Kenon Holdings Shifts Energy Strategy with Asset Expansion and Capital Efficiency

Kenon leverages its dual geographic power assets while navigating capital-intensive growth and financing constraints.

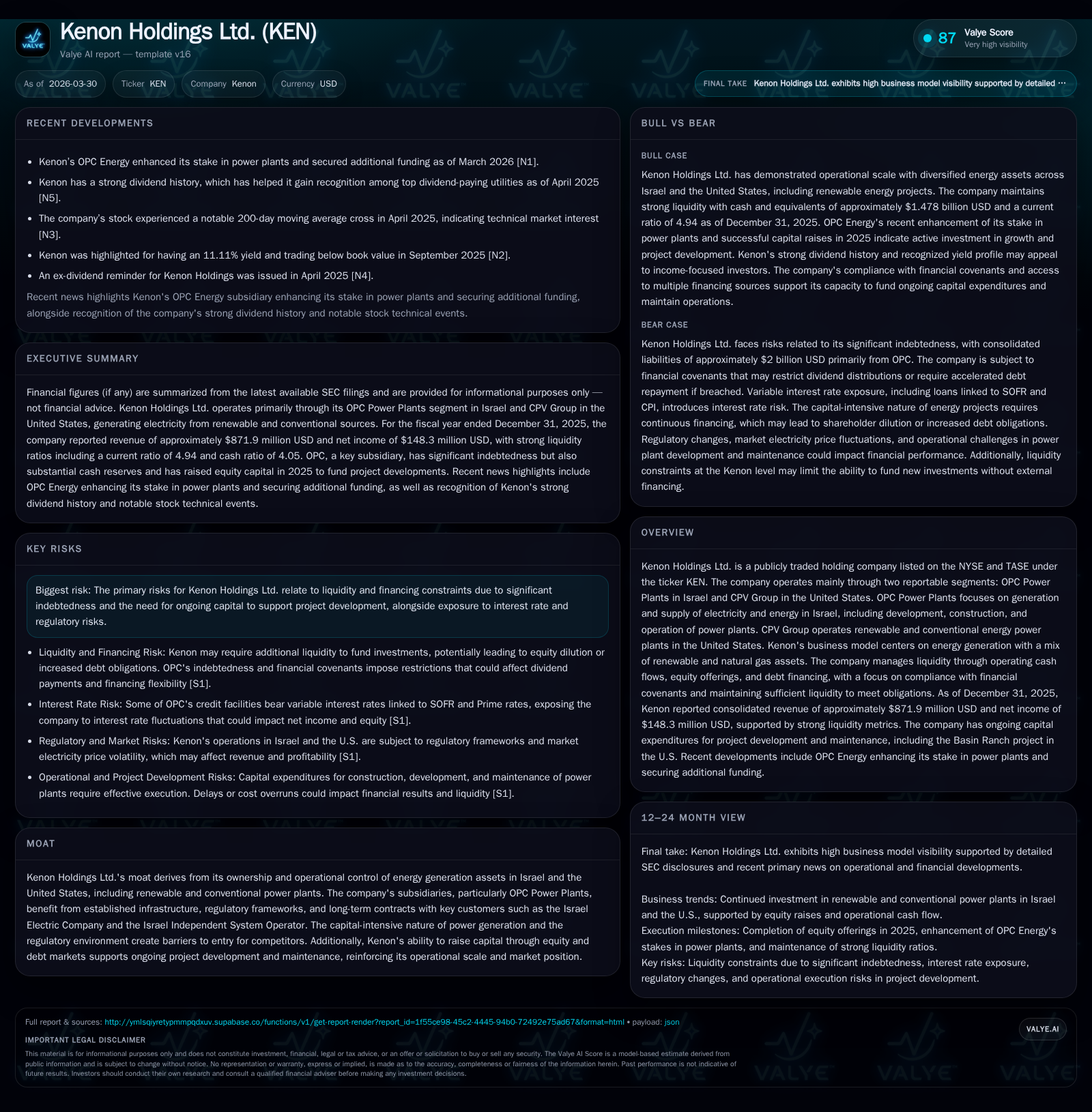

Kenon Holdings Ltd. reported strong revenue growth driven by its core OPC Power Plants in Israel and CPV Group renewables in the U.S., reaching $872 million in 2025, a 16.1% increase from 2024. Despite a sharp net income decline to $148 million due to investment and operational costs, the company maintains a solid liquidity position with increasing cash reserves and ongoing capital raises. Kenon's future expansion hinges on strategic project developments like Basin Ranch and Hadera 2, balanced against significant indebtedness and geopolitical risks that pressure financing flexibility. Its disciplined capital allocation includes growing dividends and share repurchases, underpinning a moderate approximate ROE of 4.7%.

Kenon's Revenue Growth Fueled by Dual-Region Energy Assets

Kenon Holdings Ltd., operating primarily through OPC Power Plants in Israel and CPV Group in the United States, has demonstrated robust consolidated revenue growth over recent years. The company achieved revenues of approximately $871.9 million for FY2025, marking a notable 16.1% increase from $751.3 million in FY2024 [F1]. This escalation reflects strong performance within its core energy generation segments—Israel’s OPC Power Plants contributed a dominant majority ($674.6 million), while the U.S.-based CPV Group saw revenue nearly double to $197.3 million [S14]. The diversified energy portfolio combining conventional gas-fired facilities with renewable projects underpins the upward trend in top-line, benefitting from growing electricity demand and utility contracts.

Key Drivers Behind Historic Financial Performance

The enhanced revenue stems from several sector-specific drivers: Recent tariff adjustments in Israel set the generation component at NIS 0.2890 per kWh for 2026, representing a slight decline but offset by volume growth [S1]. Meanwhile, natural gas cost fluctuations have materially impacted cost of sales, reflecting broader commodity price cycles [S1]. Expansion initiatives such as the Hadera 2 development project have entailed significant upfront expenditures impacting net profitability.

Despite rising revenues, net income contracted sharply from $634 million in FY2024 to $148 million in FY2025, a decline of 76.6% [F1]. This volatility largely reflects higher financing costs tied to recent capital raises and investments, combined with non-recurring expenses including impairments related to geopolitical disruptions [S1]. OPC’s operational continuity was affected by regional security incidents (e.g., Operation Rising Lion) which delayed equipment arrivals and plant maintenance—factors that temporarily elevated operational costs [S1].

Operational Challenges: Geopolitical and Market Price Pressures

Kenon's Israeli operations face considerable headwinds from continuing geopolitical risks involving Iran-linked conflicts which hinder supply chain reliability and increase insurance premiums [S1]. Inflationary pressure within Israel also influences interest rates on outstanding debt instruments, adding layers of financial stress [S1]. The company explicitly flags these issues as risk factors impacting project timelines and overall asset utilization.

In the U.S., power markets remain competitive with pricing sensitivity to SOFR-based interest rates affecting CPV's financing structures [S19]. Securing long-term off-take agreements remains critical given evolving regulatory frameworks around renewable power assets.

Future Growth Prospects Anchored on Project Development

Kenon's growth strategy involves deepening stakes in existing power plants through OPC alongside advancing new renewable projects such as Basin Ranch—a key initiative commencing construction in 2025 aimed at expanding CPV's portfolio of sustainable assets [N1][S1]. These initiatives align with broader energy transition trends yet require substantial capital commitments given the capital-intensive nature of utility-scale power generation.

The company acknowledges that fulfilling these plans demands ongoing equity infusions and debt financing, underscoring an investment-grade focus on maintaining covenant compliance while optimizing liquidity [S17][N1]. The balance between pursuing greenfield projects amid volatile macroeconomic conditions defines Kenon's near-term growth trajectory.

Constraints from Financing Needs and Security Risks

As of end-2025, consolidated indebtedness aggregated roughly $1.77 billion, comprising short-term obligations of $117 million and long-term borrowings around $1.65 billion [S9][F1][S10]. Kenon operates under numerous restrictive covenants including negative pledges, limitations on distributions, change-of-control clauses, and minimum financial ratio maintenance particularly within OPC entities [S10][S11].

Additional challenges arise from international credit exposure caps affecting Israeli banking syndicates lending capacity due to conglomerate credit limits tied to controlling shareholders [S10]. Higher interest rates linked to inflationary trends also increase debt servicing burdens.

Capital Allocation: Dividends, Share Repurchases, and Returns

Kenon has deployed capital prudently despite high leverage; dividends paid out rose progressively from approximately $150 million in 2023 to nearly $268 million in 2025 [F1][S6][S15], reflecting management’s commitment to shareholder returns within distributable reserve constraints imposed by Singapore corporate law [S6]. Concurrently, share repurchase activities under an open market program amounted to roughly $10 million worth of stock cancellations during 2025, totaling about 301 thousand shares repurchased [S5][S7][F1].

The company’s approximate return on equity stood at about 4.7% for FY2025 calculated using net income of $148 million against equity of $3.18 billion [F1], below sector averages typically seen in regulated utilities but indicative of current reinvestment phase dynamics.

Liquidity and Balance Sheet Analysis Amid Increasing Cash Position

Cash and equivalents reached an impressive $1.48 billion by December 31, 2025 up from just over $1 billion at prior year-end [F1][S1], supporting a healthy current ratio near 4.94 which implies sufficient working capital buffer against liabilities of $365 million [F1]. Operating cash flows grew meaningfully within OPC’s core business ($295 million vs. $207 million prior year) contributing positively despite heavy investing activity amounting to circa $362 million spent largely on new project infrastructure [S1]. Financing inflows surged largely driven by multiple equity offerings raising over half a billion dollars combined through Q2-Q4 private placements supporting development capital requirements for Basin Ranch among others [S17][N1][S25].

This liquidity cushion positions Kenon well for short-term obligations but highlights reliance on executing planned capital raises given ongoing capex commitments.

Historical Performance Summary (USD Millions)

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 872 | 148 | +16.1% | -76.6% |

| 2024 | 751 | 634 | +8.6% | +400.6% |

| 2023 | 692 | -211 | +20.5% | -160.3% |

| 2022 | 574 | 350 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 268 | 4.7 |

| 2024 | 201 | 23.8 |

| 2023 | 150 | -10.2 |

| 2022 | 299 | 15.2 |

Source: SEC companyfacts cache [F1].

What to Watch: Milestones, Funding, and Project Timelines

Looking forward, investors should monitor progress on key project milestones such as commercial commissioning of Hadera 2 in Israel and construction advancements at Basin Ranch in the U.S., along with subsequent financing tranches or equity offerings necessary to maintain momentum [N1][S1]. Regulatory decisions regarding electricity tariffs or approval delays could materially affect revenue streams.

Liquidity management remains critical given geopolitical uncertainties impacting supply chain continuity and inflation-driven cost escalations that could pressure debt service coverage ratios beyond existing forecasts. Furthermore, outcomes of contract renewals with primary customers like the Israel Electric Company will inform sustainability of OPC’s cash flows.

Continuous scrutiny of covenant compliance indicators across both Israeli and U.S. financings is advisable as missed thresholds may constrain future flexibility or trigger default scenarios.

This analysis is based solely on publicly available information including Kenon Holdings’ SEC filings and recent industry news up to March 30, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments