NeuroSense Therapeutics' Clinical Advances and Financial Strains Shape 2025 Results

Clinical progress with PrimeC contrasts sharply with liquidity pressures and widening losses in NeuroSense's 2025 financials.

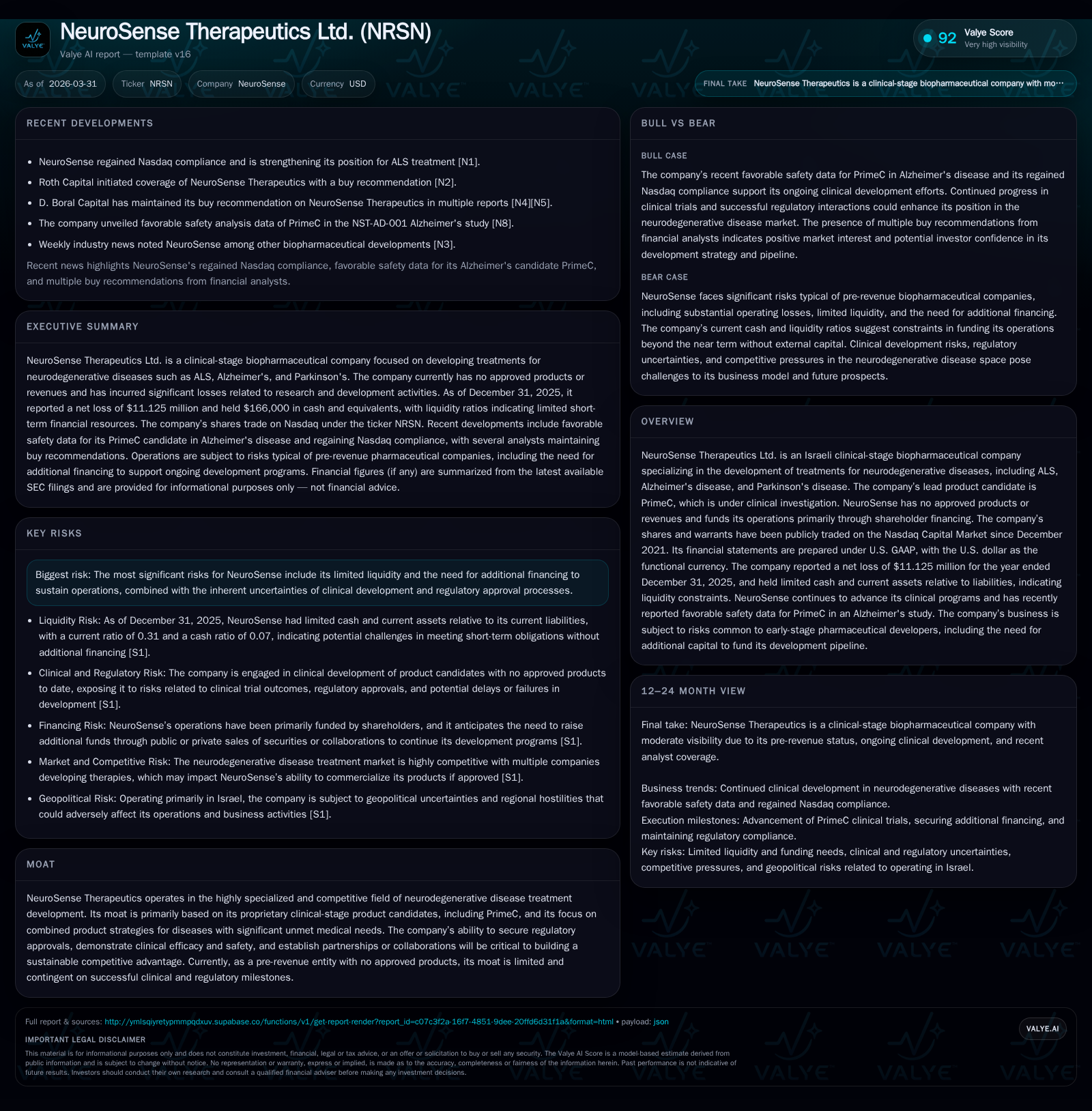

NeuroSense Therapeutics remains a clinical-stage biopharmaceutical entity focused on neurodegenerative disorders, with its lead candidate PrimeC advancing amid significant financial headwinds. Despite increasing R&D investment supporting clinical milestones, the company reported a deepening net loss of $11.125 million and suffers from a strained liquidity position evidenced by a current ratio of 0.31 as of year-end 2025. Funding operations currently relies heavily on shareholder financing, setting a clear need for additional capital to sustain drug development programs. Near-term value inflection hinges on PrimeC's regulatory progress balanced against ongoing capital challenges.

Historical Performance Patterns and Investment in R&D

NeuroSense Therapeutics operates as a clinical-stage biotech entity focused primarily on neurodegenerative diseases such as ALS through its lead candidate PrimeC. From fiscal years 2023 through 2025, the company has incurred steep operating losses driven mainly by elevated research and development expenses critical to advancing its clinical pipeline.

According to official financial metrics [F1][S1][S11][S14], operating income declined from -$9.902 million in 2024 to -$11.085 million in 2025, representing an approximately -11.9% year-over-year decrease. Net income followed suit, worsening to -$11.125 million by the end of 2025, marking roughly a 9% increase in net losses compared to the prior year. These trends highlight ongoing cash burn associated with costly clinical trials and preclinical programs.

Capital expenditures remain minimal (only $8,000 spent in 2025) relative to overall operating expenses—indicating that capital outlays are concentrated on intangible assets like drug development rather than physical infrastructure [F1][S11][S14]. This expenditure pattern aligns with typical early-stage biotech companies prioritizing pipeline progression.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -11 | -8 | -11 | 8000 | -9.0% |

| 2024 | -10 | -10 | -10 | 3000 | -1.0% |

| 2023 | -10 | -8 | -12 | 29000 | |

| 2022 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | -8 | ||

| 2024 | 96000 | -10 | |

| 2023 | 310000 | 96000 | -8 |

| 2022 | 310000 |

Source: SEC companyfacts cache [F1].

Financial Overview: Losses, Liquidity Challenges, and Capital Structure

Despite scientific advancements, NeuroSense's financial condition shows considerable strain at the close of FY2025. The company held only $166 thousand in cash and equivalents against current liabilities exceeding $2.516 million at year-end—resulting in a challenging current ratio of approximately 0.31 [F1][S4][S5][S6][S8][S10][S12]. While pre-revenue biopharma firms typically operate under elevated risk profiles due to developmental activities, this ratio underscores acute short-term funding pressures.

Shareholders’ equity swung back into negative territory at -$1.56 million in FY2025 after positive equity was reported in FY2024 [F1][S10]. This reversal reflects accumulated retained deficits from sustained net losses overwhelming previous equity injections despite recent capital raises [S8][S12]. The absence of operating revenues exacerbates reliance on external financing for working capital.

Trade payables and accrued liabilities increased substantially alongside accrued expenses nearing $1.7 million—highlighting growing operational obligations [S6][S8]. Lease liabilities are classified as operating leases under ASC 842 but do not represent material debt burdens [S4]. Overall debt levels remain minimal; thus financial leverage risk is low but liquidity risk remains significant due to limited cash reserves.

Clinical Pipeline Update: Progress on PrimeC and Regulatory Milestones

NeuroSense’s therapeutic efforts are concentrated on PrimeC for ALS treatment complemented by early-stage research in Alzheimer’s and Parkinson’s diseases using combined product strategies [N1][N2][S3]. Recent announcements include regaining Nasdaq compliance which enhances investor confidence and corporate governance standing [N1].

Roth Capital’s initiation of buy coverage reflects institutional interest grounded in optimism about trial progression while recognizing inherent biotech risks for companies without approved products [N2]. Regulatory milestones ahead constitute key inflection points for valuation.

Forward Outlook: Potential Catalysts and Operational Risks

Explicit future guidance is limited; however disclosures suggest that regulatory decisions related to PrimeC’s clinical phases will be pivotal catalysts potentially validating commercialization prospects or partnerships [N1][S1][S2].

Conversely, NeuroSense’s precarious liquidity position may necessitate dilutive financings or strategic collaborations under terms possibly unfavorable to shareholders if not carefully managed [S1]. Its emerging growth company status provides reporting relief but signals continued dependence on early-stage investment dynamics.

Capital Allocation: Focused R&D Investment Amid Financial Constraints

The company allocates capital almost exclusively toward sustaining R&D activities necessary for advancing its clinical pipeline without generating any product revenue or positive cash flow from operations [F1][S7][S9][S17][S19]. Dividends ceased following modest distributions through FY2023 ($310k annually), reflecting prudent conservation of capital aligned with developmental priorities [F1]. Share repurchases have effectively halted post-2023.

Return on equity calculations are distorted due to negative book equity (-$1.56 million in FY2025), limiting their usefulness for performance assessment [F1]. Free cash flow remains deeply negative (approximately -$7.679 million based on CFO minus capex), consistent with early-stage biotech norms prioritizing pipeline maturation over profitability.

Strategic Considerations: Balancing Innovation Opportunity With Financing Risk

From an investment perspective emphasizing scientific innovation tempered by fiscal sustainability concerns, NeuroSense presents both opportunity linked to unmet neurodegenerative needs and existential risk contingent upon successful trial outcomes alongside continued access to capital markets [F1][N2][S1].

Heavy reliance on a single lead candidate underscores pipeline concentration risk amid competitive neurodegenerative therapy landscapes.

Investors should monitor near-term cash burn relative to clinical data readouts and financing activity closely to assess viability beyond immediate horizons while watching for partnerships or licensing deals that could provide alternative funding avenues.

This narrative is prepared for informational purposes and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments