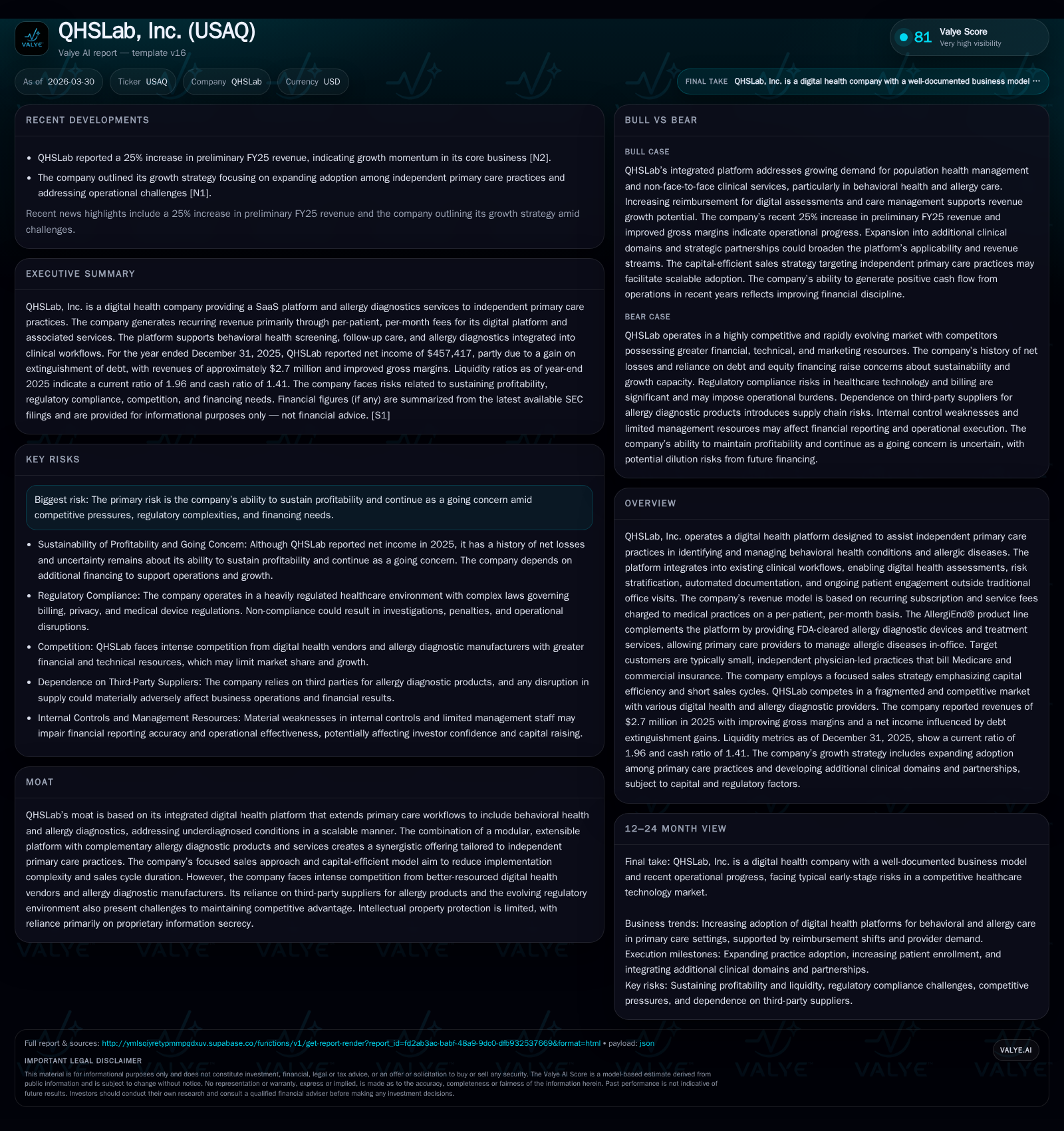

QHSLab’s Transition to Profitability: Evaluating Growth and Financial Resilience in Digital Health

QHSLab, Inc. has moved from sustained losses to net income in 2025, driven by its integrated digital health platform targeting independent primary care providers.

After years of operating losses, QHSLab posted positive net income in 2025 aided by a gain on debt extinguishment and expanding revenues from its digital behavioral health and allergy diagnostics platform. Its subscription-based, per-patient revenue model reflects steady growth in contracted practices and patient engagement, though margins face pressure from increased sales and R&D investments. Despite meaningful improvements in cash flow and capital structure marked by significant debt reduction and share buybacks, continued liquidity constraints and competitive regulatory risks pose challenges to sustaining profitability and scaling operations.

From Losses to Positive Income: Tracing QHSLab’s Historical Performance

QHSLab’s financial trajectory highlights a significant turnaround from extended losses to profitability in fiscal year 2025. The company reported revenues of approximately $2.69 million for the year ended December 31, 2025, up from about $2.13 million the previous year [F1]. This top-line growth aligns with expanding adoption among targeted independent primary care practices.

Operating income declined roughly 36%, from $205,738 in 2024 to $131,244 in 2025 [F1], reflecting elevated costs as the company invests in sales, marketing, research & development (R&D), and administrative functions during scaling efforts.

Net income shifted from a loss of $259 thousand in 2024 to a positive $457 thousand in 2025. This improvement was materially influenced by a non-recurring gain on extinguishment of debt near $1.15 million [S1][S10]. Operating cash flow also improved by over 25% year-over-year to $178,118 in 2025 from $142,437 in 2024 [F1], indicating strengthening core business cash generation.

Balance sheet improvements are notable: current liabilities decreased sharply from approximately $2.4 million at the end of 2024 to around $450 thousand by the end of 2025 [F1][S5][S10]. The current ratio stood near 1.96 times at year-end reflecting enhanced short-term liquidity.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 457417 | 178118 | 131244 | +276.4% |

| 2024 | -259239 | 142437 | 205738 | +44.6% |

| 2023 | -468362 | -159627 | -240158 | +53.0% |

| 2022 | -996001 | -350994 | -560539 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 950470 | 28.1 |

| 2024 | 42.7 | |

| 2023 | 50000 | 124.7 |

| 2022 | 50000 | -1306.3 |

Source: SEC companyfacts cache [F1].

(Figure: Summary of Selected Annual Financial Metrics [F1])

The Integrated Platform Model: Behavioral Health Meets Allergy Diagnostics

QHSLab offers an integrated digital health platform combining behavioral health assessments with allergy diagnostics under the AllergiEnd® brand [S1][S4]. This dual approach targets independent primary care physician (PCP) practices that bill Medicare and commercial insurers.

The platform features adaptive screening logic that tailors assessments based on patient responses prior to office visits. Automated documentation generates provider reports delivered directly into electronic health records (EHRs), minimizing workflow disruption for clinicians [S1].

AllergiEnd® enables PCPs to perform FDA-cleared point-of-care allergy diagnostic testing and immunotherapy treatments within their offices. By embedding allergic disease management into routine primary care encounters digitally supported by patient engagement workflows, QHSLab aims for higher patient retention and increased reimbursable clinical services utilization [S4].

The platform’s modular design facilitates expansion into additional clinical domains while maintaining standardized onboarding processes suited for smaller physician groups with limited IT resources [S4][S13].

Revenue Drivers and Patient Engagement Dynamics

Recurring revenues depend on growing the number of contracted medical practices and increasing patient enrollment per practice [S4]. Subscription fees are charged per patient per month for access to digital assessments and asynchronous follow-up care management services; utilization fluctuations affect revenue variability.

Patient participation rates critically influence sustainable growth—higher engagement with pre-appointment digital screenings enriches clinical data enabling more personalized interventions [N1][S4]. Allergy diagnostics adoption further increases utilization intensity as patients receive additional testing and treatments.

Retention of existing practices helps mitigate churn risks amid competition; demonstrating continuous value through reimbursement support or new product features is vital [N1].

Profitability Amid Cost Pressures: Operating Leverage Analysis

Despite revenue gains in fiscal year 2025 versus prior periods, operating income margins compressed due to increased spending across software development (R&D), sales and marketing (up ~34%), clinical program support staffing, and sourcing costs related to AllergiEnd® devices [F1][S24][N1].

Gross margin improved modestly (approximately 67%) benefiting from product mix synergies post-acquisition activities but was offset by elevated selling expenses leading to lower EBIT margins compared to prior year [F1][S22][S24].

Management focuses on capital-efficient operations via limited customization and standardized implementations aimed at shortening sales cycles—critical given budget constraints typical among small independent practices [S4].

Capital Allocation: Debt Reduction and Shareholder Returns

In fiscal year 2025 QHSLab substantially improved its capital structure by extinguishing significant portions of outstanding loans—including repurchasing an acquisition note—resulting in a gain exceeding one million dollars that favorably impacted net income [S10].

Current liabilities fell sharply from over $2.4 million at December 31, 2024 down below half a million by end-2025 illustrating reduced leverage risk [F1][S10]. Cash balances rose with cash equivalents totaling approximately $636K at year-end providing essential liquidity runway.

Share repurchases totaled nearly $950K during the year signaling management confidence amid improving fundamentals; no dividends have been declared or paid historically nor planned currently as cash preservation remains a priority [F1][S27]. Return on equity approximated a healthy ~28% for FY25 driven primarily by profit including non-recurring items but indicative of rising capital efficiency if operational profits sustain.

Regulatory Environment and Competitive Pressures

QHSLab operates within a heavily regulated healthcare environment subject to HIPAA privacy rules protecting health information; Stark Law restricting physician referrals; Anti-Kickback Statutes; federal False Claims Act provisions; FDA oversight over medical devices including allergy diagnostics; and evolving reimbursement regulations [S6][S7][S14][S26].

Compliance complexity is heightened by fragmented enforcement across jurisdictions requiring operational agility; violations may result in fines or exclusion from government programs undermining client adoption incentives [S6][S7].

Competition includes better-capitalized vendors specializing either solely in digital behavioral health platforms or allergy diagnostics as well as integrated offerings posing ongoing threats given their resource advantages [S17][S18]. Intellectual property protections currently rely mainly on trade secrets rather than extensive patent portfolios.

Challenges Ahead: Sustaining Growth Amid Financing Needs

Despite recent profitability milestones including positive cash flows since FY24 paired with shrinking debt load—QHSLab faces material risks sustaining these gains absent additional capital raises or refinancing opportunities [S1][S12]. The CEO’s decision not to draw salary underscores resource constraints.

Customer concentration among small independent PCP clinics poses scalability challenges due to constrained budgets slowing uptake relative to larger integrated systems [N1][S13]. Supply chain dependencies for AllergiEnd® products add potential service continuity risks.

Ongoing regulatory changes combined with intense competition demand continued execution focus on sales cycle efficiency improvements alongside planned clinical domain expansions currently gated by available financial resources.

What To Monitor Next: Growth Indicators and Financial Stability Metrics

Key metrics for investors include:

- Quarterly trends in new contracted physician practices adopting subscriptions;

- Average active patient counts per practice;

- Practice retention rates versus patient opt-out rates;

- Utilization shifts between digital screening versus follow-up care management;

- EBITDA margin trajectory linked to expense control particularly sales & marketing efficiency;

- Regulatory updates affecting FDA-cleared devices;

- Competitive developments impacting market share;

- Debt facility modifications influencing liquidity profile through quarterly filings.[N1][S3]

In summary,QHSLab occupies a strategically differentiated niche combining scalable behavioral health screenings with embedded allergy diagnostics tailored for primary care settings—a model aligned with healthcare digitization trends but challenged by legacy financing structures common among emerging public companies. Achieving consistent profitability hinges on maintaining revenue momentum via subscription renewals plus complementary clinical service upsells balanced against prudent expense management amid regulatory scrutiny extending into the foreseeable future.

This analysis is prepared solely for informational purposes based exclusively on publicly filed company documents and reputable news sources without offering investment advice or price targets. Readers should conduct further due diligence customized to their needs before forming conclusions regarding QHSLab or related sectors.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments