Noodles & Company Faces Revenue Shrinkage and Liquidity Stress in 2025

An analysis of NDLS's financial pressures and strategic responses amid intensifying competition in casual dining.

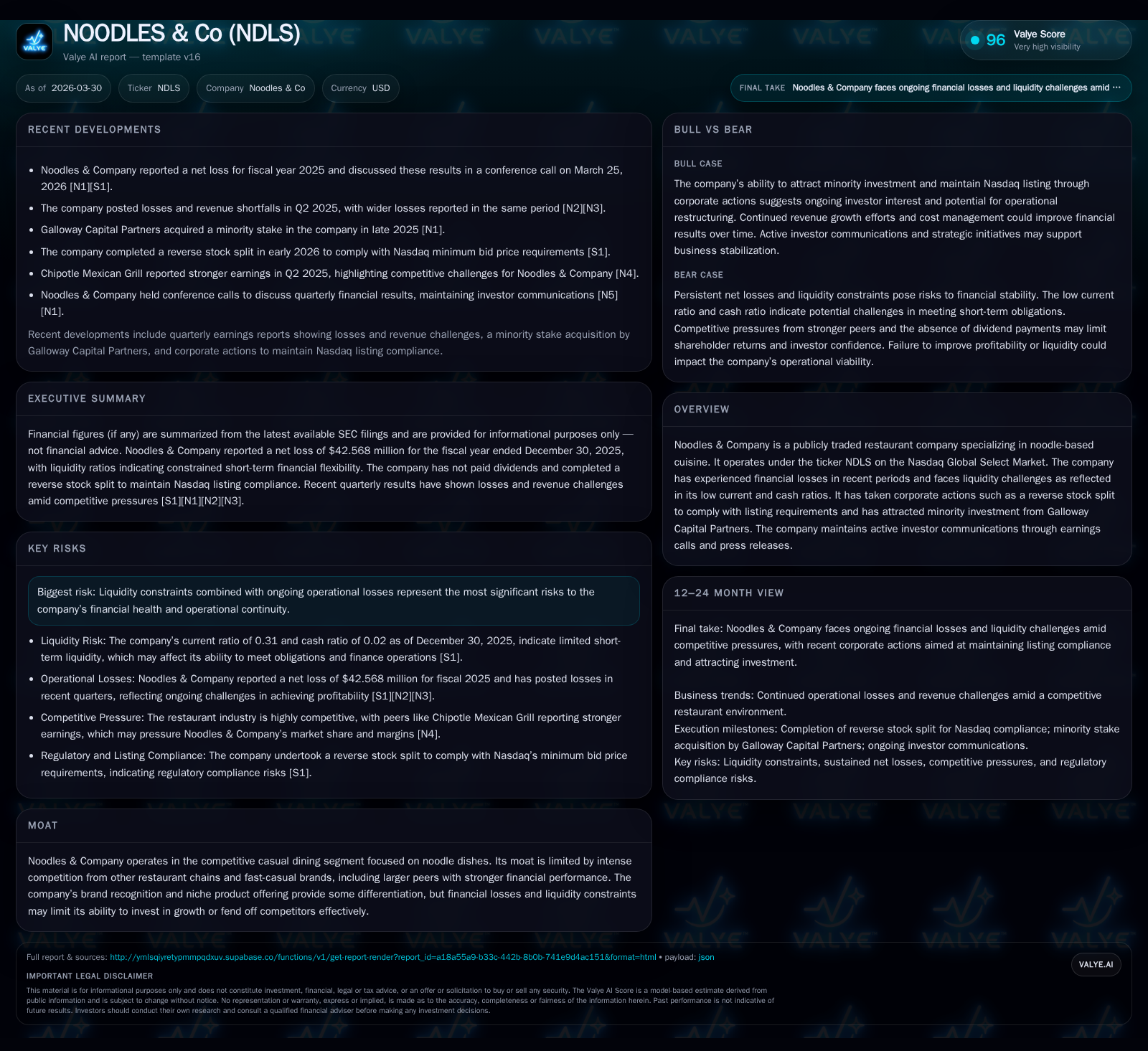

Noodles & Company experienced a significant contraction in revenue in 2025, with a nearly 13% year-over-year decline accompanied by mounting operating and net losses, despite maintaining positive operating cash flow. The company faced acute liquidity challenges, evidenced by a current ratio of approximately 0.31, prompting corporate actions including a reverse stock split to secure Nasdaq listing compliance. While its niche noodle-based offerings provide some differentiation, competitive pressures and financial constraints limit growth opportunities and capital allocation flexibility. Strategic efforts focus on stabilizing operations and navigating market demands within tight financial parameters.

Historical Performance: A Decline Despite Noodle Popularity

From fiscal year 2024 to 2025, Noodles & Company saw its revenues contract sharply by approximately 12.8%, sliding from levels seen in prior years that had shown some stability [F1]. This shrinkage culminated in a reported revenue figure of approximately $112.8 million for FY2025. Alongside top-line weakness, operating income remained mired in losses totaling $31.6 million—worsening by nearly 13.7% relative to the previous year [F1]. Net income followed this negative trajectory, with a steepening loss of $42.6 million that generated significant equity deficits resulting in negative shareholders' equity of approximately -$45.3 million [F1].

Despite these losses, operating cash flow remained positive at $7.3 million for the year, indicating disciplined working capital management amid earnings challenges [F1]. Capital expenditures markedly diminished by almost 57% compared to the prior year, reflective of restrained investment activity under liquidity pressure [F1]. These trends collectively reflect constrained operational leverage where fixed costs compress margins amid volume pressures.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -43 | 7 | -32 | 12 | -17.5% |

| 2024 | -36 | 8 | -28 | 29 | |

| 2022 | -3 | 10 | -1 | 34 | -190.4% |

| 2021 | 4 | 36 | 6 | 19 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -5 | 94.0 |

| 2024 | 0 | -21 | 649.1 |

| 2022 | -24 | -8.6 | |

| 2021 | 17 | 9.7 |

Source: SEC companyfacts cache [F1].

Table note: Revenue and income figures rounded to nearest hundred thousand USD; YoY calculations compare FY2025 vs FY2024 [F1].

Operational Drivers Behind Recent Results

The contraction in revenue during FY2025 appears linked to multiple operational headwinds detailed in recent earnings communications [N1][N2]. Shifts in product mix pressured average check sizes—a critical fast-casual sector metric—as inflationary impacts altered customer purchasing behavior and menu innovation lagged peers’ pace [N1]. Competitive dynamics intensified as larger casual dining chains expanded footprint and digital engagement capabilities, eroding Noodles & Company’s market share within its niche segment specializing in customizable noodle dishes.

Moreover, cost inflation, notably in labor and commodity inputs such as wheat and vegetable oils—staples for noodle preparation—further compressed margin profiles [N2]. The company’s modest scale limits negotiating power against suppliers compared to dominant chain peers, increasing cost pressures that outpaced pricing adjustments without risking customer attrition.

Same-store sales trends reportedly stagnated or declined slightly versus some fast casual peers gaining traction through loyalty programs and delivery channel enhancements [N1]. This underscores the challenge for NDLS to evolve its menu offerings rapidly while preserving operational efficiency amidst an intensifying sector promotional environment.

Liquidity Pressures and Market Compliance Actions

Liquidity emerged as the most pressing concern for Noodles & Company entering fiscal year-end with current assets amounting to roughly $18.9 million against current liabilities exceeding $61.8 million, resulting in a critically low current ratio near 0.31—a textbook liquidity squeeze scenario [F1]. Such imbalance signals tight short-term funding windows prone to stress from unforeseen outflows or delayed receivables.

To address imminent delisting risks tied to its common stock trading below Nasdaq’s mandated $1 minimum bid price threshold, NDLS executed a reverse stock split (eight-for-one) effective February 18, 2026 [S11][S13]. This corporate maneuver is intended purely as a listing compliance mechanism rather than a fundamental value driver but was essential to maintain market access.

The company has not declared or paid any dividends and does not anticipate doing so in the foreseeable future given its financial condition and credit facility restrictions [S1][S5]. There were no share repurchases during the fourth quarter of 2025 or the fiscal year [S1][F1]. Retained earnings are prioritized for debt reduction and operational financing.

Strategic Outlook: Growth Prospects Amid Competitive Casual Dining

Growth strategies disclosed emphasize leveraging brand recognition within noodle-centric casual dining while cautiously exploring menu diversification avenues presumed necessary to widen customer appeal beyond traditional staples [N1][S1]. Efforts reportedly include testing health-conscious options and expanding delivery capabilities; however, financial capacity limitations materially temper scale-up initiatives or technology investments requisite for competing effectively against large-scale operators.

Customer loyalty programs have been mentioned as potential drivers for repeat visitation but remain nascent relative to industry leaders deploying advanced CRM systems integrated with mobile ordering platforms [N1]. Given ongoing operating losses and constrained capital availability, aggressive marketing spend or new unit openings are unlikely near term without external capital infusion.

Sector competition with brands benefiting from multi-channel menus and established real estate footprints creates an encroaching environment requiring sharper differentiation strategies that NDLS must craft carefully while shoring up fundamentals.

Capital Allocation: Debt Management Over Dividends or Buybacks

Given the company's ongoing net losses, negative equity position, and restrictive credit covenants limiting discretionary capital deployment, NDLS has refrained from paying dividends or repurchasing shares [S5][F1]. The focus remains on retaining earnings or available cash flow resources for deleveraging and sustaining operations rather than returning capital to shareholders.

This conservative posture aligns with buy-side prudence emphasizing survival over expansion until liquidity position stabilizes adequately.

Near-Term Milestones and What to Monitor

Upcoming quarterly earnings disclosures will be critical checkpoints for liquidity improvement efforts including changes in working capital metrics such as accounts payable turnover and days sales outstanding [N1][S3]. Monitoring developments around Nasdaq listing compliance post-reverse split remains essential given historical breaches triggering uncertainty.

Key indicators warranting close surveillance include incremental movements in the current ratio above critical thresholds signaling alleviation of liquidity squeeze symptoms and trends toward normalized free cash flow generation after factoring capital expenditures which currently exceed operating cash flow margins negatively by approximately $5.1 million on a free cash flow basis for the latest fiscal year [F1].

Maintaining cautious capex discipline while driving margin recovery on same-store sales will be vital metrics alongside watchfulness for any shareholder proposals related to governance changes or further Nasdaq regulatory actions that could impose operational constraints [S4][S6].

Disclaimer: This analysis is based solely on publicly available information as of March 30, 2026, including SEC filings, earnings transcripts, press releases, and standardized financial data snapshots provided herein. It does not constitute investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments