BioScience Health Innovations Accelerates Revenue Through Patent-Backed Wellness Products Amid Capital Constraints

BHIC’s rapid growth, driven by patented mitochondrial health formulations and digital sales channels, is tempered by liquidity challenges.

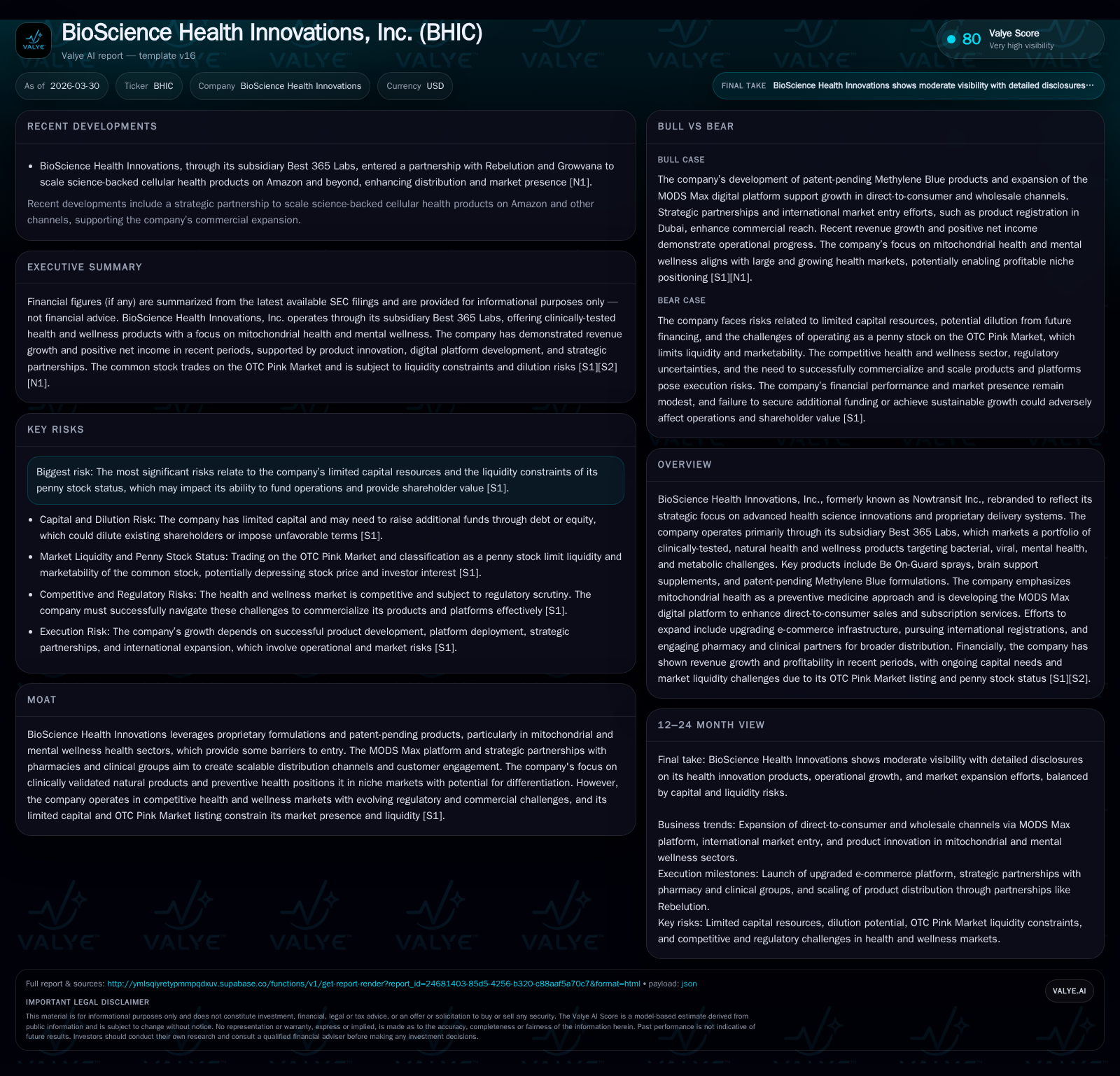

BioScience Health Innovations, Inc. has transformed its operations post-rebrand to focus on niche natural health solutions emphasizing mitochondrial and mental wellness. The company’s revenue surged over 200% in 2025, supported by Best 365 Labs’ product portfolio and the MODS Max platform aimed at enhancing customer engagement and subscription services. While profitability has been achieved on a modest scale with clear margin advantages, BHIC faces pronounced liquidity and capital constraints reflective of its OTC Pink Market status and limited investor base. Management’s near-term priorities include scaling e-commerce infrastructure, pursuing international market registrations, and reinforcing strategic partnerships without dilutive financing complications.

Company Background and Business Model

BioScience Health Innovations, Inc. (BHIC), formerly Nowtransit Inc., repositioned itself around advanced health sciences with an emphasis on natural health and wellness products via its subsidiary Best 365 Labs [S1]. The product suite targets bacterial, viral, metabolic, and mental health challenges using proprietary formulations centered on mitochondrial health—a growing preventive medicine focus—alongside patent-pending methylene blue formulations contributing additional technological differentiation.

A key strategic pillar is the MODS Max digital platform designed to foster direct-to-consumer (DTC) sales and subscription monetization. Alongside this platform development, BHIC is upgrading its e-commerce website integrating NetSuite for streamlined operations and financial management [S13]. This modernization supports scalable distribution models extending into wholesale pharmacy networks and clinical partnerships.

Historical Financial Performance

BHIC has demonstrated explosive top-line growth since commencing meaningful operations post-rebrand:

Historical performance (annual)

| FY | Rev ($mm) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 6 | 642090 | 172178 | 719051 | +208.3% | +638.0% |

| 2024 | 2 | 87000 | 23188 | 87000 | +208.7% | +134.6% |

| 2023 | 1 | -251500 | -307842 | -251500 | -202.3% | |

| 2022 | 0 | -83208 | -85782 | -91921 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 43.5 |

| 2024 | 10.4 |

| 2023 | 3720.4 |

| 2022 | -578.1 |

Source: SEC companyfacts cache [F1].

Data sourced from filings [F1]. Revenue growth accelerated dramatically post-2023 as commercialization efforts took hold. Operating income shifted from sizable losses toward positive margins, with net income mirroring this trend.

Margins have progressively improved through targeted marketing campaigns leveraging the MODS Max platform alongside wholesale channel expansions into over two thousand clinics [S13]. The focus on high-margin subscription packs delivered via direct web sales supports reported average gross margins exceeding 65%, a notable accomplishment within the natural products space where margin compression often pressures profitability.

Future Growth Prospects

Growth drivers in BHIC's outlook include:

- Expansion of Proprietary Product Lines: Continued R&D investment underpins an extensive patent portfolio covering oral methylene blue stabilization and catalytic ATP loop technologies that grant exclusivity potentially through the decade’s end [S15].

- Digital Platform Scaling: Enhanced functionality within MODS Max coupled with a revamped retail/wholesale website aims to accelerate DTC acquisition and retention while supporting recurring revenue streams through subscriptions [N1][S13].

- Wholesale Channel Penetration: Active negotiations with pharmacy chains and specialty clinical partners target licensing/co-branding agreements, offering sustainable baseline revenues beyond online channels [S13].

- International Market Registrations: Preliminary regulatory submissions in markets like Dubai open avenues for Middle Eastern distribution partnerships aligned with global expansion ambitions [S13].

Potential constraints could stem from:

- Limited capital availability restricting marketing spend or technology investment pace.

- Regulatory hurdles inherent in nutraceuticals compounded by evolving FDA policies.

- Intense competition within the burgeoning but fragmented natural wellness sector requiring sustained innovation.

Forecasts and Milestones

While no formal guidance is stated explicitly in public filings or news releases beyond operational updates [S1][N1], watchpoints include:

- Launch of the upgraded best365labs.com site projected around August 2025 to bolster ecommerce efficiency.

- Progression of international registrations particularly relating to Dubai market entry.

- Expansion benchmarks involving securing pharmacy group partnerships integrating MODS Max functionalities.

- Development milestones related to pending patent grants providing enhanced commercial protections.

Internally management stresses innovation-led growth combined with capital structure optimization as core tenets fueling projected year-over-year revenue increases in the range of mid-30% to high-40% through the remainder of the decade [S27].

Returns and Capital Allocation

BHIC has generated positive net income ($642K) alongside operating cash flow improvements ($172K) by fiscal year-end December 31, 2025 following several years of negative cash flows attributed initially to startup costs and working capital buildup [F1]. The company’s equity base expanded robustly from a near break-even position at end-2023 to approximately $1.48 million at end-2025.

An approximate return on equity stands near 43.5%, indicative of improved capital efficiency as commercial operations scale [F1]. However, BHIC currently pays no dividends nor reports share repurchase activity; capital management prioritizes reinvestment into growth initiatives and addressing liquidity needs through related-party financing arrangements rather than external debt or wide equity issuance [S26].

Notably, advances totalling over $2.4 million during the first nine months of 2025 were provided predominantly by Ageless Holdings LLC, an entity closely tied to management interests. While such related-party funding underscores insider confidence it also reflects constrained access to broad institutional capital markets given the company’s OTC Pink stock listing status [S26][S9].

Risks and Challenges

Liquidity remains BHIC’s principal risk factor with substantial reliance on affiliated entities for operational funding documented over multiple quarterly filings [S1][S5][S21]. Despite recent positive earnings trends, sustaining operations without dilutive securities offerings presents ongoing challenges compounded by volatile penny stock trading dynamics characterized by limited public float (approximately 11M shares outstanding post-reverse split) and sparse analyst coverage [S9].

Internal control weaknesses identified around accounting resource adequacy, segregation of duties, board independence, and policy documentation also highlight governance gaps necessitating remediation ahead of any uplisting attempts or enhanced compliance demands [S11][S17].

Regulatory risk persists given complex FDA frameworks governing natural health products that could impact commercialization timelines or impose additional compliance costs [S23]. Nonetheless, management emphasizes robust safety protocols for their proprietary delivery systems designed to mitigate oxidative stress-related adverse effects backing product claims with clinical validation studies.

Industry Context (Analysis)

The natural health product segment increasingly converges with biotechnological innovations focusing on mitochondrial wellness—a scientifically emergent but rapidly growing domain intersecting nutrition science with prevention medicine. BHIC's integration of biologically active mineral oxides such as methylene blue delivers a unique proposition distinct from conventional supplement offerings by enhancing cellular bioenergetics. Such technical sophistication facilitates potential regulatory classification advantages compared with pure nutraceuticals subjected only to dietary supplement standards.

The proliferation of digital health platforms enabling personalized supplementation regimens aligns well with consumer trends favoring convenience-based subscription models over one-time purchases—a dynamic BHIC seeks to capitalize on via MODS Max. Moreover, partnerships with pharmacies introducing liquid formulations through co-branding can bridge traditional retail limitations common among startups combating market fragmentation.

Conclusion

BioScience Health Innovations presents a compelling profile characterized by remarkable revenue acceleration fueled by innovative mitochondrial-centered formulations protected under pending patents. The company leverages a multi-channel commercial approach combining advanced digital platforms and nascent wholesale relationships enhancing future scalability prospects.

Nevertheless, BHIC operates within well-defined constraints relating primarily to limited financial resources typical of microcap entities whose OTC Pink market presence restricts liquidity horizons. Operational progress will hinge critically on successful execution of ecommerce enhancements, patent finalizations, international expansions, and governance strengthening necessary for future public market upgrades.

Investors monitoring BHIC should focus on confirmed patent grants milestones, uptake velocity within subscription programs powered by MODS Max technology, traction within international distribution pathways particularly Middle Eastern expansions, shifts in liquidity profile driven by capital raises or debt structuring alternatives, alongside improvements in internal control frameworks that underpin sustainable corporate governance advancement.

Disclaimer: This analysis is provided for informational purposes solely. It does not constitute investment advice or recommendations regarding any securities mentioned.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments