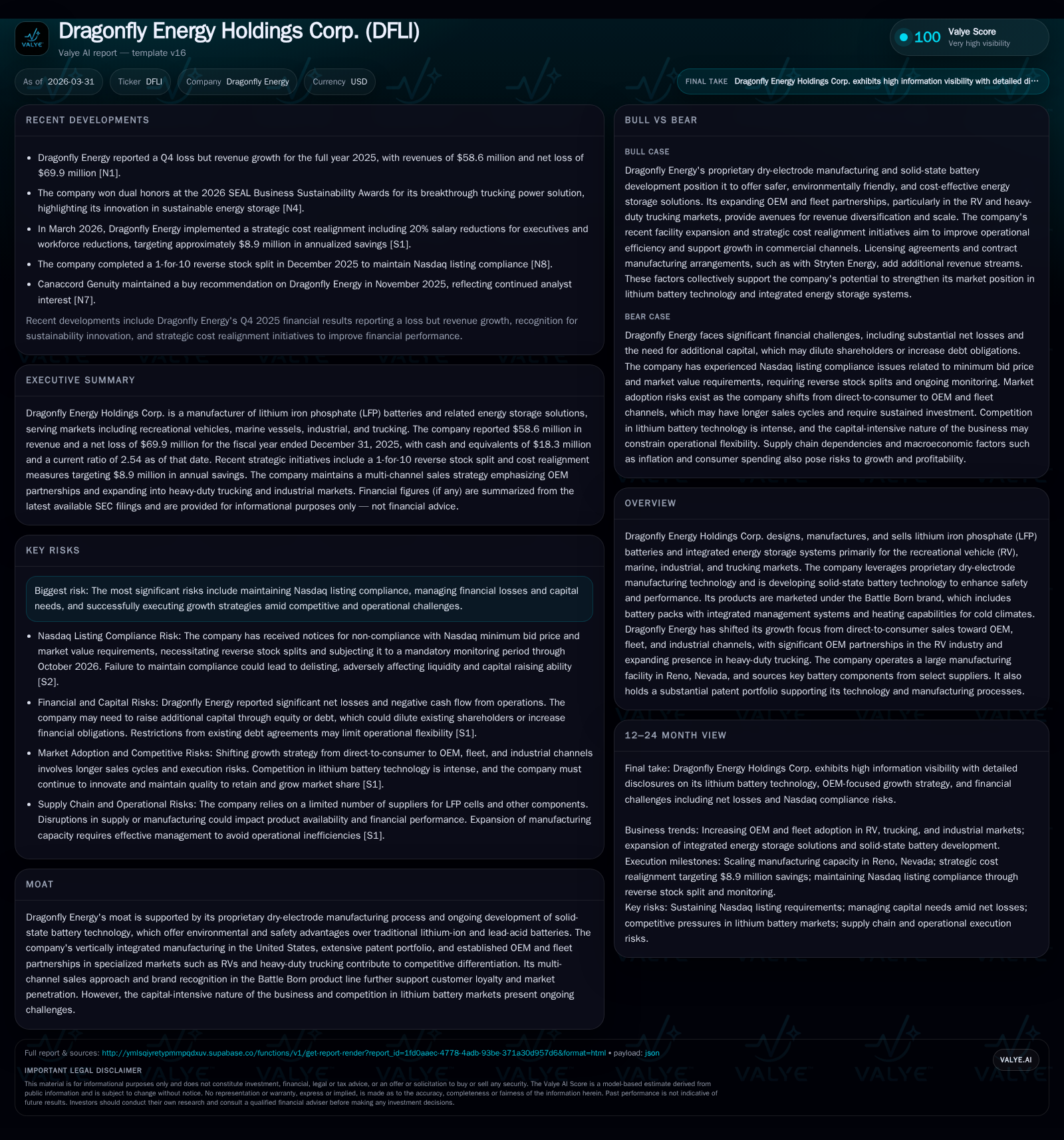

Dragonfly Energy’s Midstage Growth Marked by Technology Bets and Capital Constraints

Dragonfly Energy Holdings navigates evolving lithium iron phosphate battery markets with proprietary tech while managing heavy losses and liquidity risks.

Dragonfly Energy Holdings Corp. specializes in lithium iron phosphate (LFP) batteries catering primarily to recreational vehicles, marine, industrial, and trucking sectors. With a shift from direct-to-consumer sales towards OEM and fleet partnerships, notably in RVs and heavy-duty trucks, the company leverages unique dry-electrode manufacturing and developing solid-state technologies for differentiation. Despite revenue growth of nearly 16% in fiscal 2025 driven by expanded OEM relationships and product diversification, the company remains deep in losses with a widening net deficit and negative operating cash flow, reflecting capital-intensive R&D investments and operational expansion. Key risks include supplier concentration, reliance on a single manufacturing site, NASDAQ compliance challenges, ongoing litigation over product defects, and an uncertain ability to raise additional capital amid restrictive debt covenants.

Company Overview and Market Position

Dragonfly Energy Holdings Corp. develops lithium iron phosphate (LFP) battery solutions predominantly targeting specialized markets such as recreational vehicles (RVs), marine vessels, industrial applications, and increasingly, trucking fleets [S1][S8]. Their flagship brand, Battle Born Batteries, integrates proprietary features such as advanced battery management systems and cold-weather heating capabilities tailored for demanding use cases [S8][N1]. The company has consolidated its branding under Battle Born following prior use of dual brands to streamline market focus [S23].

Their technological edge is rooted in a patented dry-electrode manufacturing process that reduces environmental impact by eliminating solvent-based slurry coating steps common in conventional battery production [S15]. This method offers a smaller factory footprint, lower energy usage during electrode manufacture, and a reduced carbon footprint compared to traditional processes — advantages validated by third-party independent analysis [S15]. Dragonfly is also advancing next-generation solid-state battery technology expected to greatly enhance safety by removing liquid electrolytes prone to flammability while leveraging their scalable dry electrode approach [S1][S15].

The firm's vertically integrated U.S.-based manufacturing provides quality control benefits but concentrates risk exposure related to factory disruptions [S1]. Supplier dependence is also high: LFP cells come from only two suppliers, with battery management systems sourced from a single manufacturer [S1]. These factors remain potential operational constraints.

Historical Performance

Revenue growth has been steady yet modest relative to the scale needed for profitability. Fiscal 2025 revenue rose approximately 15.8% year-over-year to reach $58.63 million driven by increasing OEM adoption primarily in the RV segment — including a strategic partnership initiated in mid-2022 with THOR Industries — as well as expansion into trucking fleet markets [F1][S16][N1].

Despite top-line gains, Dragonfly remains deep in the red. Net losses widened sharply to nearly $69.9 million in 2025 compared to $40.6 million the prior year reflecting intensified spending on research & development for dry-electrode scaling and solid-state technology alongside costs associated with automating production facilities [F1][S15]. Operating income was negative $23.17 million but improved slightly from previous years' larger deficits [F1].

Cash flow trends mirror these results: operating cash flow was negative $25.97 million last fiscal year while capital expenditures dropped by roughly 29% year-over-year to $1.95 million as the company managed liquidity conservatively given capital needs [F1]. Equity increased to $11.53 million at end-2025 after equity raises linked to debt restructuring initiatives earlier that year [F1][S4][S5].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 59 | -70 | -26 | -23 | +15.8% | -72.2% |

| 2024 | 51 | -41 | -7 | -26 | -193.9% | |

| 2023 | -14 | -18 | -27 | +65.1% | ||

| 2022 | -40 | -46 | -34 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -28 | -606.6 |

| 2024 | -10 | 431.9 |

| 2023 | -25 | -49.5 |

| 2022 | -53 | -349.2 |

Source: SEC companyfacts cache [F1].

Table reflects reported financials where available; revenue only disclosed for last two full fiscal years.

Competitive Advantages and Moat

Dragonfly's core moat derives primarily from its patented dry electrode process which offers unique environmental benefits such as reduced energy consumption (71% less during electrode manufacture), elimination of toxic solvents like NMP (N-Methyl-2-pyrrolidone), smaller factory space needs (22% less), and lower carbon emissions compared to standard wet coating methods used widely in lithium-ion cell production [S15]. These attributes provide cost efficiency potential alongside sustainability—a key differentiator amid growing regulatory focus on green manufacturing practices.

Complementing this production edge is their extensive IP portfolio: over 50 issued patents internationally protecting aspects ranging from chemical compositions to manufacturing techniques plus nearly four dozen more pending globally across key regions including U.S., Europe, China, Korea, Japan and India [S10].

Brand recognition fostered through Battle Born's aftermarket presence supports strong OEM uptake especially within RV manufacturers such as THOR Industries who have fostered an exclusive regional distribution relationship expected to deepen over time [S16][S23]. Substantial growth prospects lie ahead due to increased lithium adoption over incumbent lead-acid alternatives driven by better cycle life, safety profiles (non-flammable chemistry), lighter weight, and system integration capabilities fueled by proprietary monitoring platforms like Dragonfly IntelLigence launched recently [S19][S21].

However, competition remains fierce involving traditional lead-acid producers with entrenched customer bases as well as other vertically integrated lithium-ion battery firms targeting the same niche end markets with differing chemistries or scale advantages [S13][S25]. Price pressures intensify particularly as some competitors import lower-cost battery products or components.

Growth Prospects and Strategic Directions

Dragonfly is actively shifting away from direct consumer channels toward OEMs, fleet operators, distributors, and dealers—a move that aligns better with larger volume orders though often at thinner margins [N1][S23]. Key verticals targeted include:

- Recreational Vehicles: Leveraging relationships like THOR's $15 million strategic investment made in July 2022 alongside joint IP development agreements improves integration ease within factory-installed systems [S16].

- Heavy-Duty Trucking Fleets: Early commercial deployments with major operators highlight growing traction; products enable fuel savings via reduced diesel idling while helping fleets comply with anti-idling regulations [S20].

- Marine & Industrial Vehicles: Leveraging drop-in compatibility allows easier replacement of lead-acid systems maintaining reliable power delivery across harsh conditions.

Product-wise Dragonfly aims to transition from pack supplier toward becoming a full cell manufacturer through successful commercialization of its patented dry electrode process scalable across multiple chemistries including solid-state cells under development—a critical next phase expected to enhance thermal stability avoiding flammability issues posed by liquid electrolytes common among competitors' designs [S15][S1].

Expansion of complementary system components such as integrated heating solutions for cold-temp operation alongside monitoring software further broadens customer value proposition encouraging ecosystem lock-in within each application segment [S21]. Licensing deals contribute incremental revenues exemplified by contracts relating to the Battle Born brand licensing for B2B sales commenced in late 2024 [S23].

Watchpoints/Analysis:

Future growth will critically depend upon the pace of solid-state technology development success—currently subject to engineering challenges causing delays or risk of failure—and Dragonfly’s ability to leverage these innovations into broader OEM agreements beyond RVs into trucking fleets amid intense competitive dynamics [S1][S7]. Also pivotal will be broader market acceptance amid price sensitivity given increasing availability of lower-cost imports.

Financial Condition & Capital Allocation

Dragonfly’s losses have markedly expanded notwithstanding revenue growth signaling continued heavy investment weighted towards R&D scaling new technology platforms—net losses ballooned from $40.6m in 2024 to almost $70m in 2025 while operating cash flow remained negative at nearly $26m last fiscal year reflecting ongoing working capital absorption and fixed cost structure burdens related to automation upgrades [F1][S14].

Capital expenditures fell year-over-year indicating cautious liquidity management amid constrained access due partly to existing loan covenants restricting borrowings targeting minimum EBITDA levels plus liquidity thresholds imposed under the term loan amended multiple times during late-2025 refinancings that saw principal reduction from over $93m down near $19m combined with issuance of preferred shares carrying cumulative dividends not paid in cash but added back into principal obligations creating layered obligations on cash flow going forward [F1][S5][S14].[S22]

The company ended FY25 with approximately $18.3 million cash reserves against current liabilities of $19.7 million yielding a current ratio around 2.54 which suggests near-term liquidity coverage despite substantial losses but underscores limited runway absent further financing or marked improvement in cash generation metrics.[F1]

Equity remains positive but volatile having swung from negative ~$9m end-2024 back above $11m end-2025 largely due to equity raises tied partly to debt conversions coupled with warrant issuances raising dilution risk for existing shareholders going forward.[F1][S14]

No dividends or buybacks have been declared consistent with investment stage priorities focused on product development and capacity building rather than capital returns[S28].

Risks:

Persistent operating losses raise questions about sustainability without successful scale-up or additional capital injections which may prove dilutive or expensive amid current market volatility.[S24] Nasdaq listing compliance has previously been challenged due to market capitalization thresholds triggering corrective actions including reverse splits and shareholder approvals delaying delisting threats but highlighting volatility risk impacting investor confidence[S2].[N1] Potential legal exposure exists stemming from recent class action allegations claiming design defects causing safety risks related to overheating of certain positive terminal connections on specific Battle Born batteries; while management disputes liability there remains further uncertainty regarding financial consequences[S1].[N1] Supplier concentration risks linked to limited qualified LFP cell sources exposes operations vulnerable interruptions particularly if geopolitical disruptions materially affect global supply chains.[S6][S11] Dependence on a single Nevada manufacturing plant limits redundancy options further magnifying operational continuity risks[S6].[S10] Intense competition from traditional battery manufacturers combined with entrants focused on alternative chemistries pressures pricing power alongside rapid innovation demands requiring continued R&D investments limiting margin expansion[S13].[N1] Non-compliance risks relating anti-corruption statutes add potential reputational/legal costs especially if pursuing international procurement or commercial deals[S7],[S29]

Summary & Outlook

Dragonfly Energy Holdings sits at an inflection point balancing promising proprietary technologies offering differentiated environmental and safety advantages against capitalization challenges characteristic of early-stage specialty battery producers.Scaling innovative dry-electrode techniques towards full cell production along with advancing solid-state cells constitutes critical catalysts for long-term competitiveness.The company's focused shift toward OEM-fleet markets broadens volume streams beyond direct consumer sales but requires managing margin pressure amid fierce competitive ecosystems.Short-to-medium term outlook hinges heavily on improving revenue mix penetration along fleet accounts while containing escalating R&D spend alongside fulfilling stringent loan covenants.Safeguarding supply continuity amidst supplier concentration risk coupled with resolving ongoing litigation are essential near-term priorities.Financial flexibility remains constrained despite recent debt restructuring necessitating prudent capital stewardship.

Continued monitoring should focus on updates regarding solid-state technology milestones, execution progress within heavy-truck fleet deployments beyond pilot stages, outcomes related to class action litigation exposure, operating leverage improvements driven by factory automation efforts, liquidity trends relative to covenant thresholds post waiver expiration periods,and competitive positioning shifts responding dynamically both domestically within U.S.-based assembly advantages and globally relative pricing pressures.

This analysis is based solely on publicly available information through March 31, 2026; it does not constitute investment advice nor reflect any recommendation regarding securities listed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments