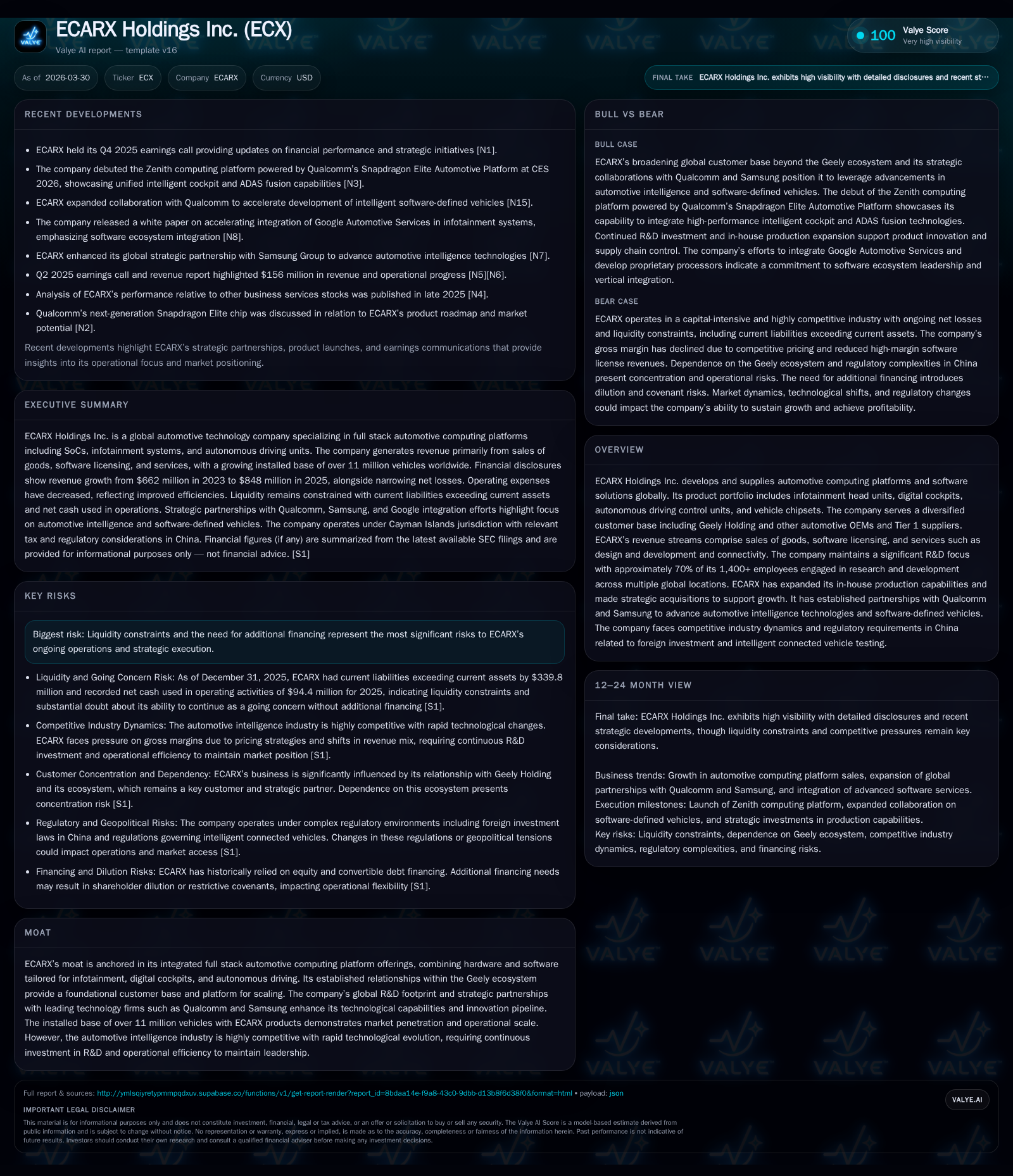

ECARX Holdings Inc. Shrinks Operating Loss While Managing Liquidity and Margin Pressure

ECARX Holdings advances automotive computing platforms amid competitive pressures and liquidity challenges.

ECARX Holdings Inc. (ECX) reported a narrower operating loss in fiscal 2025 driven by reduced operating expenses despite modest gross margin compression. Revenue growth from automotive computing platform sales was offset by declines in software licensing and service revenues. The firm continues to invest heavily in R&D with about 70% of its workforce dedicated to innovation, supported by strategic partnerships and acquisitions to bolster its production capabilities. Liquidity remains strained with negative cash flow from operations and a current ratio below one, highlighting ongoing financing needs to support growth. The company's integrated hardware-software stack and embedded position within the Geely ecosystem provide a foundation for future expansion, though competitive dynamics and funding risks persist.

Historical Performance and Financial Overview

ECARX Holdings Inc., a developer of integrated automotive computing platforms, reported marked improvements in its operating results for the fiscal year ended December 31, 2025 [F1], [S1]. The company narrowed its operating loss significantly to approximately $54.8 million in 2025, compared with a loss of $122.9 million in 2024—a reduction of about 55%. This improvement was driven primarily by a deliberate reduction in operating expenses including research and development (R&D) and selling general administrative (SG&A) costs [S13]. However, gross margin compressed from 20.8% in 2024 down to 19.0% in 2025 due mainly to the decline in higher-margin intellectual property licensing revenue within the software license segment [S4], [S13].

Revenue streams are diversified across sales of goods (automotive computing platforms), software licensing, and services encompassing development contracts and connectivity solutions [S4], [S25]. While sales volume of automotive computing products increased—helping retail revenue—both software license revenues (which fell from $42.5 million to $29.7 million) and service revenues experienced declines anchored by decreased contract completions during the period [S4]. Despite this mixed segment performance, gross profit rose marginally from $160.1 million in 2024 to $161.3 million, reflecting volume-driven gains somewhat offset by pricing pressure on key components like System-on-Chip (SoC) modules [S13].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -66 | -94 | -55 | 12 | +48.3% |

| 2024 | -128 | -59 | -121 | 16 | +3.5% |

| 2023 | -132 | -175 | -129 | 9 | +40.7% |

| 2022 | -223 | -59 | -213 | 19 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -107 | 23.4 |

| 2024 | -75 | 53.0 |

| 2023 | -184 | 102.0 |

| 2022 | -77 | 868.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY growth not explicitly provided; Buybacks indicate shares repurchased under authorized program.

Operational Progress and Cost Management

The cost structure evolved with cost of goods sold increasing due to higher sales volumes along with modest rise in design/development contract associated costs; simultaneously there was a softening of SoC core module expenditures reflecting product mix shifts [S4], [S7]. R&D expenses decreased substantially by nearly 29%, dropping from approximately $174.9 million in 2024 to $123.3 million in 2025 due to streamlined resource allocation amidst ongoing integration efforts [S13]. SG&A also reduced by about 13%, supporting overall expenditure control.

This tight management helped improve operational efficiency despite competitive pressures leading to margin erosion; operating losses shrank accordingly but remain significant as ECARX balances scaling investment versus short-term profitability goals.

Capital Allocation and Returns

Capital expenditure during the year was relatively modest at around $12.2 million compared to prior years reflecting measured investment choices aligned with R&D priorities and capacity-building initiatives such as development of the Hangzhou Fuyang production facility initiated mid-2024 and acquisition actions like Hubei Dongjun Automotive Electronic Technology Co., Ltd.[S22].

ECARX also engaged actively in capital return efforts through share repurchases totaling nearly 21.4 million shares authorized up until March 31, 2026 with actual purchases approximating $28 million at an average price near $1.35 per share during early-to-mid-2025 [S9], signaling confidence in equity value enhancement where feasible.

Financially however, ECARX remains constrained with cumulative net losses aggregating over one billion dollars since inception alongside a negative equity balance exceeding -$280 million as of end-2025 consistent with the company's ongoing investment phase aimed at capturing market share [F1]. Return on equity computed as net income over equity for fiscal year ends at positive percentages does not hold practical significance here given persistent negative equity.

Liquidity Position and Capital Structure Risks

Liquidity requires close monitoring given current assets at roughly $483 million contrasted sharply against current liabilities exceeding $823 million yielding a current ratio around only 0.59 as of late-2025—a continued indication that near-term obligations surpass working capital availability [F1], [S6], [S11].

The company generated negative cash flow from operations of approximately $94 million in latest fiscal year despite improved operating leverage vs prior periods where operational cash consumption was more severe; investing activities reflected increased outflows from investments primarily into debt securities and strategic stakes alongside moderate capital expenditures [S14], [S21]. Financing cash inflows were notably robust boosted by new equity raises totaling approximately $88 million including follow-on offerings and private placements with controlling shareholder Geely Investment Holding Ltd., as well as convertible note issuances supplementing working capital needs [S19], [S6].

ECARX benefits structurally from backing by Geely's ecosystem including related party loans bearing relatively low-interest rates (~3.9%), factoring arrangements linked to trade receivables within Geely's financial ecosystem, supporting operations but also creating interconnected financial dependencies that could amplify risk if market conditions worsen or industry disruptions occur [S24]. Continuing need for external financing beyond current facilities presents heightened execution risk for sustaining growth trajectory.

Industry Positioning and Future Growth Drivers

ECARX has successfully cultivated an integrated hardware-software stack targeting infotainment head units, digital cockpits, autonomous driving control units (ADCU), vehicle chipsets (SoCs), and core operating system platforms tailored toward software-defined vehicles—a segment growing rapidly as car manufacturers emphasize modularity and connected intelligence [N/A sector analysis]. Its moat is underpinned by deep integration within Geely's large vehicle manufacturing umbrella along with technology partnerships including Qualcomm and Samsung aimed at advancing automotive intelligence technologies at scale across global markets including Europe alongside China .[N/A analysis]

Over eleven million vehicles globally run on ECARX technology implicating significant operational scale; however, competition is fierce involving established tier-1 suppliers diversifying into intelligent cockpit systems plus specialized semiconductor vendors intensifying price pressure . Innovation cycles demand aggressive R&D funding which ECARX maintains consistently via ~70% employee allocation toward research functions across multinational sites embracing emerging tech trends such as autonomous driving enhancements.

Future growth hinges upon executing on scaling software licensing models tied to mass adoption of fully software-defined cars while defending hardware market share amidst commoditization risks; expansion beyond Geely-related customers towards broader OEMs represents an important avenue but requires navigating regulatory complexities especially related to China’s foreign investment environment plus international standards compliance regimes detailed in their filings [S10],.

Outlook Considerations

Though explicit forward guidance remains absent from disclosures,[N2]/[N3] market watchers should monitor several key milestones indicative of progress: tangible improvements in unit economics and margin stabilization beyond pricing pressures; successful broadening of customer base outside legacy Geely relationships; ongoing reductions or controlled increases in net cash burn shaping sustainable liquidity trajectories; continued ramp-up of proprietary SoC designs demonstrating technology leadership; potential further share repurchase activity signaling capital discipline.

However notable risks persist related to potential liquidity shortfalls requiring additional fundraising which could dilute ownership or constrain operational flexibility; competitive incursions eroding pricing power; regulatory scrutiny impacting cross-border operations particularly amidst evolving PRC foreign investment laws; along with product liability exposures intrinsic to automotive electronics markets subject to strict consumer safety enforcement regimes detailed extensively within SEC disclosures [S16],[S17],.

Conclusion

ECARX Holdings Inc.’s fiscal 2025 results illustrate a company gradually improving its operating efficiency while sustaining revenue momentum primarily through core automotive computing product sales despite ongoing challenges compressing margins and software segment revenues. The firm’s commitment to innovation and global R&D breadth supported by Geely affiliation provides foundational strengths amidst challenging industry dynamics.

Liquidity fragility remains a chief concern necessitating vigilant capital structure management alongside balanced growth investments. Market participants should watch execution against scaling software licensing models, margin restoration efforts amid component cost fluctuations, capital raise success or alternative credit sources underpinning working capital sufficiency.

While the company’s sizable installed base coupled with strategic partnerships furnishes opportunity for expansion into highly competitive automotive intelligence markets increasingly shaped by digital transformation demands, financial risks underscore the importance of monitoring evolving operational cash flow trends relative to financing availability in the coming periods.

Disclaimer: This report is intended for informational purposes only and does not constitute investment advice or recommendations regarding any securities discussed herein. Readers should consult their own advisors before making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments