Inhibitor Therapeutics’ Financial Stress and Regulatory Hurdles Limit Growth Visibility

Clinical-stage Inhibitor Therapeutics continues pre-revenue development of itraconazole-based cancer therapies amid operational and patent risks.

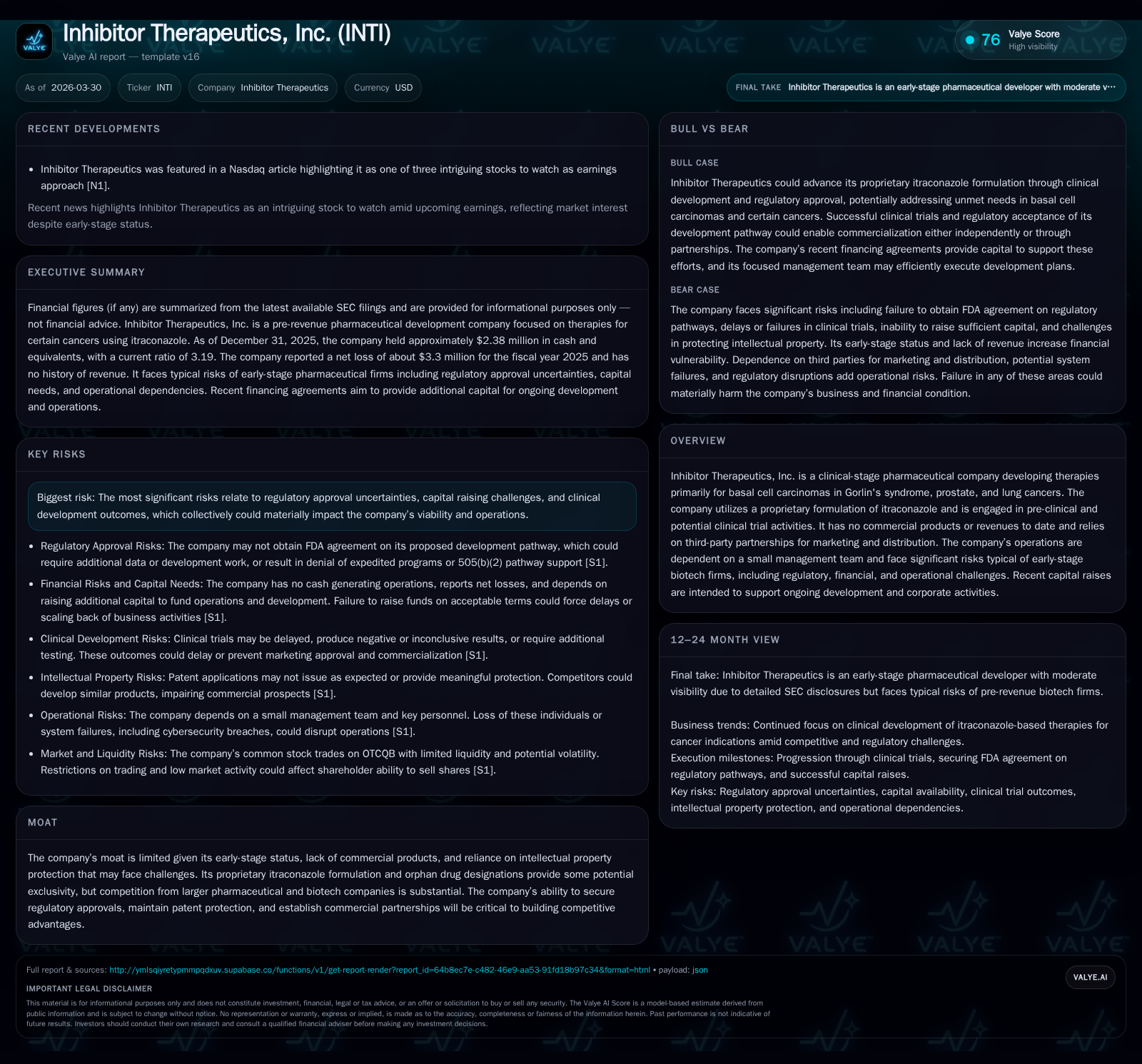

Inhibitor Therapeutics, Inc. remains an early-stage pharmaceutical firm focused on developing itraconazole formulations for basal cell carcinomas and cancers such as prostate and lung. Despite orphan drug designations providing some intellectual property protection, the company faces significant regulatory uncertainty, patent litigation risk, and capital constraints with no revenues to date. Sustained operating losses have eroded equity liquidity, culminating in a negative net equity position by end-2025. Future growth hinges on FDA progress, successful clinical outcomes, and securing strategic partnerships amid an increasingly competitive oncology market.

Company Overview

Inhibitor Therapeutics, Inc. is a clinical-stage pharmaceutical company primarily engaged in developing therapies targeting basal cell carcinoma nevus syndrome (BCCNS), along with prostate and lung cancers. Its core innovation lies in a proprietary reformulation of itraconazole, an antifungal agent repositioned for anticancer utility. The company’s focus has evolved around leveraging orphan drug designations to aid exclusivity for its niche indications. However, no products have yet reached commercialization, with operations focused on preclinical development and potential clinical trial readiness [S1].

Historical Performance

Inhibitor Therapeutics exhibits a classic early-stage biotech financial profile characterized by zero revenues since at least 2017 through 2021 [F1]. Operating losses have been persistent and growing in magnitude: from approximately $658K in FY2022 to over $3.4 million by FY2025 [F1]. Negative net income closely tracks these operating losses, highlighting limited non-operational income sources. Cash flow from operations is similarly negative - nearly $3.2 million outflow in 2025 - reflecting ongoing R&D expenditure without offsetting inflows [F1].

The equity base deteriorated significantly from a positive $8.3 million at the end of FY2022 down to negative $1.3 million by FY2025 [F1]. This erosion signals cumulative losses exceeding invested capital or dilution accompanied by increases in liabilities. Importantly, the company’s current ratio stands robust at approximately 3.19x, suggesting current asset coverage exceeds liabilities but potentially driven by recently raised capital restricted for near-term use [F1][S16].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -3 | -3 | -3 | +1.2% |

| 2024 | -3 | -3 | -4 | -10.3% |

| 2023 | -3 | -3 | -3 | -125.0% |

| 2022 | 12 | 12 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 255.5 |

| 2024 | -168.2 |

| 2023 | -57.3 |

| 2022 | 145.9 |

Source: SEC companyfacts cache [F1].

*Note: FY2022 net income and CFO unusually positive likely due to non-routine transactions or reversals.

Growth Drivers and Constraints

Potential Catalysts

Growth prospects for Inhibitor Therapeutics depend heavily on progression through regulatory milestones and clinical validation of its itraconazole formulation’s efficacy across targeted oncology indications [S1][S14]. The company has engaged with the FDA via Type C meetings scoped towards convincing the agency of a streamlined approval pathway (505(b)(2)) leveraging prior data sets (HP2001). However, this pathway is not guaranteed; the FDA may require additional data or reject the proposed endpoints [S1].

Intellectual property protection based on orphan-drug status offers some market exclusivity advantages potentially extending into commercial phases if approvals are achieved [S1][S6]. Establishing third-party collaborations for commercialization could accelerate market access while reducing upfront capital expenditures given the absence of internal sales/marketing infrastructure [S11][S16].

Constraints and Risks

Despite these prospects outlined by internal plans and regulatory interactions [S1], multiple barriers remain formidable:

- Regulatory approval timelines are uncertain with notable risks of rejection or demands for extended studies.

- The proprietary formulation's patents may face challenges including narrower claims than expected or litigation that could diminish exclusivity [S6][S8][S9].

- Competition from well-financed global pharmaceutical companies working on similar cancer targets presents constant pressure [S11][S22].

- Financial resources remain constrained; recent capital raises totaling roughly $3 million with potential follow-ons reflect funding needs but face execution uncertainty [S16].

- Dependency on a small management team increases operational risk; loss of key personnel could materially hamper execution capability [S27].

- Lack of product liability insurance presently exposes the firm to unmitigated risks during trials or after commercialization efforts [S6].

- Market acceptance uncertainties include pricing negotiations and reimbursement from payors which may impact commercial viability despite approval success [S15].

Capital Allocation and Financial Outlook

Inhibitor Therapeutics has not paid dividends since at least FY2019 nor does it have earnings enabling dividend distribution [F1]. Buybacks are not indicated given financial stress as evidenced by contractual equity issuance for needed liquidity via stock sales alongside warrants effective February 2026 raising an initial $3 million with an option for approximately $2.5 million more if exercised [S16][S3].

This injection partially alleviates immediate liquidity concerns but does not eliminate the company's reported substantial doubt regarding its ability to continue as a going concern absent further financings or strategic partnerships [S16]. Cash reserve levels are modest relative to ongoing burn rates.

No explicit revenue forecasts or commercial launch timelines have been disclosed by management or filings as of latest reports [S1][S2]. Monitoring FDA feedback on trial designs or acceptance along with news around licensing/collaborative arrangements will be critical indicators.

Summary Analysis

As a small-cap clinical-stage biotech focused on anticancer repurposing via itraconazole formulations targeting orphan indications such as Gorlin's syndrome BCCNS and select carcinomas, the company sits at a precarious inflection point typical within biopharma startups but amplified by its zero-revenue status heading into mid-2026. Capital preservation through equity raises is vital while pursuing regulatory clarity following Type C FDA engagements. Yet financial deterioration—negative equity—and continued losses underscore tight runway constraints. The patent landscape remains uncertain with potential litigation possibly diluting perceived moat value despite orphan-drug exclusivities. Operationally reliant on external partners for manufacturing and commercialization intensifies execution risk. Meanwhile competitive pressures from larger oncology players working on immunotherapies or targeted small molecules impose additional hurdles. Until confirmatory clinical data evidencing safety and efficacy accrues alongside firmer regulatory endorsement emerges, inherent volatility will likely persist in valuation sentiment around Inhibitor Therapeutics. Future breakthroughs or strategic partnerships could markedly alter prospects but require crossing several high-risk thresholds common in this sector. Investors should regard this profile as one emblematic of early-stage drug developers focusing mainly on pipeline advancement rather than near-term profitability.

This analysis is based solely on available financial data from SEC filings through March 26th 2026 [F1][S#] and publicly filed risk disclosures without speculative forecasts or price assessments. Readers should consider inherent uncertainties linked to biotechnology sector dynamics including developmental setbacks and regulatory outcomes when interpreting this report.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments