Live Oak Acquisition Corp. V’s Transition Hinges on Teamshares Merger Execution and Capital Strategy

A blank check SPAC with a focused acquisition mandate prepares to combine with Teamshares, aiming to leverage operational expertise and capital markets access.

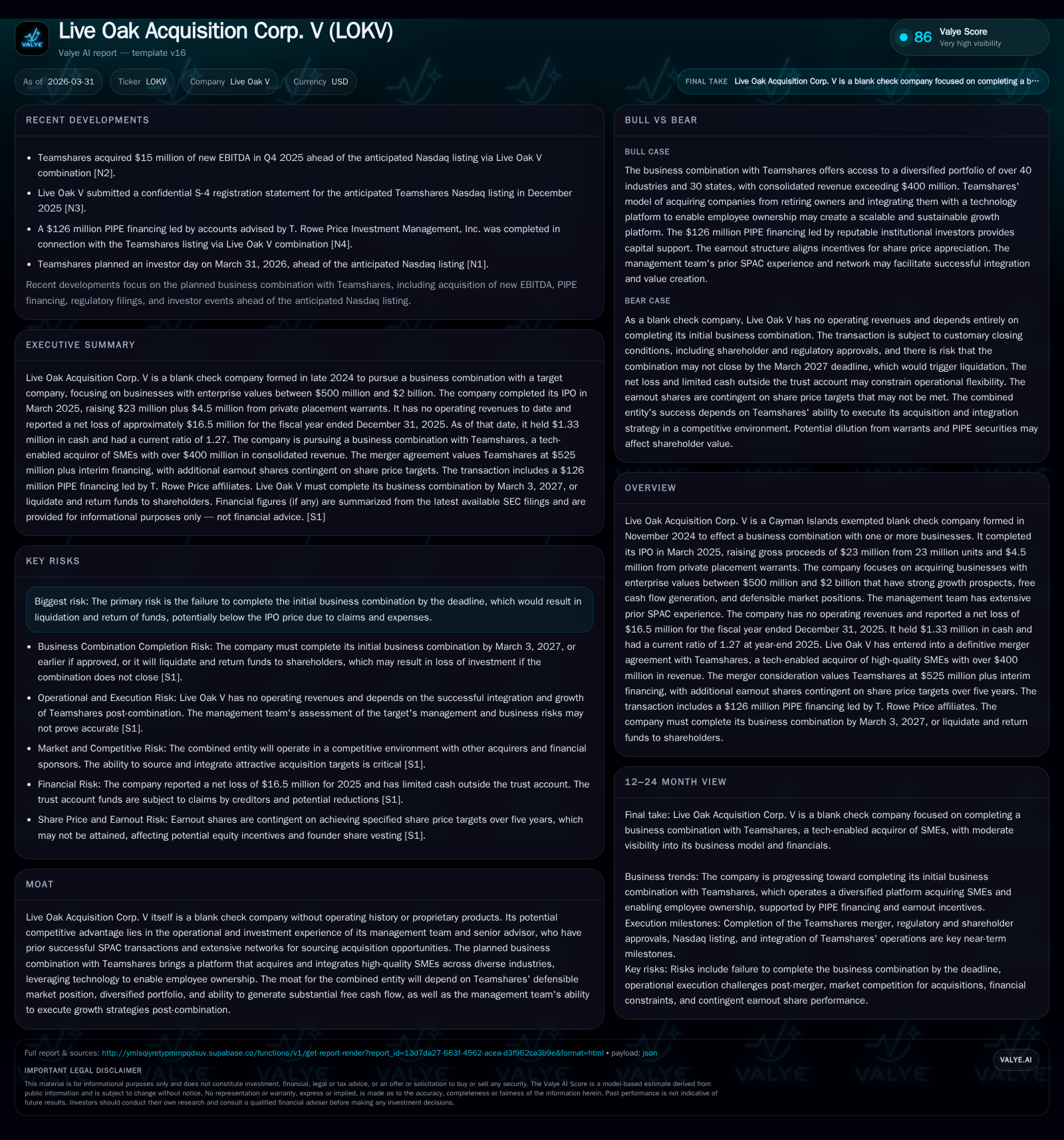

Live Oak Acquisition Corp. V (LOKV) is a Cayman Islands exempted blank check company formed in late 2024 and completed its IPO in early 2025, raising $23 million plus a private placement of $4.5 million in warrants. It targets business combinations with companies valued between $500 million and $2 billion, emphasizing growth, free cash flow, and defensible positioning. To date, it has no revenues and operated at a net loss of $16.5 million for 2025 while maintaining a modest cash position and current ratio of 1.27. The company is advancing its definitive merger agreement with Teamshares, a platform acquiring high-quality small-to-medium enterprises enabled by technology and employee ownership models. The success of LOKV’s transition depends heavily on consummating this business combination under terms that align capital structure, shareholder redemptions, and the ability to deploy further financing as needed.

Company Background and Historical Performance

Live Oak Acquisition Corp. V (LOKV) was established on November 27, 2024 as a Cayman Islands exempted blank check company formed solely for the purpose of effecting one or more business combinations [S1][S22]. It completed its IPO in March 2025 by selling 23 million units priced at $10 each including an over-allotment option exercise bringing gross proceeds to approximately $23 million. Concurrently, the Sponsor privately placed 4.5 million warrants at $1 each generating an additional $4.5 million for the company [S1][S22]. Total cash raised initially was about $27.5 million gross before expenses.

As a blank check company without operating history or commercial revenues prior to a business combination, LOKV reported no revenues through fiscal year end December 31, 2025 [F1]. Operating losses amounted to approximately -$9.1 million during this period (reflecting organizational costs, administrative expenses related to IPO readiness, legal fees, advisory costs) driving a net loss of about -$16.5 million [F1]. Cash reserves outside the Trust Account stood at roughly $1.33 million while the current ratio was measured at 1.27 indicating sufficient liquidity for ongoing administrative activities but minimal working capital [F1].

Recent filings confirm no ongoing litigation or material contingencies against the company or its management supporting an orderly pending transition toward its business combination target [S17].

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Net loss reflects pre-business combination operational costs primarily related to IPO setup and administrative expenses without revenue generation.

Business Model: Investment Focus and Strategy

Although LOKV may pursue combinations across various industries post-IPO, management has focused on acquiring businesses generally valued between $500 million to $2 billion that exhibit robust growth prospects coupled with strong free cash flow generation capabilities underpinned by defensible competitive moats [S22][S15]. This acquisition strategy capitalizes on operational expertise from its senior management team and advisor network who bring broad transactional experience sourcing middle-market opportunities conducive to value creation.

Their evaluation criteria include:

- Defensible market positions creating barriers to entry.

- Businesses at strategic inflection points benefiting from public market access.

- Diversified customer bases mitigating downturn risks.

- Platforms scalable through add-on acquisitions leveraging management know-how.

- Firms demonstrating ability to generate returns exceeding cost of capital.

This approach aims for synergy between management’s operational involvement post-merger and access to public capital markets allowing acceleration of growth initiatives [S15][S10].

Upcoming Business Combination with Teamshares

LOKV has entered into a definitive merger agreement with Teamshares, a tech-enabled platform focused on high-quality SME acquisitions incorporating employee ownership mechanisms [N1][S21]. Teamshares represents the company’s principal vehicle leveraging technology-driven integrations across diverse SMEs aligned tightly with LOKV’s criteria emphasizing sustainable cash flows and growth avenues.

The merger consideration contemplates an aggregate implied value near $525 million plus additional interim financing converting into equity upon closing [S21][S29]. Contingencies include possible earnout shares issuance up to six million common shares signaling performance-based incentives aligned with long-term value creation [S21].

Investors should monitor milestones such as:

- Final closing conditions including requisite approvals.

- Shareholder vote scenarios or tender offer provisions applying redemption rights.

- Details surrounding any PIPE financing arrangements integral to transaction funding beyond Trust Account balances.

Financial Position and Capital Allocation Insights

Despite low operating liquidity ahead of business combination closure—with only about $1.33M cash outside Trust Account—the company benefits from substantial trust funds totaling over $230 million as per initial IPO proceeds plus warrant placements earmarked exclusively for mergers [S22][F1]. Funds within the Trust Account are segregated from general corporate purposes but can be deployed post-combination directly or via financing structures including PIPE deals or debt issuances designed to optimize deal economics [S23][S28].

Shareholders have redemption rights at approximately $10.39 per share based on Trust Account value as of late 2025 but are subject to aggregate redemption caps without company consent (15% limit), preserving capital availability intended for the initial business combination’s liquidity needs [S11][S12][S24].

Sponsor-related provisions constrain insider redemptions ensuring alignment with public investors; insiders waive liquidation rights if the transaction does not complete protecting overall shareholder interests [S6][S12].

Capital allocation flexibility includes private purchases of shares from redeeming shareholders potentially improving deal closing odds by softening redemption pressures; these activities comply with SEC rules designed to avoid conflicts impacting shareholder voting outcomes [S7][S14][S25].

No dividends or buybacks have been declared given the company's blank check status focusing resources entirely towards closing acquisitions and maintaining regulatory compliance through continuous disclosure filings consistent with Nasdaq listing standards [S26].

Risks and Considerations

Completion risk remains critical: failure to consummate an initial business combination by March 3, 2027 results in mandatory liquidation distributing remaining trust assets less claims and expenses—potentially below IPO levels—and ceasing operations altogether [S1][S20].

Other considerations include:

- Competitive bid environment among SPACs, private equity groups and strategic buyers targeting overlapping SME platforms challenging exclusivity windows; limited financial firepower may hamper bidding versus larger peers [S26].

- Potential dilution stemming from PIPE instruments or debt financing if purchase price exceeds Trust funds after redemptions [S23][S29].

- Regulatory complexities connected with tender offers versus shareholder vote negotiations impacting timing and investor sentiment.

- Absence of historical operating metrics complicates valuation comparables until combined entity reports subsequent periods.

What To Watch Next (Analysis)

With limited direct guidance publicly available beyond regulatory disclosures and merger proxy filings expected closer to deal execution dates, investors should monitor:

- Announcement of definitive closing timeline details including any amendments extending deadlines supported by shareholder votes.

- Structure and scale of any PIPE financings supplementing Trust funds especially participation by cornerstone investors providing confidence in deal financing.

- Initial financial disclosures post-merger showing combined entity revenue run-rate growth trajectories tied to Teamshares’ SME platform effectiveness.

- Redemption election levels by public shareholders reflecting confidence or skepticism toward acquisition terms.

- Development of incentive plan filings granting equity awards aligning management interests post-close as stipulated under merger covenants [S18].

Disclaimer:

This analysis is intended solely for informational purposes regarding Live Oak Acquisition Corp. V based on publicly available data as of March 31, 2026. It does not constitute investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments