Spark I Acquisition Corp’s Path to Business Combination: Financial and Strategic Outlook

A detailed analysis of Spark I Acquisition Corp's financial history, sponsor support, and strategic prospects as it approaches its extended business combination deadline.

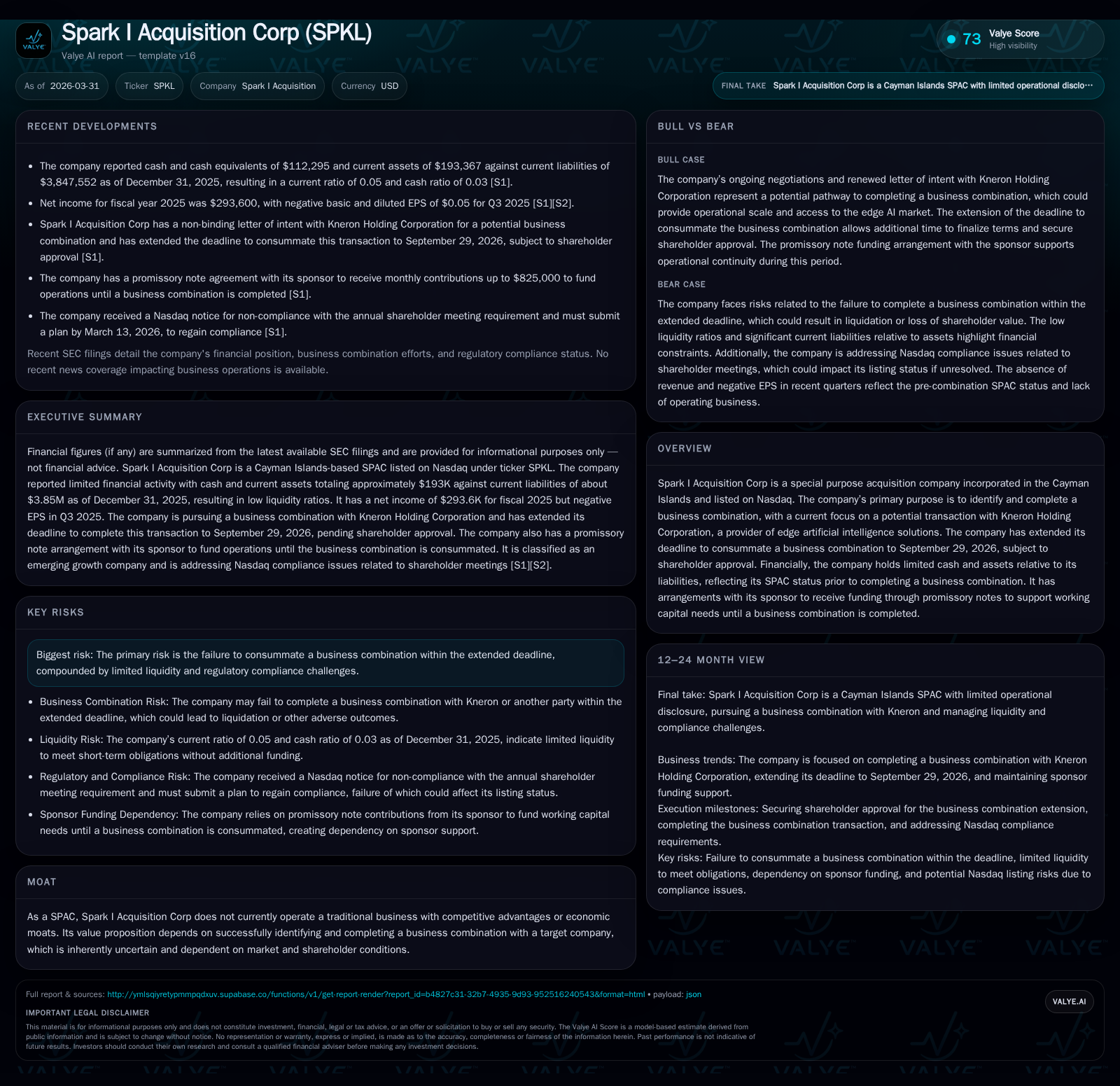

Spark I Acquisition Corp remains in the critical transitional phase typical of SPACs, with its financial profile characterized by limited liquidity and increasing liabilities amid ongoing operating costs. The sponsor has implemented a structured non-interest bearing promissory note to support working capital needs following shareholder-approved extension of the merger deadline to September 2026. While the company's focus on a business combination with edge AI provider Kneron Holding Corporation aligns with tech sector growth trends, risks related to deal completion and regulatory compliance persist. Monitoring forthcoming filings and shareholder redemption activities will be essential to gauge the culmination of the business combination process.

Financial Trajectory and Performance Drivers to Date

Spark I Acquisition Corp's recent financial results encapsulate common pre-combination SPAC dynamics marked by increasing operating losses and strained liquidity. In fiscal year 2025, the company reported a net income of approximately $294 thousand — down dramatically from $3.15 million in 2024, amounting to a decline of roughly 90.7% year-over-year [F1]. This precipitous drop stems from escalating administrative expenses typical for SPACs in their operational phase before completing a merger.

Operating cash flow worsened by about 31.7% over the same period, descending from negative $1.87 million in FY2024 to negative $2.46 million in FY2025 [F1]. This reflects sustained cash burn associated with ongoing legal, advisory, and compliance costs.

Equity has concurrently deteriorated markedly from approximately negative $4.37 million at end-2024 to negative $7.15 million at end-2025 [F1]. Such negative equity signals accumulated deficit pressures as liabilities—particularly current liabilities—have mounted.

The company's current ratio highlights acute short-term liquidity constraints: with current assets at about $193 thousand against more than $3.84 million of current liabilities at fiscal year-end 2025, the ratio stood near an alarmingly low 0.05 [F1]. This imbalance suggests an urgent dependence on external capital injections for working capital continuity.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 0 | -2 | -90.7% |

| 2024 | 3 | -2 | +531.0% |

| 2023 | -1 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -4.1 |

| 2024 | -72.1 |

| 2023 | 32.2 |

Source: SEC companyfacts cache [F1].

Table: Spark I Acquisition Corp Historical Performance Snapshot (FY2023-FY2025) [F1]

Notably, substantial shareholder redemptions have depleted trust account funds earmarked for deal financing—this dynamic compounds fiscal stress ahead of any transaction consummation [S12][S13].

Sponsor Funding Role and Liquidity Position

Given the stark liquidity mismatch evidenced by current assets vis-à-vis liabilities around the close of FY2025 [F1], Spark I Acquisition Corp has leaned heavily on its sponsor for funding support through a promissory note arrangement engineered in conjunction with a shareholder-approved extension.

As disclosed on June 27, 2025 [S10][S11], the sponsor agreed to make monthly infusions into the SPAC’s trust account at a rate equating to $0.015 per outstanding Class A ordinary share capped at $55,000 per month up to an aggregate maximum of $825,000. These contributions are credited against a non-interest bearing unsecured promissory note payable upon maturity — either when a business combination is consummated or by September 29, 2026 if no deal closes [S10].

The promissory note structure allows for additional discretionary drawdowns up to $2.5 million minus prior contributions to meet working capital demands but bears no interest and can be prepaid without penalty at any time [S10][S15]. This flexibility mitigates immediate liquidity risks but underscores reliance on sponsor goodwill given limited internal cash reserves alone (~$112k at fiscal-end 2025) relative to >$3.8 million in current liabilities [F1].

In sum, this arrangement effectively bridges operational gaps during SPAC lifecycle closure uncertainty but highlights acute sensitivity to timely business combination resolution or interim capital availability.

Evaluating the Business Combination Timeline Extension

Originally mandated under its memorandum and articles of association to complete a business combination by July 11, 2025, Spark I Acquisition Corp successfully obtained shareholder approval on July 8, 2025 to extend this deadline through September 29, 2026 [S10][S13][S14].

The vote was significantly attended with approximately 90% shareholder quorum; however nearly one-third opposed or abstained indicating some shareholder reticence regarding delay [S13]. Post-approval redemptions ensued where holders of about 7.76 million Class A shares redeemed their interests for approximately $84.8 million cash withdrawn from the trust account—removing a substantial funding tranche from potential transaction financing [S12][S13].

This extension was pivotal in enabling negotiations toward finalizing a binding agreement with Kneron Holding Corporation while supporting incremental sponsor funding via promissory notes keyed off this prolonged window [S10][S15]. It also buys time for regulatory approvals but simultaneously elevates risk exposure given ongoing costs and shareholder attrition.

Understanding the Target: Kneron Holding Corporation and Market Context

While direct company disclosures provide limited detail beyond acknowledging Kneron as Spark I’s primary prospective merger candidate [N/A], Kneron is established within the specialized segment of edge artificial intelligence solutions offering hardware-software integration focused on AI silicon chips and firmware optimized for inference tasks deployed across IoT devices.

This market niche aligns favorably with secular technological trends emphasizing decentralized AI computation close to data sources reducing latency and power consumption—a fundamental shift underpinning growing interest among chip makers able to monetize low-power edge inference capabilities.

Kneron’s profile complements this trajectory serving growing demand sectors ranging from smart cameras and wearables to automotive applications where embedded AI interpretation is paramount.

Consequently, Spark I’s targeting of Kneron situates its business combination strategy within an emerging high-growth technology universe rather than more commoditized sectors prone to margin compression.

Capital Allocation Review: Structure, Dividends, and Returns Considerations

Consistent with typical SPAC practice prior to transactional closure—or in some cases absence thereof—Spark I Acquisition Corp has neither declared dividends nor engaged in share repurchase programs during FY2023-FY2025 [F1][S12][S14]. Its capital allocation focus has naturally centered on maintaining viability until completing its identified business combination.

On July 9, 2025 following shareholder approval of timeline extension proposals involving conversion mechanics totaling four million Class B ordinary shares into Class A shares issued directly to the sponsor reflects adjustments consolidating equity structure aligned with governance protocols necessitated prior to merging operations [S14][S22].

Approximated return on equity based on latest annual net income (~$294k) against negative equity balances (-$7.15 million) equates broadly to negative ~4.1%, emblematic not only of operational losses but also significant accumulated deficits embedded within Spark I’s shell-stage balance sheet carrying costs dominant over earnings generation potential absent consummation events that would dilute or profoundly shift this baseline metric [F1].

Key Risks and Regulatory Factors Impacting Completion

Risk disclosures articulate fundamental hazards centered chiefly upon failure to consummate an initial business combination within contractual deadlines—a scenario exposing holders potentially to liquidation preferences or loss of invested value absent alternative recourse measures [S4][S5][S6].

Other material risks include fragmented shareholder support evidenced through sizeable redemptions that reduce overall trust account balances available for merger proceeds while heightening uncertainty over approval thresholds required at subsequent voting stages [S16]. Compliance complexities connected with maintaining Nasdaq listing standards—such as timely annual meeting obligations recently challenged per Nasdaq notifications—add further strain demanding strategic remediation plans [S25].

Moreover, Spark I’s Cayman Islands incorporation brings layered statutory nuances regulating corporate governance standards influencing transactional timing and reporting obligations.

Legal proceedings referenced remain limited but any protracted litigation surrounding deal terms or regulatory scrutiny could impair momentum.[S4]

Outlook for Completion Milestones and Market Watchpoints

Absent explicit forward guidance filed by Spark I Acquisition Corp regarding precise expected dates for definitive agreements or close events with Kneron or alternate targets—as typical remains reasonable given inherent SPAC deal negotiation opacity—the primary market watchpoints lie in:

- Updates filed via SEC Form 8-Ks disclosing material definitive agreements,

- Announcements concerning incremental sponsor funding draws or amendments,

- Public communication surrounding evolving levels of shareholder redemption activity post-approval,

- Company disclosures addressing Nasdaq compliance plans related to shareholder meeting timing,

- Any emerging legal developments potentially impacting transaction clearance.

For market participants tracking Spark I's next chapter transitionally positioned from blank check entity toward operating platform dependent fundamentally on closing conditions and regulatory approvals—that are yet fluid—continuous diligence around these filings is prudent.

This analysis synthesizes disclosed financial data extracted primarily from SEC filings through fiscal year-end March-April 2026 aligned with Valye News’ editorial standards ensuring factual rigor without speculative valuation commentary or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments