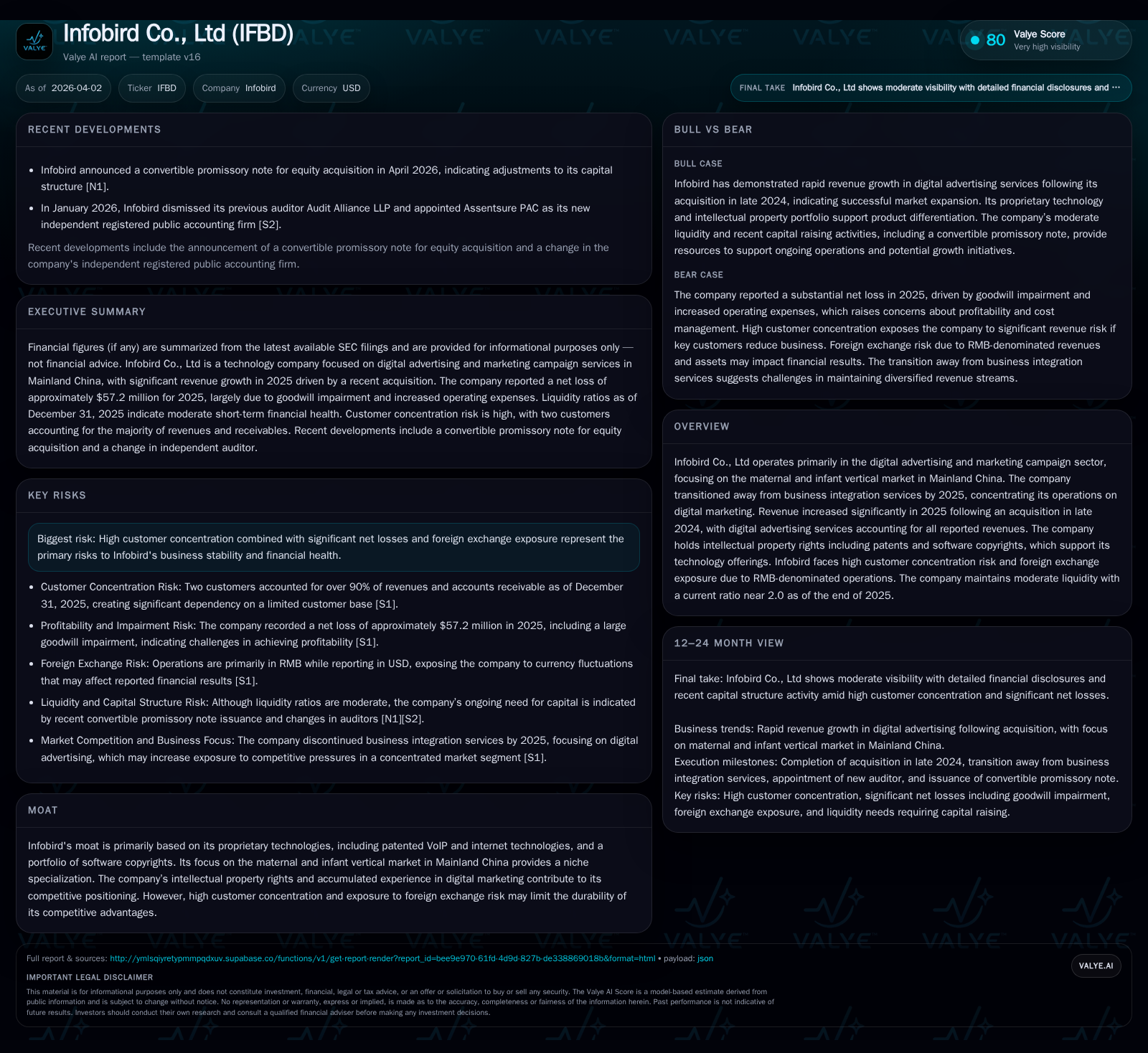

Infobird's Strategic Pivot Drives Revenue Growth Amid Profitability Challenges

Following a late-2024 acquisition, Infobird refocused on digital advertising in the maternal and infant vertical, yielding strong top-line growth but deepening operating losses.

Infobird Co., Ltd shifted its business model in late 2024 to concentrate fully on digital advertising and marketing campaigns within Mainland China's maternal and infant sector. This transition fueled a remarkable 505.5% revenue increase to $8.7 million in 2025, driven by the acquisition’s contribution and expansion in specialized services. Despite this surge, operating losses expanded sharply to approximately $56.4 million, reflecting increased selling and administrative expenses tied to scaling efforts. The company maintains a concentrated customer base with two clients accounting for over 92% of revenues, exposing it to counterparty risk. Liquidity remains stable with a current ratio near 2.0, supported by cash reserves and manageable liabilities. Capital allocation prioritizes R&D and market development with no dividends or share repurchases reported. Foreign exchange risk persists due to RMB-denominated operations reported in USD. Future growth depends on managing customer concentration, executing acquisitions via convertible notes, and navigating regulatory complexities inherent in its VIE structure.

Strategic Pivot and Revenue Growth

Infobird Co., Ltd completed a transformative shift following an acquisition in November 2024 that led the company to focus exclusively on digital advertising and marketing campaigns within Mainland China's maternal and infant vertical [S1]. This strategic realignment resulted in a substantial increase in revenues from approximately $1.44 million in FY2024 to around $8.7 million in FY2025—a growth rate of 505.5% as per reported data [F1][S1]. By the end of 2025, Infobird had fully exited its business integration services segment, consolidating all revenue generation into digital advertising [S1].

Historical Financial Overview

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 9 | -57 | -1 | -56 | +505.5% | -2623.3% |

| 2024 | 1 | -2 | 3 | -2 | +413.5% | +18.5% |

| 2023 | 0 | -3 | -3 | -3 | -94.9% | +83.1% |

| 2022 | 6 | -15 | -5 | -14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -1 | -356.9 |

| 2024 | 2 | -3.2 |

| 2023 | -4.5 | |

| 2022 | -5 | -232.1 |

Source: SEC companyfacts cache [F1].

All figures approximate; revenue and profit metrics are reported in thousands of U.S. dollars.

Operational Drivers

Post-acquisition efforts centered on precision targeting through multi-platform data analytics leveraging social media marketing, search engine optimization, and content distribution tailored for maternal-infant audiences [S1]. The company's proprietary technologies—including one patent related to VoIP/internet technologies and an extensive portfolio of software copyrights—support these capabilities [S17].

R&D investments have increased modestly to sustain ongoing product development essential for maintaining competitive advantage within this niche market [S17][S11].

Customer Concentration & FX Risk

Revenue concentration is pronounced: two customers accounted for approximately 80.7% and 11.3% of total revenues respectively at December 31, 2025 [S7][F1]. These clients also represented roughly 86% and 11% of accounts receivable balances respectively at year-end [S7], underscoring counterparty credit risk.

While reporting currency is USD, nearly all revenues and expenses are denominated in RMB without hedging practices currently employed [S4]. This exposes Infobird’s financial results to foreign exchange volatility risks.

Profitability & Expense Dynamics

Despite rapid revenue growth, operating income declined steeply to a loss of approximately $56.4 million for FY2025 from a loss of $1.7 million the prior year [F1][S1]. Selling expenses more than tripled to about $1.5 million reflecting intensified marketing efforts aligned with growth strategy [S11]. General and administrative costs rose nearly 40%, reaching $2.6 million primarily due to personnel and rental cost increases associated with expanded operations [S11].

Gross profit improved but gross margin contracted compared to prior periods amid higher direct costs [F1][S14]. Net losses were further impacted by non-cash impairment charges recorded during the period [F1][S13].

Capital Allocation & Liquidity

Since its April 2021 IPO raising net proceeds around $22.9 million [S3], Infobird has allocated capital predominantly toward R&D and sales/marketing infrastructure expansion with no dividends or share buybacks declared recently [S3][F1]. Capital expenditures remained stable at approximately $0.77 million annually [F1].

Liquidity remains sufficient with current assets of approximately $9.6 million versus current liabilities near $4.85 million as of December 31, 2025 yielding a current ratio near 2x [F1][S4]. Cash balances were about $6.2 million mid-2024 with short-term borrowings utilized as needed [F1][S10].

Outlook & Risks

Key areas for monitoring include:

- Progress on convertible promissory note funding planned equity acquisitions aimed at expanding product offerings or customer base [N1][S1].

- Efforts to reduce high customer concentration risk which currently leaves financial stability vulnerable.

- Regulatory developments affecting the VIE structure used by Infobird as a Cayman Islands holding company operating through Chinese subsidiaries [S9].

- Ability to sustain technological innovation amid competitive pressures within China’s digital advertising market.

- Managing operational costs effectively to move toward profitability despite aggressive top-line growth.

This analysis is based solely on publicly available SEC filings and news sources cited herein; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments