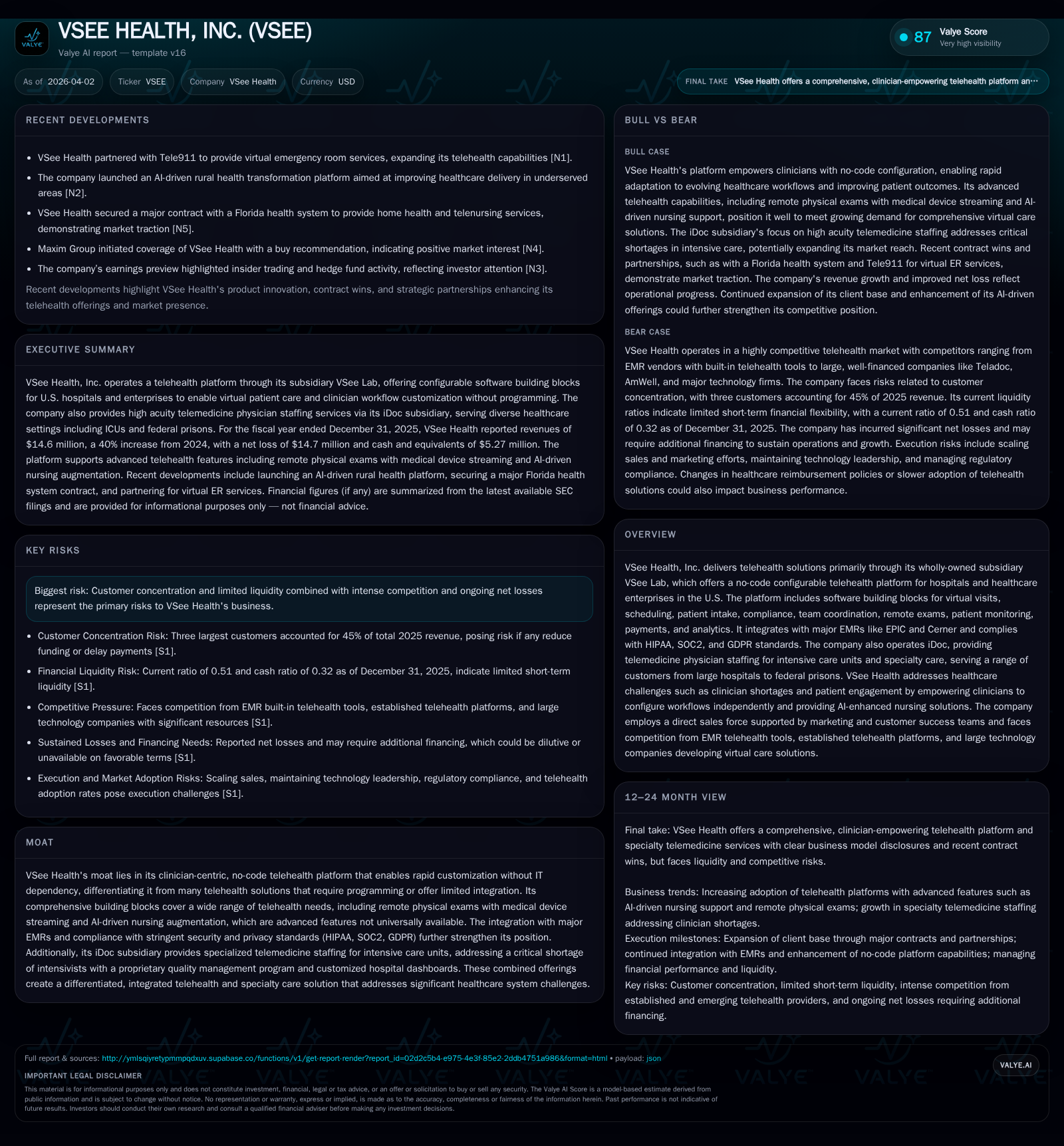

VSee Health Advances Clinician-Centric Telehealth Amid Intensifying Competition and Liquidity Pressures

VSee Health has delivered substantial revenue growth driven by its telehealth platform and ICU staffing services but continues to face sizable net losses and liquidity constraints.

VSee Health, Inc.'s growth over the past years hinges on the expansion of its no-code configurable telehealth platform (VSee Lab) and the integration of its high-acuity telemedicine staffing subsidiary iDoc. The company recorded a notable 40% revenue increase in 2025 largely fueled by iDoc's contribution, supported by growing demand for remote ICU physician services and virtual care. However, VSee remains unprofitable with persistent operating losses, raising solvency questions evidenced by substantial accumulated deficits and a current ratio below 1. Competitive pressures from entrenched EMR vendors, telehealth incumbents, and technology giants complicate VSee's market positioning. The company must balance investing in platform enhancements, scaling operations, and managing regulatory risks while navigating ongoing negative cash flow and concentrated customer relationships.

Company Overview

VSee Health, Inc. operates through wholly-owned subsidiaries VSee Lab and iDoc to deliver telehealth solutions across the U.S. healthcare ecosystem. VSee Lab provides a modular, no-code configurable telehealth platform designed primarily for hospitals and healthcare enterprises seeking flexible virtual care tools without extensive IT dependence. The software suite includes capabilities spanning virtual visits, scheduling, patient intake forms, compliance sign-offs, team coordination, remote exams enhanced by medical device streaming and AI nursing augmentation, payments integration including insurance processing, clinical documentation, and analytics dashboards. The platform supports integration with major electronic medical record (EMR) systems such as EPIC and Cerner via HL7 and FHIR standards while maintaining HIPAA, SOC2, and GDPR compliance.

Complementing these software offerings is iDoc’s specialized physician staffing services focused on intensive care units (ICUs), providing access to neurointensivists, cardiac intensivists, pulmonary critical care specialists among others. This addresses acute clinician shortages by remotely staffing high-acuity inpatient environments leveraging proprietary quality management programs customized to individual hospital workflows.

Historical Performance and Growth Drivers

VSee Health’s financial performance reflects a transition marked notably by the June 2024 acquisition of iDoc that materially contributed to revenue expansion. In FY2025, consolidated revenues grew to $14.6 million—up 40% from FY2024—driven predominantly by iDoc's surge in telehealth service volume ($2.9M) and patient fees ($2.2M), representing more than half of total revenues in 2025 [F1], [S19]. Subscription-based software revenues from VSee Lab declined about 22%, showing challenges in recurring enterprise client engagement.

Operating losses shrank sharply from $62 million in FY2024 to roughly $9.6 million in FY2025—a meaningful improvement indicating cost controls or scaling benefits but not yet breakeven profitability [F1]. Net losses narrowed by approximately 74% year-over-year to $14.7 million.

Cost of revenues rose strongly—more than doubling mostly due to increased personnel costs for physicians under iDoc contracts as well as cloud hosting and device expenses linked to HHS contracts held by VSee Lab.

Financial Summary Table

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -15 | -3 | -10 | 29928 | +74.5% |

| 2024 | -58 | -6 | -62 | 55267 | -1207.3% |

| 2023 | -4 | -1 | -3 | -36.1% | |

| 2022 | -3 | -1 | -4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -3 | |

| 2024 | -6 | ||

| 2023 | 7 | 36.0 | |

| 2022 | 110 | 43.7 |

Source: SEC companyfacts cache [F1].

Note: Operating Income = OpInc; Operating Cash Flow = CFO; all figures rounded.

Future Growth Prospects

Growth prospects hinge on several vectors:

- Platform Adoption: VSee Lab’s no-code telehealth platform aims to attract hospitals seeking flexible customization without reliance on IT departments—a key pain point among clinicians frustrated with rigid EMR built-in tools or costly custom software development [S7].

- iDoc Scaling: The intensivist shortage across hospital settings remains acute nationwide; iDoc’s model providing virtual ICU physician services taps into this scarcity with existing contracts typically renewed every two to three years potentially enabling recurring revenue streams [S6], [S14].

- Partnerships & Ecosystem Integration: Recent collaboration with Tele911 for virtual emergency room coverage could unlock new acute care markets beyond traditional ICU services [N1].

- Regulatory Tailwinds: Continued acceptance of telehealth reimbursement policies post-COVID may sustain volume growth but requires continuous adaptation given evolving state-level licensure requirements restricting remote supervision models or modalities [S8], [S13].

However, growth faces caps including customer concentration risks given reliance on few large clients accounting for close to half revenue recently [S15]; competitive encroachment from entrenched EMR vendors embedding their own telehealth functions; large telehealth platforms like Teladoc/AmWell; technology giants potentially deploying scale advantages; as well as internal limitations related to incremental customer acquisition costs increasing operational expenses.

Capital Allocation and Financial Returns

Capital allocation demonstrates priority toward growth investment amidst ongoing loss generation:

- Cash reserves stood at approximately $5.27 million at end-2025 against current liabilities exceeding $16 million—placing liquidity constraints front-and-center as the current ratio sits near 0.51 signaling short-term stress despite recent equity raises and convertible note financings reported throughout filings [F1], [S9], [S11].

- Operating cash flow remains negative though improved nearly 40% year-over-year at approximately -$3.4 million; free cash flow remains negative after modest capital expenditures (~$30k annually), consistent with SaaS norms rather than hardware-centric models.

- Share buybacks are negligible ($44), indicating no distribution focus while accumulated deficit totals exceed $82 million—highlighting ongoing capital consumption typical of emerging growth healthcare tech firms but limiting near-term returns metrics such as ROE despite an approximate calculated figure over 100%, which stems from negative equity distortions rather than sustainable profitability benchmarks.

Regulatory & Legal Environment Considerations

VSee Health operates within a highly regulated domain encompassing HIPAA data privacy requirements alongside complex federal/state fraud and abuse statutes such as Stark Law and Anti-Kickback Statutes governing referrals and reimbursement processes critical to its physician staffing business model [S5], [S8], [S20].

Additional considerations include:

- Compliance with FCC equipment authorization requirements for wireless medical devices involved in streaming medical data.

- Litigation exposure risks related to data breaches or malpractice claims inherent to telemedicine service provision.

- Increasing scrutiny from federal regulators could impose operational burdens or fines affecting financial performance adversely.

Industry Context Analysis

Telehealth adoption accelerated during COVID-19 but faces normalization pressures as payor policies tighten coverage criteria. Larger healthcare systems frequently develop proprietary or integrated EMR-based solutions eroding market share potential for third-party platforms focused solely on video conferencing. Nonetheless, comprehensive workflow configurability coupled with AI-driven features creates differentiation niches requiring ongoing innovation investment.

Similarly, acute care telemedicine services like those offered by iDoc compete with specialist providers initially hardware-focused but shifting toward integrated SaaS models emphasizing clinical workflow optimization.

Milestones & What To Watch

With explicit guidance sparse,[N1] future milestones include:

- Expanding integration footprint with additional EMRs or care networks transitioning from legacy video tools.

- Scaling client base beyond heavy concentration while sustaining contract renewals especially in ICU tele-staffing segments.

- Progression toward positive operating income through margin expansion driven by higher software subscription growth offsetting professional services costs.

- Managing regulatory risk mitigation transparently including compliance updates with state-specific telehealth laws or fraud investigations outcomes.

- Monitoring liquidity developments including equity financing capacity given current asset-liability imbalances.

Conclusion

VSee Health is an emerging health technology player positioned at the intersection of clinician empowerment through technology-enabled virtual care models amid systemic workforce shortages particularly intensivists nationwide. Its differentiated no-code configurable platform offers user-centered design advantages with strong back-end integrations addressing wide-ranging clinical workflows complemented by specialty acute care physician staffing under iDoc.

However, the company navigates challenges marked by intense competition from entrenched EMR vendors adding basic telehealth abilities through incumbent mature SaaS providers plus looming regulatory headwinds complicating provider licensing frameworks across states coupled with liquidity strains underscoring uncertain sustainability absent further capital infusions or rapid profit trajectory attainment.

Progress will be measured not only by topline expansion fueled chiefly through ICU services ramp-up but also ability to convert innovation into scalable margins while maintaining compliance and diversifying customer concentration risks over coming periods.

This memorandum is intended solely for informational purposes regarding VSee Health Inc.’s business operations based on publicly available data as of April 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments