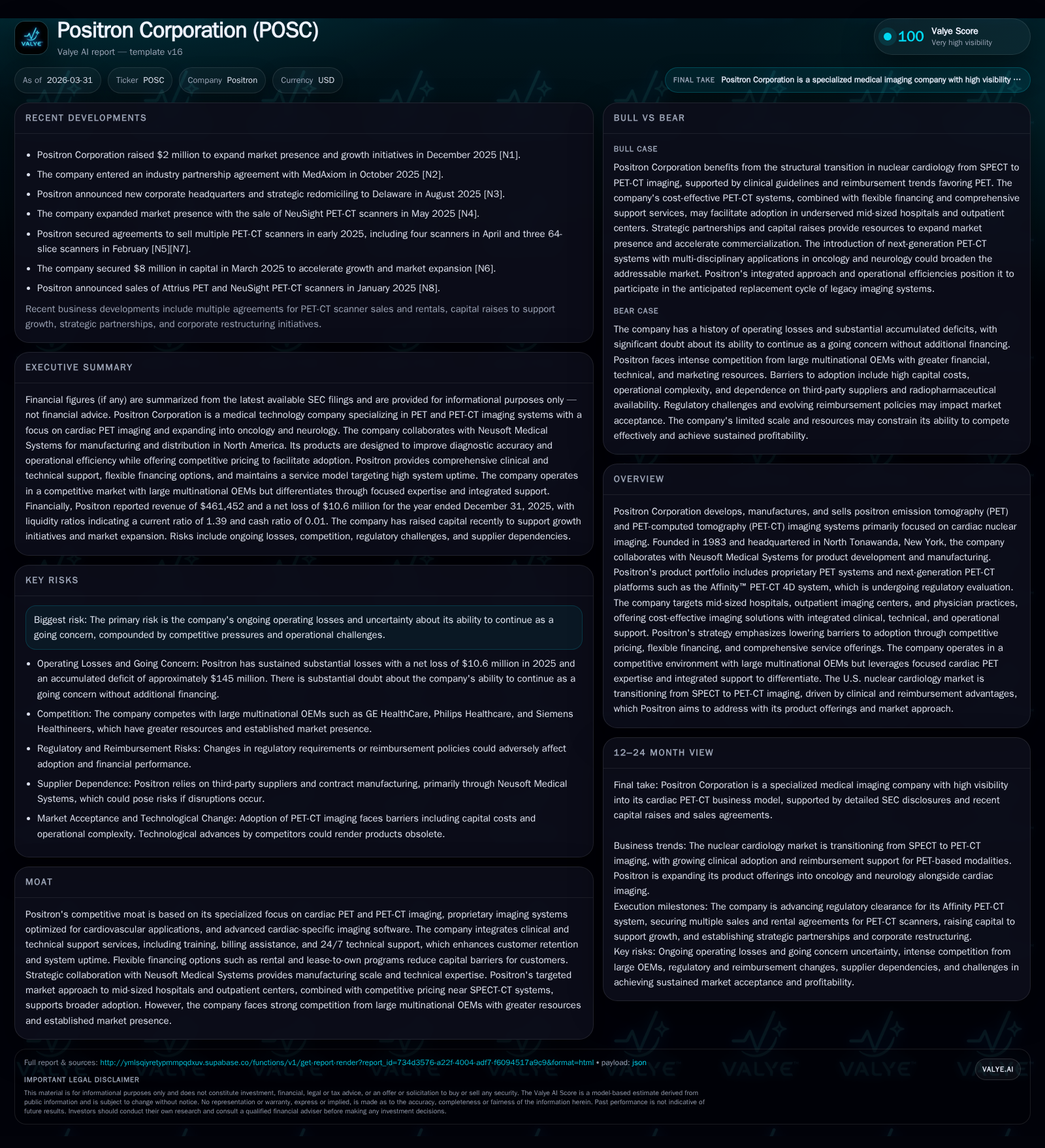

Positron Corp’s Cardiac PET-CT Growth Hindered by Persistent Operating Losses and Cash Strain

Positron focuses on cardiac PET-CT imaging innovation but faces financial hurdles amid expanding clinical applications.

Founded in 1983, Positron Corporation develops specialized PET and PET-CT molecular imaging systems with an emphasis on cardiac nuclear imaging. Its product line targets mid-sized hospitals and cardiology practices, offering cost-effective imaging solutions supported by comprehensive service and financing models. Despite recent revenue growth driven by strategic partnerships and emerging oncology applications, Positron remains unprofitable with substantial operating losses and cash flow deficits raising going concern doubts. The company aims to leverage a lower-cost value proposition against large equipment OEMs while navigating regulatory milestones and market adoption challenges.

Company Background and Historical Performance

Positron Corporation, incorporated in Texas in 1983 with headquarters in North Tonawanda, New York, develops positron emission tomography (PET) and PET-computed tomography (PET-CT) imaging systems primarily focused on cardiac nuclear imaging [S1][S23]. The company integrates proprietary imaging technology with clinical support services including physician training, billing assistance, and technical support designed to enhance system uptime for mid-sized hospitals, outpatient centers, and physician practices [S6][S25].

Financial data reveals persistent operational losses amid modest revenue growth. Total revenue rose from $259K in FY2014 to $461K in FY2025—an approximate 78% increase year-over-year—indicating early commercial traction but still limited scale [F1]. Despite this growth, the company has not achieved profitability; operating income deteriorated from a loss of about $2.7 million in FY2014 to roughly $10.5 million in FY2025. Net income similarly declined to a loss exceeding $10.6 million in FY2025 from positive earnings in earlier years [F1]. This trend highlights ongoing challenges scaling operations profitably.

Operating cash flow remained negative at approximately -$4.7 million for FY2025 while capital expenditures were relatively low but rising modestly—signaling cautious investment into product development or infrastructure expansion. Shareholders’ equity stood at about $1.44 million as of year-end 2025; however, the company carries an accumulated deficit close to $145 million reflecting sustained historical losses that weigh heavily on balance sheet strength [F1].

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 461452 | -11 | -5 | -10 | ||

| 2014 | 259000 | 0 | -3 | -45.6% | -97.5% | |

| 2013 | 476000 | 3 | -3 | -3 | +25.9% | +256.4% |

| 2012 | 378000 | -2 | -2 | -5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -734.4 | |

| 2014 | -10.3 | |

| 2013 | -3 | -30.5 |

| 2012 | -2 | 35.4 |

Source: SEC companyfacts cache [F1].

Note: Latest fiscal year shows significant worsening of losses despite revenue growth.

Market Positioning and Industry Dynamics

Positron's competitive advantage lies in its dedicated focus on cardiac PET and next-generation PET-CT technologies optimized for cardiovascular diagnostics. It offers advanced cardiac-specific software tools supporting workflow efficiencies such as coronary visualization and motion correction [S6][S7]. This specialization contrasts with larger competitors like GE HealthCare, Philips Healthcare, and Siemens Healthineers that provide broader diagnostic portfolios but less targeted cardiac solutions.

The company's strategic partnership with Neusoft Medical Systems enhances its capacity through outsourced manufacturing primarily based in China while allowing access to technical expertise critical for product development [S1][S25][S27]. This collaboration is essential given Positron's comparatively limited internal resources.

Historically high capital costs of PET/PET-CT systems relative to SPECT technology have constrained widespread adoption predominantly to larger institutions. Additional barriers include complexities of radiopharmaceutical logistics and the need for specialized clinical expertise. Positron aims to reduce these hurdles by offering competitively priced systems often comparable to SPECT-CT pricing alongside flexible rental and lease-to-own financing options that lower upfront investment requirements [S7].

Clinical endorsement of cardiac PET over SPECT is increasing due to superior diagnostic accuracy including quantitative myocardial blood flow metrics. Advances such as new Fluorine-18 radiotracers improve logistical feasibility by easing challenges associated with short-lived isotopes traditionally used in PET imaging [S12][S17][S22]. Additionally, Medicare reimbursement rates around $2,250 per outpatient PET study provide favorable economic incentives compared to legacy modalities supporting provider adoption [S12][S22].

Product Development and Growth Prospects

Positron’s portfolio includes dedicated cardiac PET systems alongside preparations for launching the Affinity™ PET-CT 4D system—a next-generation platform designed for multi-disciplinary clinical applications including cardiology, oncology, and neurology [S1][S25][S28]. Regulatory testing for this platform is underway involving performance validation partly conducted at Positron's own facility with assistance from independent certifiers such as Intertek [S28][N1].

Expanding clinical indications beyond cardiology represent a key growth area with oncology explicitly noted as a vertical opportunity leveraging molecular imaging capabilities embedded into new hardware platforms. Neurology also presents potential synergies given conditions amenable to molecular diagnostic techniques.

Recent orders secured from leading nuclear cardiology practices confirm early commercial interest; however most historical revenues derive from service contracts linked to the installed base of PET systems rather than direct equipment sales—highlighting reliance on recurring service income during early commercialization stages [N1][S18][F1].

Financial Health and Capital Allocation

Financially precarious conditions persist due to steep net losses intensifying sharply in FY2025 despite revenue gains—the operating margin deficit suggests elevated fixed costs or underutilized capacity during scale-up phases [F1]. Operating cash flow remains deeply negative (-$4.7 million), while capex levels remain modest indicating conservative reinvestment but insufficient free cash flow generation (estimated negative free cash flow near -$4.7 million considering capex) [F1].[N1]

Working capital was positive at approximately $937K as of December 31, 2025 due to current assets exceeding liabilities; nonetheless liquidity constraints limit operational flexibility [F1][S10]. Management expresses substantial doubt about the company's ability to continue as a going concern without additional financing through equity or debt issuance under uncertain terms [S1][S10].

Capital allocation has prioritized advancing clinical validation efforts and regulatory submissions for advanced products like Affinity™, alongside sustaining operational expenses rather than shareholder returns—no dividends have been declared or are planned given persistent losses [F1][S8]. Equity improved year-over-year but remains minimal relative to accumulated deficits nearing $145 million reflecting deep value erosion necessitating future profitability breakthroughs for tangible returns.[F1]

Risks Highlighted by Regulatory Filings

Key risks include:

- Ongoing operating losses causing substantial accumulated deficits impairing financial sustainability.

- Going concern uncertainties posing risk of restructuring or severe curtailment absent successful capital raises.[S1]

- Intense competition from well-capitalized multinationals threatening market share expansion.[S6][S26]

- Regulatory challenges including pending FDA clearance for new systems critical for commercial launch.[S28]

- Dependence on third-party manufacturing exposing supply chain continuity risks.[S26]

- Reimbursement uncertainties dependent on government programs subject to policy changes affecting demand.[S12]

- Limited human resources with only ten full-time employees highlighting execution risk.[S13]

- Compliance exposure due to extensive healthcare regulations requiring costly oversight.[S4][S8]

Outlook & Monitoring Points

Absent explicit guidance beyond strategic initiatives targeting operational scale-up and oncology/neuro market expansion via next-gen products, key monitoring areas include:

- Progress on FDA clearance milestones for Affinity™ PET-CT system impacting incremental revenues.

- Adoption rates within mid-sized hospitals and outpatient cardiology centers measured by order volume outside pilot installations.

- Ability to maintain liquidity through capital markets access amid dilution pressures given concentrated stockholder ownership.[N1][S16]

- Developments improving radiopharmaceutical availability facilitating clinical workflows.

- Competitive responses from major OEMs including potential pricing or bundling tactics targeting similar customers.

Summary

Positron Corporation offers niche-focused innovation within cardiac PET/PET-CT molecular imaging supported by comprehensive service infrastructure aimed at increasing adoption among underpenetrated mid-sized medical facilities. Early commercial progress is evidenced by recent orders and collaborations leveraging Neusoft’s manufacturing scale; however heavy operating losses paired with cash shortfalls create significant uncertainty around near-term viability without further capital infusion or rapid revenue growth. The company’s strategy aligns well with evolving clinical guidelines favoring PET over SPECT modalities supported by reimbursement frameworks incentivizing advanced diagnostics yet faces execution complexity amid entrenched incumbents and regulatory hurdles.

This document is prepared solely for informational purposes based on referenced public filings and news without expressing any investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments