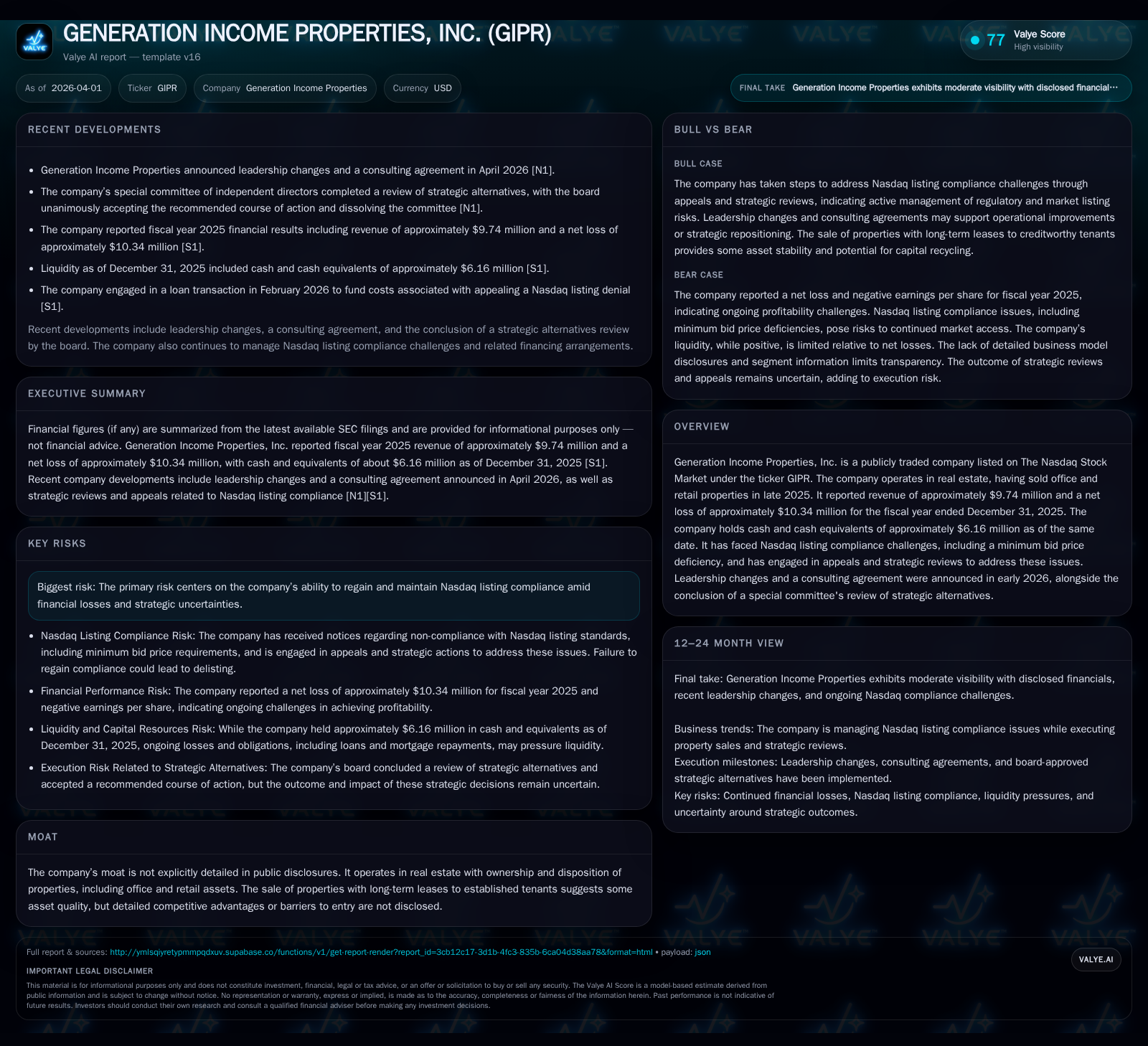

Generation Income Properties Battles Nasdaq Compliance and Strategic Restructuring

After divesting key office and retail assets, Generation Income Properties confronts steep losses and leadership changes while addressing Nasdaq listing challenges.

Generation Income Properties, Inc. (GIPR) experienced a strategic pivot in 2025 marked by disposing of significant real estate holdings amid persistent operating losses. Despite flat revenue, the company faced deepening net losses reaching over $10 million and a negative equity position as of year-end 2025. Concurrently, GIPR is engaged in an active appeal process to address Nasdaq’s minimum bid price deficiency threat to its listing, complemented by board-level strategic reviews and recent leadership turnover. Liquidity remains constrained with limited capital expenditures and no dividend or buyback activity, suggesting a conservative financial posture while exploring recapitalization or restructuring options.

From Rapid Expansion to Strategic Disposition: Historical Performance

Generation Income Properties exhibited strong top-line growth from FY2022 through FY2024, ramping revenue from approximately $5.43 million to over $9.76 million before plateauing in FY2025 at around $9.74 million [F1]. This stall reflects a decisive strategic shift after selling key properties during late 2025, including office assets like the Maitland, Florida property and retail holdings such as the Grand Junction, Colorado site [S27][S29]. Both sales involved long-term leases with established tenants underlining asset quality but also marked a retreat from an acquisitive growth phase.

Operating income has deteriorated each year over this period with losses worsening from -$2.47 million in 2022 to -$6.99 million in 2025—a decline of over 36% year-over-year for the last year alone. Net income mirrors this trajectory with widening deficits reaching -$10.34 million last fiscal year [F1]. Despite stable revenue on paper in 2025 following disposals, margin compression and potentially impairment charges contributed to continued profitability erosion—a common challenge for REITs shedding assets amid adverse market conditions.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 10 | -10 | 929474 | -7 | -0.2% | -23.9% |

| 2024 | 10 | -8 | 1022362 | -5 | +27.9% | -46.0% |

| 2023 | 8 | -6 | 12345 | -3 | +40.5% | -76.6% |

| 2022 | 5 | -3 | 583884 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 1 | 246.2 |

| 2024 | 1159481 | -5 | -144.1 |

| 2023 | 1216280 | -32 | -156.0 |

| 2022 | 1356915 | -12 | -30.3 |

Source: SEC companyfacts cache [F1].

Table: GIPR historical financial performance from FY2022-FY2025 highlighting flattening revenue post-dispositions alongside mounting losses.

Mounting Losses and Capital Efficiency Challenges in 2025

Fiscal results reveal that Generation Income Properties struggled to leverage asset dispositions into operational gains. Operating losses deepened by more than one-third versus the prior period despite no material change in revenues [F1]. The absence of capital expenditures in FY2025 contrasts sharply with prior years’ sizable investments—indicative of restrained reinvestment possibly due to financial pressures or strategic caution [F1].

Operating cash flow remained marginally positive (~$929k), signaling some underlying cash-generative capacity even as headline profitability faltered; however free cash flow is effectively capped given zero capex spend [F1]. This restrained capital outlay jeopardizes future income streams unless offset by portfolio refinements or new acquisitions.

A noteworthy complexity arises given that reported equity was negative $4.2 million at year-end—suggesting accumulated losses exceed owners’ equity base leading to distortions in standard profitability metrics such as return on equity (ROE). While naive calculation yields an inflated ROE figure (246%), this is misleading due to negative denominator effects rather than true economic returns [F1]. This situation underscores deteriorated balance sheet health typically challenging for REITs reliant on investor confidence for capital access.

Nasdaq Listing Compliance: Appeals and Regulatory Hurdles

The company faces direct regulatory risk regarding compliance with Nasdaq’s minimum bid price rules—a common issue for lower-priced securities on the exchange [N1][S4][S6]. Following notice of deficiency due to sub-$1 trading price levels at intervals during early-2026 filings indicate management has initiated appeals processes to preserve listing status.

The procedural timeline involves initial notices followed by potential panel rehearings; successful outcomes could stay delisting proceedings intermittently pending final resolutions [N1][S4]. Such ongoing uncertainty adds pressure on share liquidity and investor sentiment given share suspension risks during protracted adjudications.

This challenge dovetails closely with the company’s liquidity maneuvers — such as raising affiliated loans explicitly to fund legal costs related to the appeals — reinforcing how regulatory enforcement translates into tactical financial strain [S7]. For a small-cap REIT with recent net losses and limited cash reserves (~$6.16 million), this represents material operational risk needing continuous management focus beyond core real estate stewardship.

Leadership Turnover and Consulting Agreements: What It Signals

Recent news confirms board-level executive shifts coinciding with governance refresh strategies typical amid turnaround or restructuring phases [N1]. The engagement of external consultants hints at attempts to reinforce decision-making agility or secure specialized expertise addressing complex challenges including rule compliance and strategic refocusing.

Leadership change often aims to signal recalibration prioritizing improved transparency or execution capabilities especially when combined with formalized special committee oversight reviewing strategic alternatives critical during distressed episodes [N1][S3]. For investors familiar with real estate cycles and REIT governance norms such realignments tend to precede either recapitalizations or asset reconfigurations aiming at preserving franchise value.

Balance Sheet Dynamics: Liquidity, Debt Amendments & Equity Changes

Recent SEC disclosures enumerate several debt amendments involving convertible promissory notes exchanged amongst affiliates and third parties structured with conversion rights tied closely to prevailing market prices but capped below certain thresholds ($0.10 floor per share) reflecting cautious valuations amid turbulence [S7–S10][S13][S28]. These instruments also include guarantees via operating partnerships secured by equity pledges underpinning loan structures evidencing sophisticated credit risk layering relevant for distressed real estate operators.

Net cash position stood around $6.16 million at end-2025—relatively modest for the scale of operations but reflective of proceeds recycling from asset dispositions earlier that year used partly for mortgage repayments connected directly to sold properties [F1][S27][S29]. The negative equity reported signals lingering balance sheet impairment requiring significant recapitalization efforts or asset efficiency enhancements.

Such complexity maps onto industry realities where small-cap REITs grapple with thin margins while balancing debt maturities against constrained refinancing avenues amid capital markets volatility tightened by regulation-driven pressures.

Capital Allocation History: Dividends Suspended Amid Financial Tightening

Consistent with contractionary financial modes amid NASDAQ compliance risks and operating deficits GIPR suspended dividend payments starting FY2025 after distributing approximately $1.16 million in dividends during FY2024 [F1][S19][S24]. No share repurchase programs were announced or executed per latest disclosures.

In REITs facing market adversity suspension of dividends usually points toward capital preservation strategies diverting free cash flow towards deleveraging or operational restructuring rather than shareholder returns—a prudent though confidence-testing stance under current conditions.

Absence of buybacks further reinforces very limited discretionary cash available given ongoing legal costs around listing appeals compounded with operating shortfalls restricting internal resource cushions.

Path Forward: Strategic Alternatives Under Special Committee Review

Latest filings describe conclusion of a special committee's review recommending certain unspecified strategic alternatives now endorsed by the full board [N1][S3]. While specific pathways remain confidential the playbook for comparable small-cap distressed REITs commonly involves pursuing further monetization of property holdings not fully realized in late-2025 disposals, recapitalization efforts involving existing creditors or potential equity raises subject to shareholder approval constraints owing to Nasdaq rules, or even privatization/delisting options if public market support diminishes materially.

This aligns well with typical crisis governance frameworks emphasizing maximizing stakeholder recovery value amidst sustained listing threats compounded by earnings weakness alongside uncertain macroeconomic headwinds.

Key Metrics Snapshot: What Investors Should Monitor Next

- Revenue Stability: Watch quarterly results for impact from any further asset sales post-2025 including leaseback arrangements that may cushion rental income erosion.

- Nasdaq Appeal Outcomes: Monitor announcements from regulatory bodies regarding delisting risks or relief measures impacting stock trading status.

- Balance Sheet Movements: Track disclosures regarding convertible note conversions or amendments plus new borrowing facilities affecting leverage ratios.

- Cash Flow Trends: Assess operating cash flows Q-on-Q for signs of stabilization or accelerating distress factoring reduced capital spending profiles.

- Capital Policy Updates: Stay alert for board commentary on resuming dividends/share repurchases reflecting recovered financial health or ongoing prudence under tighter conditions.

Disclaimer: This analysis relies solely on publicly disclosed information as cited without speculative projections or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments