4 |

| 2023 | -9 | -54.9 |

| 2022 | -5 | -56.8 |

Source: SEC companyfacts cache [F1].

Note: YoY percentages represent change compared to previous fiscal year.

Decoding the Proprietary Edge: AirSCWO Technology and Market Positioning

At the heart of 374Water's value proposition lies its proprietary AirSCWO technology — an iteration of supercritical water oxidation tailored specifically for hazardous waste destruction including persistent organic pollutants such as PFAS (per- and polyfluoroalkyl substances). Through supercritical oxidation kinetics that operate at conditions above water’s critical point (~374°C and ~22 MPa), the technology facilitates rapid and near-complete mineralization of complex hazardous compounds into environmentally benign end products.

Notably distinct from traditional incineration or chemical treatment methods, AirSCWO operates with minimal harmful emissions due to closed-system processing under supercritical conditions, reducing secondary contamination risks , [S4]. The technology has demonstrated operational effectiveness through Department of Defense-sponsored projects underlining its suitability for treating military-related PFAS contamination—a sector experiencing heightened regulatory scrutiny globally.

Despite these intrinsic technological strengths protected by patents which contribute to creating barriers for replication or patent circumvention , AirSCWO competes against well-entrenched incumbent waste treatments such as anaerobic digestion (biodegradation), standard landfilling practices, thermal incineration, lagoon/spray-field methodologies, and chemical stabilization via lime additions [S4]. Competitors wield advantages encompassing deeper market penetration, broader client relationships across municipal, industrial, and governmental markets, established service frameworks, diverse financing schemes including project financing options unavailable to SCWO currently [S4].

Thus while AirSCWO addresses emerging environmental demands unmet by conventional means—especially around PFAS’s refractory nature—the market penetration will hinge on demonstrating scalable reliability coupled with cost competitiveness against legacy solutions.

Commercialization Challenges and Management Dynamics in an Early-Stage Firm

The transition from innovative concept to scalable commercial offering continues to challenge 374Water materially beyond purely technical domains. Recent executive churn including the departure of CEO Christian Gannon in October 2025 followed by interim leadership until new appointments early in Q1 2026 illustrates ongoing management instability [S27]. Accompanying this are identified material weaknesses within internal financial controls that compromise reliable forecasting accuracy—an issue that heightens investor scrutiny concerning governance quality [S1], .

Such governance vulnerabilities complicate operational planning especially as the Company attempts cost controls while expanding product deployments and managing third-party supplier ecosystems required for AirSCWO system assembly [S21]. Additionally, dependency on government contracts introduces further uncertainty given cyclic budgeting constraints at federal/state levels [S1]. The need for specialized permits for system siting limits geographic rollout velocity requiring considerable management attention [S6], compounding scalability challenges.

Failure to mitigate these organizational risks may delay key commercial milestones or increase capital outlays due to inefficiencies or compliance costs.

Financial Results Unpacked: Losses, Liquidity, and Capital Allocation Strategies

In detailed financial terms derived from audited filings up to FY2025 [F1], fiscal performance reveals deepening losses: operating income deteriorated to almost negative $21.15 million compared to prior years’ losses climbing steadily since FY2022 [$4.76 million] through FY2024 [$12.8 million] indicative of heavy R&D expenses combined with operational overheads not offset by meaningful revenue inflows.

Operating cash flow turned substantially more negative ($-14.3M), reflecting both low sales volume inflows plus working capital demands including inventory buildup for planned deployments [F1]. Meanwhile capex jumped sharply—over $1.9 million spent primarily on scaling manufacturing capabilities required to meet expected demand increases contrasted with under $0.6 million a year earlier—marking clear reinvestment geared towards commercial expansion efforts [F1], [S15].

No dividends or share repurchase programs are reported given concentrated cash burn needs; equity financing remains essential moving forward with limitations imposed by public float thresholds under SEC "baby shelf" regulations limiting ATM offerings size relevant at ~$39 million public float level as noted in annual disclosures [S25].

Capital structure risks are notable since inability to secure fresh funding beyond available reserves may compel drastic operation curtailments threatening viability absent timely contract wins or technology monetization ramp-up [S11], [S17], [S22].

Market Competition and Regulatory Barriers Impacting Expansion

Competitive dynamics feature intensifying pressure from incumbents employing mature technologies such as anaerobic digestion that enjoy entrenched client bases with recognized cost advantages along with flexible channel networks allowing bundling services [S4], [S8]. Moreover, competition also drives periodic pricing shocks risking margin compression once SCWO achieves broader market introductions.

Regulatory permitting emerges as a non-trivial hurdle impeding rapid geographic proliferation; acquiring land use permissions together with environmental operation licenses demands extended lead times often involving multijurisdictional governmental interactions causing deployment delays and elevated compliance expenses impacting project economics unfavorably during critical growth windows [S6], [S8], [S13].

Further legal exposures arise from potential product liability claims linked to defective operation or incomplete toxic substance destruction which could impair reputation plus trigger costly litigation settlements undermining investor confidence substantially jeopardizing future contract prospects without adequate risk mitigation frameworks implemented proactively [S10].

Outlook and Key Milestones: What To Monitor in SCWO’s Path Forward

Absent explicit forward guidance within recent disclosures or press announcements ([N#] none available), indicators worth close tracking include successful contracting progression primarily within government sectors where policy budgets currently favor PFAS remediation projects given heightened environmental mandates (, [S1]).

Interim management’s effectiveness stabilizing operations post-executive reshuffle remains critical whilst enhancements addressing material control deficiencies must be achieved expediently for credible financial stewardship signaling maturity necessary when courting institutional investors for capital raises ([S27]).

Technical milestones such as demonstration-scale multi-unit deployments validating modularity/scalability together with cost optimization initiatives targeting breakeven thresholds over short-to-medium horizons will signify transition from pilot-phase into repeatable commercial models ().

Expansion into regulated international markets will likely require surmounting delayed permitting processes along with establishing third-party vendor partnerships aligned with local compliance regimes ([S6]). These elements collectively frame essential milestones anchoring longer-term growth expectations.

Investment Implications: Balancing Opportunity Against Execution Risk

From a qualitative perspective synthesizing operational realities against financial dislocations suggests that while AirSCWO embodies strategically important environmental technology addressing increasingly urgent remediation demands notably targeting PFAS pollutants otherwise resistant to existing treatments (), near-term prospects remain encumbered by persistent execution risks including:

- Early-stage commercialization fatigue exemplified by substantial net losses,

- Dependence on government contracting environments vulnerable to shifting political budget priorities,

- Governance shortcomings raising transparency concerns,

- Competitive pushback from legacy incumbents with deeper resource pools,

- Regulatory permit procurement delaying footprint expansion,

- Financing prerequisite uncertainties compounded under dilutive pressures resulting from limited public float liquidity.

In this context, the pathway toward profitable sustainability is contingent not only on technical merit but crucially hinges on organizational fortification combined with successful business scaling capped by dependable capital access.

Disclaimer: This analysis is provided solely for informational purposes based strictly on publicly available data up to April 2026 without any recommendation regarding investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments