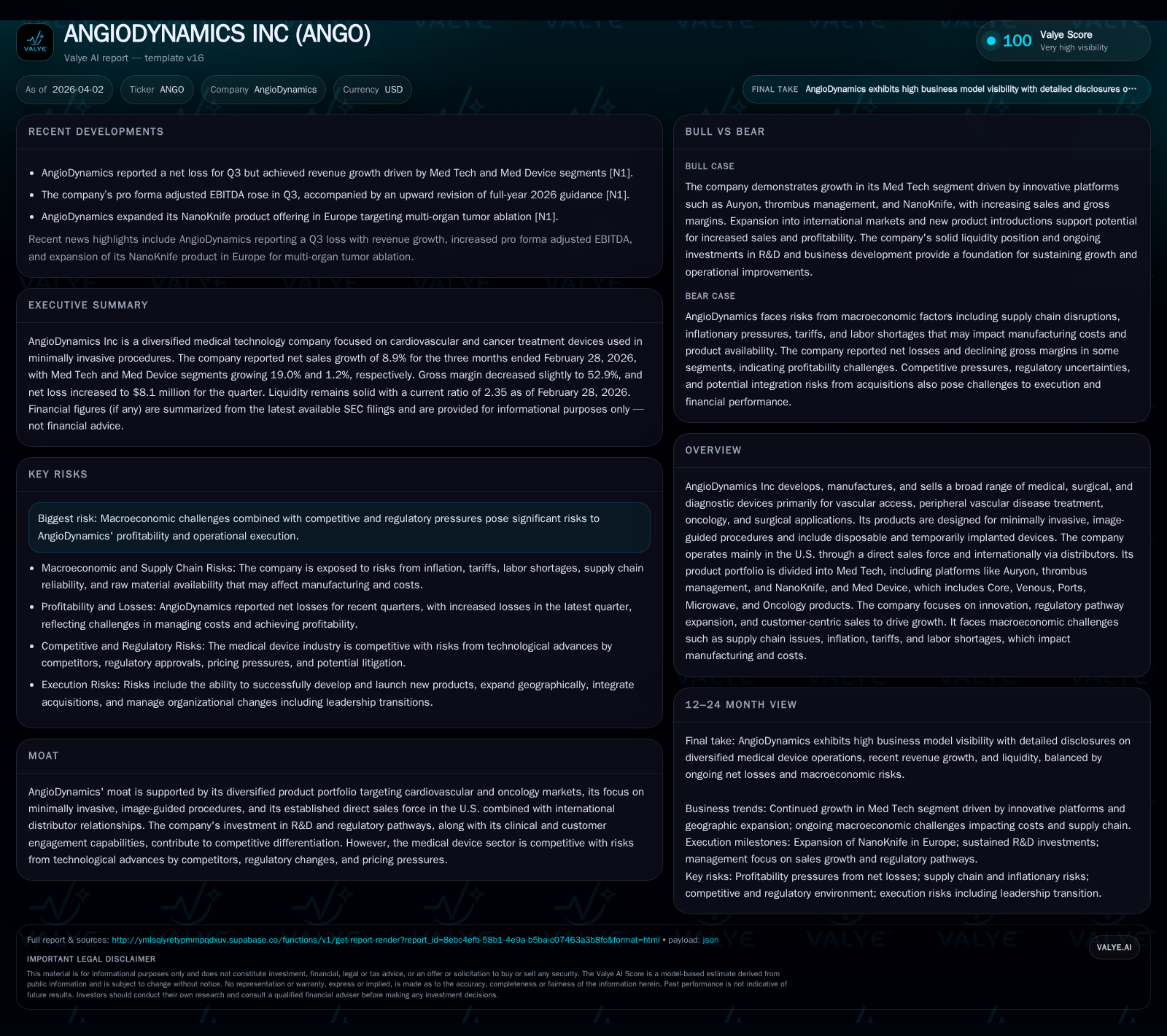

ANGIODYNAMICS' Performance Shift Reflects Innovation and Operational Challenges

AngioDynamics balances robust Med Tech revenue gains with persistent net losses amid inflation and supply chain headwinds.

AngioDynamics has demonstrated notable revenue growth driven mainly by its Med Tech segment, including platforms like Auryon and NanoKnife, with annual sales nearly quadrupling since FY2019. Despite top-line expansion, the company continues to face operating losses, although trends indicate a narrowing deficit compared to previous years. Macroeconomic pressures such as inflation, tariffs, and labor shortages have constrained gross margins and exacerbated operational costs. Capital allocation remains conservative with limited buybacks and negative free cash flow, reflecting ongoing challenges in achieving profitability. Future growth depends on clinical adoption of innovative products and expanding international market presence, particularly in Europe for NanoKnife.

Historical Revenue Growth Breakdown: Med Tech Momentum vs Med Device Stability

AngioDynamics recorded substantial top-line expansion over recent fiscal years with revenues leaping from approximately $71 million in FY2019 to $291 million by FY2021, representing an almost fourfold increase over two years per company facts data [F1]. This explosive revenue growth primarily reflects the rapid uptake of the company's innovative Med Tech platforms, notably Auryon (an image-guided thrombectomy system) and NanoKnife (a minimally invasive ablation technology targeting oncology applications). The Med Tech segment's revenue advanced by more than 19% year-over-year most recently [S6], dwarfing the Med Device segment's low single-digit percentage growth.

The company's product portfolio is split between capital equipment-heavy offerings in the Med Tech sector—which require image-guided minimally invasive procedures—and largely disposable or temporary implant devices within the Med Device division. The latter includes products such as Core disposable catheters, Venous access devices, Ports, Microwave ablation tools, and other Oncology-related disposables.

Growth in the Med Tech arena reflects both new product launches and increasing clinical adoption curves across US markets via direct sales force efforts complemented by distributor relationships internationally. Conversely, the Med Device segment displays more stable but modest top-line progress, likely due to mature product lines facing pricing pressures and competitive dynamics consistent with industry norms [S6].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -34 | -10 | -40 | 4 | +81.6% |

| 2024 | -184 | -28 | -192 | 3 | -251.5% |

| 2023 | -52 | 0 | -51 | 4 | -97.5% |

| 2022 | -27 | -7 | -28 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -15 | -18.6 |

| 2024 | -31 | -89.7 |

| 2023 | -4 | -13.9 |

| 2022 | -11 | -6.3 |

Source: SEC companyfacts cache [F1].

This atypical dip into FY2019-2020 reflects transitional periods preceeding significant portfolio expansion through acquisitions or internal R&D breakthroughs not detailed here but aligning with the exponential rebound observed starting FY2021.

Operational Profitability Trends and Margin Dynamics Over Recent Fiscal Years

Despite strong revenue traction, AngioDynamics has consistently reported operating losses across these years though improving markedly recently. The operating income moved from a deep deficit of roughly -$192 million in FY2024 to a reduced loss of about -$40 million in FY2025 according to SEC filings and factsheet data [F1]. Similarly, net income losses narrowed from roughly -$184 million to -$34 million during this timeframe.

Gross margin metrics reveal divergent trends across segments: The Med Tech segment maintains relatively robust gross margins around mid-60%s supported by volume leverage and price realization despite cost inflation [S6], while the Med Device segment sees more pronounced erosion—dropping into mid-40% levels recently—as tariffs and raw material cost escalation weigh heavily on unit economics.

Key drivers of margin pressure include:

- Escalated cost of goods sold stemming from inflationary impacts on raw materials and manufacturing labor wages;

- Tariff impositions elevating landed costs particularly for imported components;

- Product mix shifts towards newer but less mature technologies affecting absorption of fixed overheads;

- Incremental depreciation related to placement units impacting COGS.

On the operating expenses front, incremental increases in R&D spending—up by about $1.6 million year-over-year through recent quarters—reflect sustained investments in clinical studies, regulatory filings, and new product validation programs crucial for anticipated long-term differentiation [S27]. Concurrently, selling & marketing expenses grew as the company expands its sales footprint and supports launch activities.

These dynamics produce a complex picture where operating leverage partially offsets cost headwinds but profitability remains challenged given macroeconomic inflationary pushes combined with competitive price containment inherent to healthcare procurement practices.

Key Drivers Behind Revenue Expansion and Headwinds Impacting Margins

Strategically, AngioDynamics has emphasized innovation-led growth via its flagship product lines:

- Auryon: Focuses on thrombus management—a high-priority clinical territory benefiting from increasing physician preference for image-guided catheter systems reducing procedural risk.

- NanoKnife: Expanding indications especially within oncology for ablation therapies that offer less invasiveness compared to traditional surgery.

As disclosed in recent news releases and filings ([N12],[S2]), international expansion efforts have centered on broadening NanoKnife's European footprint reflecting substantial untapped multi-organ tumor ablative treatment opportunities backed by regulatory clearances outside the U.S.

These drivers are juxtaposed against persistent external operational constraints attested by SEC risk disclosures ([S4],[S6]):

- Ongoing supply chain shortages impacting availability of critical components leading to backlog management challenges;

- Inflationary pressures inflating direct labor costs alongside procurement expense volatility;

- Tariffs exerting quantifiable negative gross margin impacts amounting to millions annually;

- Labor shortages constraining manufacturing throughput capacity.

The interplay between higher sales volumes commanding better price points (price realization lagging) versus rising cost inputs requires close monitoring as it shapes near-term margin trajectories as well as overall cost structure efficiency.

Future Growth Prospects Anchored by Product Innovation and Geographic Expansion

Looking ahead, AngioDynamics projects multiple growth avenues aligned with clinical adoption curves and continued geographic penetration:

- U.S.-centric direct sales efforts capitalize on embedded physician relationships amplifying cross-selling opportunities within cardiovascular interventionists' practice;

- International expansion focuses particularly on distributor-enabled channels targeting key European markets where NanoKnife recently gained multi-organ tumor ablation indication approval ([N12]);

- Regulatory pathway advancement remains pivotal aiming at faster approvals for novel indications enhancing addressable market size;

- Continuous R&D pipeline investment expected to yield adjunctive technologies supporting core platforms ensuring sustained competitive differentiation ([N2],[S2]).

However, these prospects are counterbalanced by market realities including healthcare reimbursement variability globally plus emerging competitor technologies threatening share retention potential.

Macroeconomic and Supply Chain Challenges Influencing Near-Term Performance

Explicit risk factors cited within recent SEC filings ([S4],[S6],[S18]) emphasize macroeconomic uncertainties severely influencing operational results:

- Raw material pricing volatility forces reactive procurement strategies disrupting cost predictability;

- Lead time delays inflate inventory stocking requirements increasing working capital demands;

- Labor market tightness limits scaling manufacturing output despite demand growth pressures;

- Tariffs constitute recurring drag on gross margins compelling continuous pricing negotiations with customers amidst value-based purchasing regimes.

Consequently, recent quarterly results show discernible gross margin contractions within certain segments attributable directly to these inputs coupled with incremental depreciation charges tied to capitalized assets deployed into production lines.

This environment underscores heightened complexity for AngioDynamics' management team striving to normalize supply chain resiliency while maintaining customer service levels crucial for preserving clinical adoption momentum.

Capital Allocation Review: Cash Position, Buybacks, and Return on Equity Analysis

From a capital allocation standpoint based on latest fiscal year-end figures ([F1]):

- Cash & equivalents stand at approximately $37.8 million as of February 28, 2026 providing liquidity buffer amid continued operating cash deficits;

- Free cash flow remains negative: Operating cash flow was around -$10.1 million netting against capex of roughly $4.5 million translating to an approximate FCF deficit near $14.6 million;

- Limited share repurchase activity ($1.67 million buybacks in FY2025) suggests disciplined preservation of capital rather than aggressive shareholder returns considering persistent net losses;

- Calculated ROE registers negative (~ -18.6%) emphasizing ongoing profitability challenges necessitating structural margin improvements before equity generation stabilizes.

These financial details illustrate constrained cash flow performance limiting capacity for expansive shareholder returns or sizable M&A without external funding sources while underlying equity base remains substantial at $183 million validating balance sheet strength albeit with diminished earnings power.

Monitorables: Critical Upcoming Milestones and Indicators to Watch

Key operational indicators warrant vigilant observation going forward comprise:

- Timing of pivotal FDA or international regulatory approvals accelerating product label expansions particularly for additional NanoKnife indications ([N12]);

- Quarterly earnings guidance revisions capturing shifts in expected revenue progression or margin recoveries amid evolving macro environment ([N2]);

- Supply chain normalization evidenced by reduced lead times and stabilized procurement costs enabling gross margin expansions;

- Clinical trial progress milestones facilitating medical community acceptance validating value proposition enhancing commercial uptake rates;

- Pricing environment evolution specifically response to group purchasing organization negotiations affecting average selling prices within end markets offering tailwinds or headwinds accordingly.

Tracking these variables offers pragmatic visibility into sustainability of current growth trajectory balanced against operational execution risks intrinsic in capital-intensive med tech commercialization phases.

This report synthesizes publicly available financial statements filed with the SEC alongside relevant recent news disclosures without extrapolation beyond documented facts or forward-looking statements provided by AngioDynamics as of early April 2026. It serves informational purposes exclusively without constituting investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments