LanzaTech’s Transition From R&D To Commercial Scale Faces Liquidity and Profitability Challenges

LanzaTech Global leverages proprietary gas fermentation technology to convert waste carbon into fuels and chemicals but remains burdened by recurring losses and capital constraints.

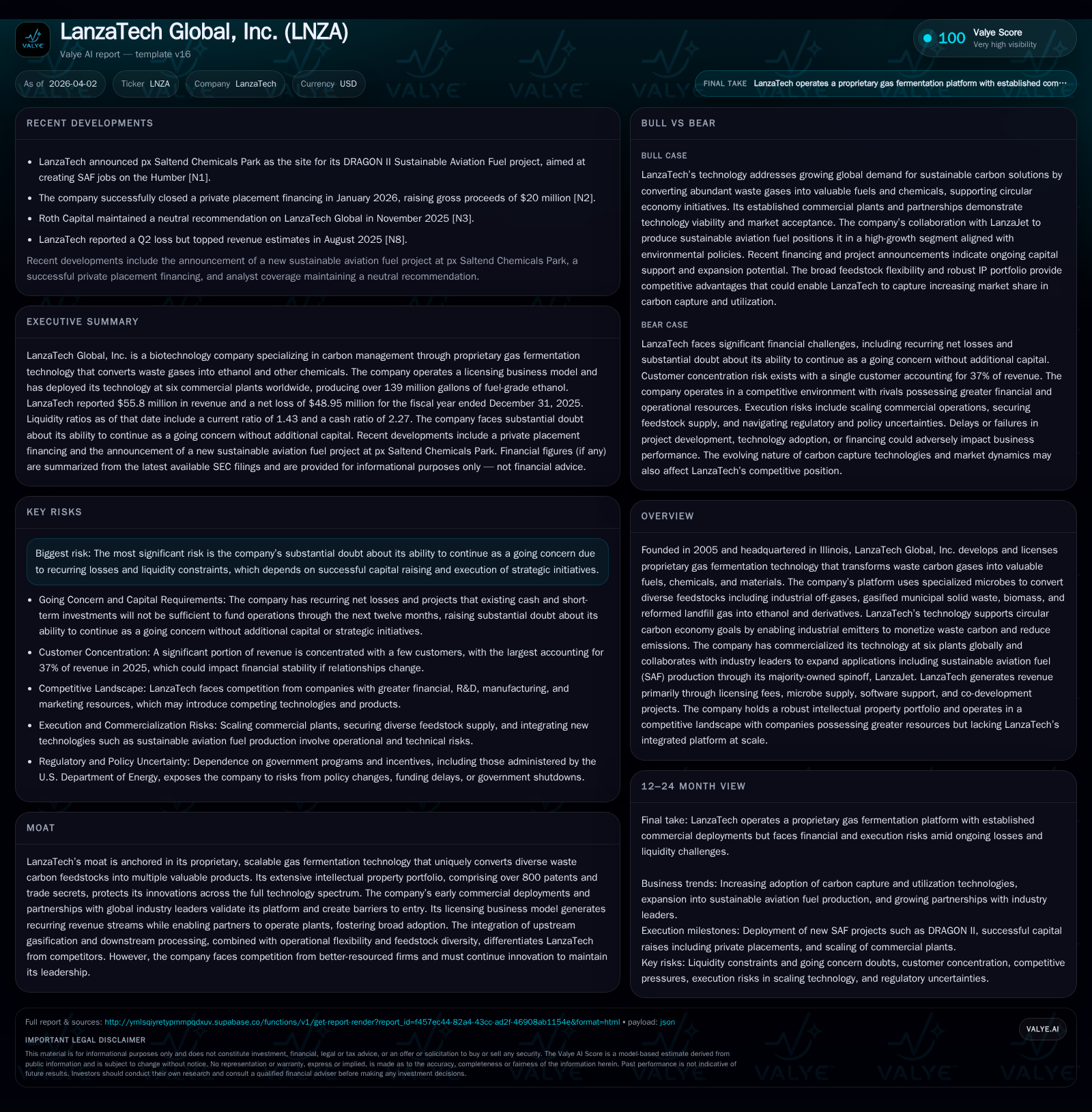

Founded in 2005, LanzaTech Global, Inc. has pioneered carbon recycling via microbial gas fermentation, deploying commercial plants worldwide and expanding applications including sustainable aviation fuel through its LanzaJet spinoff. Despite 12.6% revenue growth in 2025 driven by increased licensing and product sales, the company reported continued large operational losses, with net losses of $49 million and negative operating cash flow exceeding $64 million. Its licensing model provides recurring revenues, yet profitability remains elusive amid heavy R&D expenses and cost optimization efforts. Liquidity pressures persist, evidenced by a cash balance of $13.2 million at end-2025 and substantial doubt about its ability to continue as a going concern without significant capital raises or strategic alternatives.

Company Overview

Founded in 2005, LanzaTech Global, Inc., headquartered in Skokie, Illinois, operates at the intersection of biotechnology and sustainability with its proprietary gas fermentation platform [S1]. The company harnesses specialized microbes that metabolize various industrial off-gases and waste carbon feedstocks—such as biomass-derived syngas and landfill gas—into ethanol and derivative products including sustainable aviation fuel (SAF), chemicals for packaging, fabrics, and other consumer goods [S1]. This capability positions LanzaTech to contribute materially to a circular carbon economy by enabling industrial emitters to monetize waste gas streams while reducing net greenhouse gas emissions.

LanzaTech’s business model centers on licensing its technology rather than owning manufacturing plants outright [S1]. Licensees build, own, and operate facilities using LanzaTech’s platform; in exchange, LanzaTech earns royalty fees tied to revenue generated. The company complements licensing revenues with microbe supply contracts, software support services, contract research agreements (including joint development activities), and co-development collaborations [S4].

A notable extension of the company’s platform is the launch of LanzaJet in 2020—a majority-owned spinoff focused on commercializing sustainable aviation fuel derived via an Alcohol-to-Jet process developed from LanzaTech ethanol [S1]. As of December 31, 2025, LanzaTech held roughly a 45.6% fully diluted interest following a Series A transaction earlier that year that diluted its stake from approximately 53% [S1].

Historical Financial Performance

LanzaTech’s financials evidence a challenging transition from R&D-heavy operations toward broader commercialization.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 56 | -49 | -65 | -79 | +12.6% | +64.5% |

| 2024 | 50 | -138 | -89 | -109 | -20.8% | -2.7% |

| 2023 | 63 | -134 | -97 | -106 | -9771.4% | |

| 2022 | -1 | 0 | -6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -66 | 1257.7 |

| 2024 | 0 | -94 | -1024.3 |

| 2023 | 8 | -106 | -117.1 |

| 2022 | 16.3 |

Source: SEC companyfacts cache [F1].

Revenues declined sharply between FY2023 and FY2024 associated with project completions related to joint development agreements (JDA), followed by a rebound of over $6 million (+12.6%) in FY2025 chiefly due to increases in licensing revenue from LanzaJet sublicensing activities alongside greater CarbonSmart ethanol product sales [S19],[F1]. The company’s cost of revenues grew commensurately (+17%) as it scaled product manufacturing output.

Operational expenses reflect the company's dual-phase nature: while R&D expense slowed by nearly one-third in FY2025 due to workforce reductions and focused program prioritization, SG&A only modestly declined (-6%) despite restructuring costs incurred [S13],[F1]. Operating income losses narrowed meaningfully by over $29 million (-27%), but negative EBITDA persists given heavy upfront investments transitioning toward commercial scale.

Negative operating cash flows improved similarly (-27%) but remain highly adverse at nearly negative $65 million for FY2025 [F1]. Capital expenditures plummeted from $5.3 million in FY2024 to just $1.3 million in FY2025 as management imposed stringent spending controls [F1]. No dividends were declared nor share repurchases executed during recent periods as the firm concentrates resources on preserving liquidity amidst funding needs.

Growth Drivers and Challenges

Technology Platform & Market Adoption

LanzaTech’s moat lies principally in its unique microbial gas fermentation technology that adapts across diverse feedstocks including steel mill off-gases, municipal solid waste syngas, agricultural biomass conversion gases, and reformed landfill gases—application breadth unmatched among peers [S9]. This platform flexibility supports multiple downstream products: ethanol bases fuels or intermediates; ethylene derivatives used in packaging films; surfactants; glycols for detergents; PET precursors enhancing circularity in plastics supply chains [S1].

Commercial validation occurred first with Shougang LanzaTech JV's Chinese plant in 2018—world’s first of its kind—followed by additional plants in India, Belgium, China (three more), totaling six operated sites generating over 139 million gallons of fuel-grade ethanol cumulatively [S1],[F1]. These plants demonstrate scalability albeit still early stage for worldwide mass adoption.

Partnership dynamics also shape growth paths: the LanzaJet entity exemplifies vertical integration from ethanol production into sustainable aviation fuel markets addressing growing mandates among airlines for lower carbon intensity fuels [S1]. Aside from SAF potential—which is capital-intensive with regulatory dependencies—the company is adapting capabilities for single-cell protein production addressing protein feed shortages aligning with agricultural sustainability goals.

Revenue Concentration & Geographic Exposure

In FY2025 more than one-third (~37%) of revenues stemmed from one customer highlighting concentration risks relative to prior year shifts when largest client accounted for only ~25% [S9]. Moreover, about half the receivables are foreign-based reflecting global project footprint particularly strong in Asia-Pacific locales where regulatory push supports renewable fuels infrastructure [S8],[F1].

Competitive Landscape & IP Protection

With over 800 active patents combined across patent families internationally—primarily sole-owned—the IP portfolio fortifies competitive positioning although no single patent dominates sufficiently on its own [S9]. Industry competition intensifies however given influx of better-funded ventures targeting carbon capture utilization with inorganic catalysts or synthetic biology platforms posing innovation challenges requiring ongoing R&D sustenance.

Executional Risks & Liquidity Constraints

A major vulnerability is the company’s recurrent operating losses coupled with liquidity strain [S6],[S10],[F1]. Cash reserves declined dramatically by about $28 million (63%) during FY2025 attributed mainly to operational burn partially offset by financing transactions including issuance of $40 million preferred stock equivalent shares plus a $20 million common equity private placement early in calendar year 2026 [S12]. Nonetheless management states current cash levels are insufficient for sustaining operations beyond twelve months absent further capital injections or asset monetizations triggering substantial doubt about going concern status per GAAP disclosures [S15],[S17].

The debt profile includes a Brookfield loan originated via SAFEs conversion extended into marked-to-market liability arrangements with terms linking repayment to project equity investments which had not materialized as of end-2025 leaving principal outstanding around $60 million face value but fair-valued near $11 million requiring close monitoring of refinancing flexibility [S22],[S23],[F1].

Legal proceedings including derivative lawsuits related to prior business combination structures are acknowledged but considered immaterial presently; litigation reserves are funded within insurance retentions limiting financial impact prospectively [S25],[S6].

Management response entails streamlined corporate priorities emphasizing core technologies commercialization while tightening organizational costs reflected by ~30% cutbacks in R&D spend as well as workforce rationalizations manifesting incremental gross margin improvements even if overall net results remain negative this fiscal cycle [S13],[F1]. Additional avenues pursued include strategic partnerships or asset sales though no definitive milestones disclosed yet beyond announced financings.

Forward-Looking Observations (Analysis)

Although explicit guidance has not been publicly disclosed regarding imminent revenue targets or profitability timelines, key indicators focus investors’ attention:

- Expansion into new geographic licensee developments could drive incremental royalty streams progressing toward model scalability;

- Commercialization success hinges on continued deployment velocity of modular biorefinery units leveraging existing industrial land reducing capex intensity;

- Growing market demand for SAF derived from circular carbon sources under supportive policy frameworks likely enhances long-term addressable market opportunity;

- Continued cost discipline combined with selective R&D investments essential to fend off competitive innovations especially vis-à-vis catalyst-based CCU technologies;

- Securing sufficient capital remains imperative both for sustaining working capital buffer amid cash burn cycles and financing strategic expansions or potential acquisitions.

Monitored metrics should include project level deliverables at key joint venture partners’ facilities (notably China/India), volume ramp-ups of CarbonSmart products sales outside core customer concentrations as well as equity dilution effects constraining shareholder value retention.

Capital Allocation & Returns Profile

Shareholder returns remain sparse given absence of dividends or buybacks since inception due primarily to persistent losses limiting free cash generation capacity [F1],[S24]. Negative operating CF exceeding $64 million annually alongside very modest capex indicates tight reinvestment strategy focused on operational efficiency rather than expansive capital spending [F1],[S13].

Approximate return on equity calculated inversely due to negative equity base yields distorted figure exceeding nominal +1200% mathematically but practically conveying lack of positive net income capable of accruing capital gains sustainably yet potentially signaling turnaround leverage effect if profitability achievable through scale benefits [F1].

Liquidity position bears close scrutiny: ending cash reserves near $13 million compared with high current liabilities totaling over $27 million yield current ratio ~1.43 indicating limited cushion against short-term obligations without fresh capital inflows requested imminently [F1],[S10],[S14],[S17]. Recent financings involving common stock private placements ala January-26 ($20M gross proceeds) plus preferred stock issuances provide some runway extension but remain contingent on execution success alongside strategic deals under evaluation per filings [S12].

Executives have proactively amended articles authorizing increased share count options coupled with reverse stock split actions aimed at governance alignment ahead of expected financing rounds converting legacy warrants exercisable post-split at adjusted price points maintaining orderly capitalization structure integrity [S24].

In summary, while not yet delivering positive returns or positive operating margins historically recorded significant progress toward commercialization scaling exists embodied by steady topline advances accompanied with ongoing cost rationalization although substantial risks emanate from capital constraints underscoring dependency on access to investment markets during unstable macroeconomic conditions typical within clean-tech sectors today.

This analysis is prepared solely for informational purposes based on publicly available filings provided up until April 2, 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments