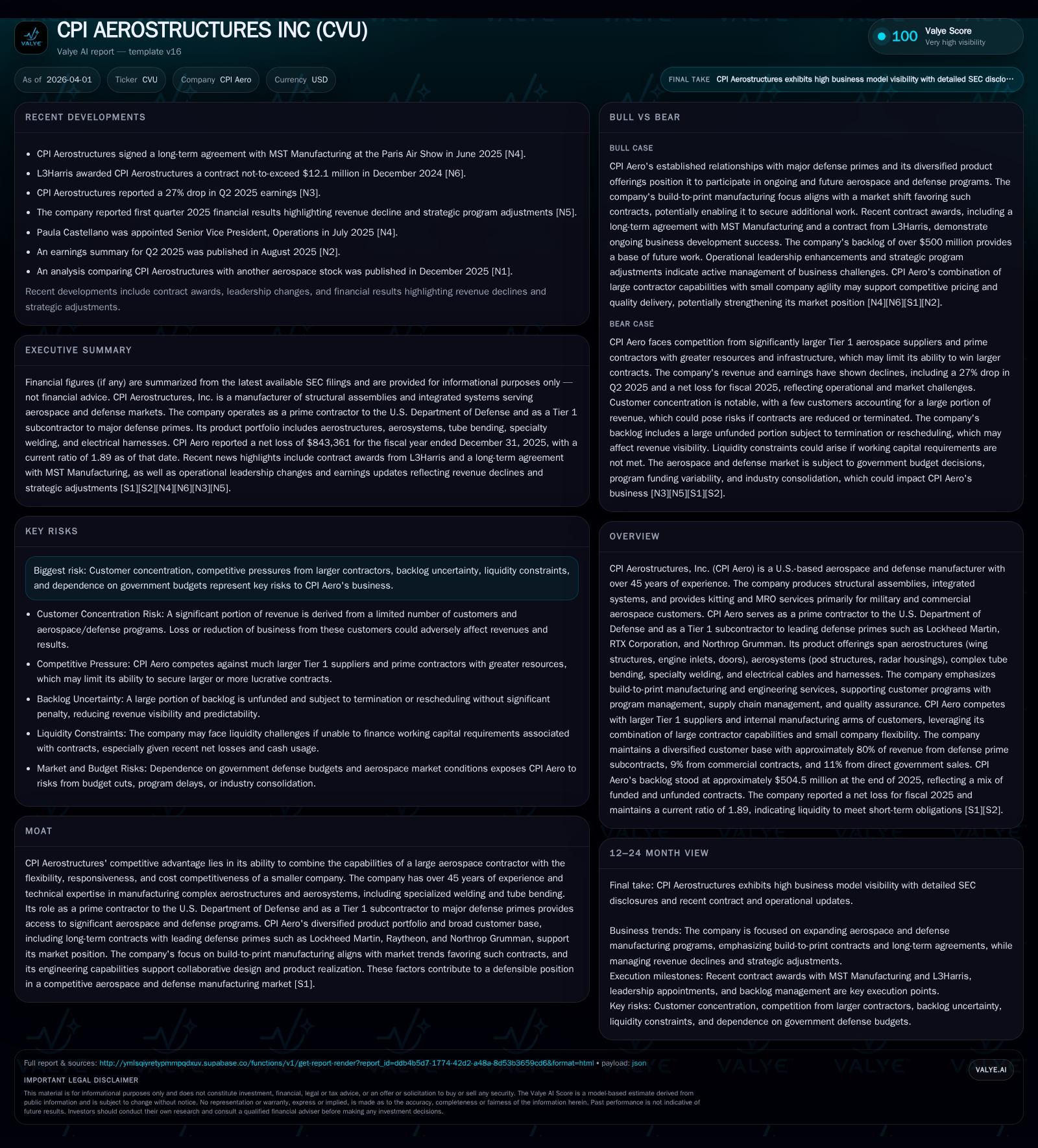

CPI Aerostructures Navigates Margin Pressure Amid Government Contract Uncertainties

Despite stable revenues, CPI Aerostructures faces operational losses and liquidity constraints driven by contract dynamics and working capital demands.

CPI Aerostructures, a Tier 1 aerospace and defense subcontractor, reported a sharp decline from operating income to a loss in 2025 amid stable revenue levels. The company’s backlog remains robust but is subject to government funding variability and contract termination rights. Liquidity is pressured by high borrowing costs, restrictive debt covenants, and negative cash flow. Customer concentration with major primes like Raytheon and Sikorsky presents both opportunity and risk. Capital returns are constrained by losses and covenant restrictions, while competitive pressures persist from larger aerospace firms. Management continues to pursue long-term contracts to stabilize future revenue streams.

Historical Growth and Operating Performance Trends

CPI Aerostructures’ revenue peaked at approximately $31.6 million in FY2015 before contracting to about $23.8 million in FY2017, where it has since stabilized without significant growth reported [F1]. This trend reflects challenges in maintaining volume or pricing within its aerospace and defense manufacturing niche.

Profitability has deteriorated notably: after posting operating income above $6.7 million in FY2024, the company recorded an operating loss of roughly $176 thousand in FY2025 alongside a net loss of approximately $843 thousand [F1]. This shift signals rising contract costs or operational inefficiencies outpacing revenues.

Cash flow from operations also reversed sharply, moving from a positive $3.6 million in FY2024 to negative $5.2 million in FY2025, highlighting increased working capital demands possibly tied to upfront costs under complex government contracts [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1 | -5 | 0 | 65036 | -125.6% |

| 2024 | 3 | 4 | 7 | 403854 | -80.8% |

| 2023 | 17 | 4 | 6 | 140450 | +87.5% |

| 2022 | 9 | 1 | 5 | 40789 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -3.3 |

| 2024 | 3 | 12.7 |

| 2023 | 4 | 77.9 |

| 2022 | 1 | 218.6 |

Source: SEC companyfacts cache [F1].

Source: Annual data per latest SEC filings [F1]

Backlog Composition and Revenue Drivers

CPI Aero’s revenue is heavily dependent on U.S. Government contracts either direct or as a Tier 1 subcontractor for major primes including Raytheon Technologies, Sikorsky (Lockheed Martin), Lockheed Martin itself, and the U.S. Air Force [S1][S13][S25]. These customers accounted for approximately 38%, 20%, 11%, and 11% respectively of FY2025 revenues [S1].

The company’s funded backlog grew moderately from about $85 million at end-2024 to roughly $91.8 million at end-2025 while unfunded backlog slightly decreased amid cautious customer commitments [S13]. However, backlog figures are not definitive indicators of future revenue due to contract modifications, termination rights without significant penalty for unfunded portions, and dependency on government funding cycles which can cause delays or cancellations [S1][S13].

Revenue recognition aligns with costs incurred under ASC606 but remains vulnerable to supply chain issues or changes in production schedules.

Liquidity Profile and Debt Covenants

Liquidity depends on a revolving credit facility secured by substantially all assets provided by Western Alliance Bank (formerly BankUnited). As of September 30, 2025, borrowings under this facility stood near $15.9 million with interest charged at Prime +2%, resulting in an effective rate around 9.5% during that period [S4][S5][S6].

The credit agreement includes financial covenants such as minimum debt service coverage ratio (≥1.5x), maximum leverage ratio (≤4x), minimum quarterly net income after taxes (≥$1), and minimum adjusted EBITDA (≥$1 million), tested quarterly [S6]. CPI Aero required multiple waivers during fiscal year 2025 due primarily to earnings declines linked with program terminations impacting covenant compliance [S4][S6].

These covenants also restrict dividends, asset sales without consent, additional indebtedness, mergers/acquisitions transactions, and certain payments on subordinated debt limiting flexibility [S4][S10]. Negative operating cash flow exacerbates liquidity pressure raising risks related to potential covenant breaches or collateral foreclosure.

Market Positioning and Customer Concentration Risks

CPI Aero’s competitive advantage stems from combining the scale capabilities of larger Tier 1 subcontractors with the agility of a smaller organization focused on build-to-print aerostructures including wing assemblies, engine air inlets, tactical pods for electronic warfare/intelligence surveillance reconnaissance systems alongside specialized welding services [S18].

It competes against larger Tier-1 suppliers such as Spirit Aerosystems and Kaman Aerospace for structural components while facing fewer competitors for aerosystems products where internal manufacturing arms dominate competition [S18].

Customer concentration remains elevated with four major customers representing nearly 80% of revenues; this concentration exposes CPI Aero to risks from changes in production volume or contract awards among these key primes [S1][S28].

Outlook and Growth Considerations

Management focuses on securing long-term agreements offering greater stability alongside expanding into commercial aerospace segments such as engine inlet production for Embraer’s Phenom series aircraft initiated recently with initial orders expected to generate deliveries starting in 2026 [S13].

Nonetheless, growth visibility is moderated by ongoing government budget uncertainties affecting contract funding cycles along with risks inherent in subcontracting such as scope changes or cancellations that may affect timing or realization of revenues [S13][S19][S20][S25][S27].

Competition remains intense with larger aerospace primes possessing greater resources challenging CPI Aero’s cost competitiveness despite its responsiveness advantage.

Capital Allocation Profile

Capital allocation is constrained by operational losses reflected in negative net income (-$843K) relative to equity (~$25.8 million) yielding an approximate return on equity of -3.3% for FY2025 [F1]. Free cash flow was deeply negative at over $5 million reflecting substantial working capital consumption amid lower profitability [F1].

No dividend payments or share repurchase activities have been disclosed consistent with lender-imposed restrictions limiting distributions under existing credit agreements which prioritize liquidity preservation amidst covenant compliance challenges [F1][S4][S10].

This analysis synthesizes publicly available financial statements and SEC disclosures without providing investment advice or forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments