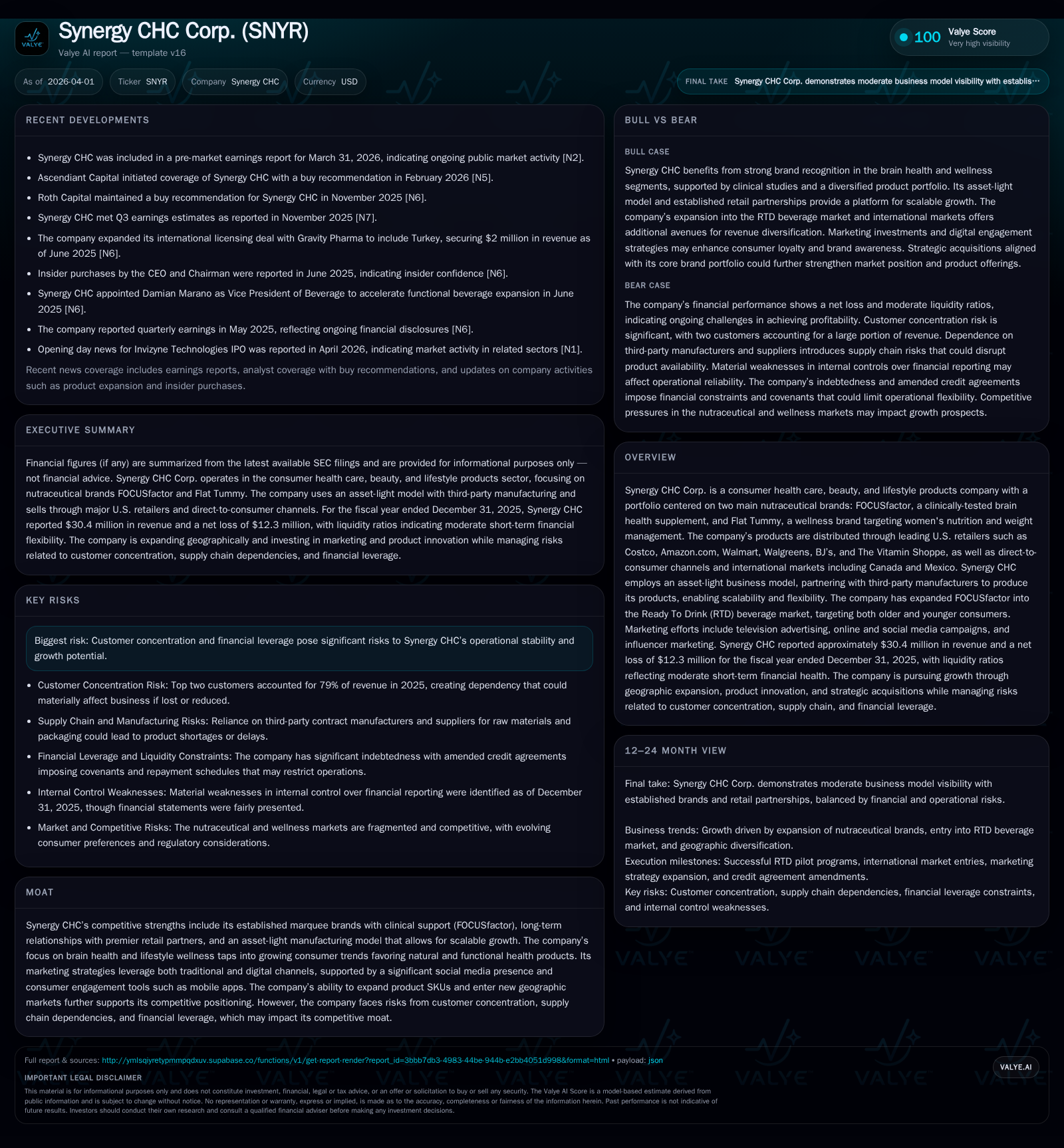

Synergy CHC Corp.: From Clinical Brands to Capital Pressures

Synergy CHC's expansion of its clinically backed nutraceutical brands contrasts sharply with rising financial leverage and operational losses.

Synergy CHC Corp. has developed two marquee nutraceutical brands—FOCUSfactor, a clinically validated brain health supplement, and Flat Tummy, focused on women's nutrition—that have driven SKU proliferation and geographic expansion. Despite these product portfolio advances and an asset-light manufacturing model enabling scalability, the company faces declining revenues and mounting losses, including a 12.8% revenue drop alongside an operating loss of $8.5 million in 2025 [F1]. Intensifying regulatory scrutiny and legal risks inherent to the fragmented U.S. supplement market burden operations. Moreover, Synergy’s significant financial leverage and negative equity strain its capital flexibility, raising questions about near-term growth funding and debt servicing [S9][S21].

Historical Performance: Growth Erosion Despite Core Brand Expansion

Synergy CHC Corp.’s financial trajectory over recent years underscores a troubling erosion of growth despite strategic brand developments. After acquiring its key brands—FOCUSfactor in January 2015 and Flat Tummy later that year—the company successfully expanded SKU counts markedly: FOCUSfactor grew from 3 SKUs to over 34 by end-2025, while Flat Tummy increased from a single SKU to 13 under its wellness umbrella [S1][S27].

However, these product line expansions have coincided with declining financial performance. Revenues dropped from $34.8 million in FY2024 to $30.4 million in FY2025, marking a -12.8% year-over-year decline according to the latest filings [F1]. Operating income swung from a positive $5.8 million surplus into an $8.5 million loss (a -245.8% change), signaling deteriorating margins amidst higher costs or weaker pricing power possibly linked to competitive pressures and customer concentration risks [F1]. Net income likewise plunged into a loss exceeding $12 million in FY2025.

Operational cash flow remains a point of concern with negative figures persisting at approximately -$2.6 million for FY2025, though slightly improved compared to -$4.8 million the prior year, indicating ongoing challenges converting sales into liquidity amid cost structure burdens [F1]. Capital expenditures have remained minimal (~$129K historically), reinforcing Synergy’s asset-light approach but limiting investment in infrastructure that could drive efficiencies or innovation.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 30 | -12 | -3 | -8 | -12.8% | -680.8% |

| 2024 | 35 | 2 | -5 | 6 | ||

| 2019 | -9 | 3 | -8 | -49.5% | ||

| 2018 | 34 | -6 | 1 | -5 | -5.0% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 53.4 | |

| 2024 | -12.8 | |

| 2019 | 3 | 177.0 |

| 2018 | 1 | -155.2 |

Source: SEC companyfacts cache [F1].

Table: Selected Annual Financial Metrics illustrating declining revenue and profitability alongside persistent negative cash flows [F1]

This pattern highlights an operational tension: rapid SKU proliferation aimed at capturing niche wellness segments contrasts with diminishing underlying business fundamentals.

FOCUSfactor & Flat Tummy: Brand Dynamics Powering Product Diversification

At Synergy’s core lie two marquee nutraceutical brands well positioned within consumer health trends emphasizing natural cognitive support and women's wellness.

FOCUSfactor offers a clinically tested brain health supplement featuring a unique proprietary formula supported by independent trials—not FDA drug approval—but designed specifically to enhance memory, concentration, and focus [S1]. The brand’s evolution includes expansion beyond traditional supplement tablets into Ready To Drink (RTD) beverages targeting both older adults concerned with cognitive decline and younger consumers seeking functional energy products—a strategic articulation of innovation within the RTD segment known for rapid growth but intense SKU competition [S27].

Flat Tummy operates within the lifestyle nutrition space focusing primarily on women's weight management with various SKUs extending into nutritional shakes and other wellness supplements [S27]. This diversification reflects broadening consumer demand but also exposes the brand to evolving product cycle risks common in weight management categories.

The company’s asset-light manufacturing model is significant here: by outsourcing production entirely to third-party contract manufacturers with multiple regional suppliers, Synergy can flexibly scale volumes without heavy fixed asset burdens or supply bottlenecks typical of vertically integrated competitors [S27]. This enables accelerated SKU proliferation—expanding FOCUSfactor SKUs from just three at acquisition in early 2015 to over thirty-four today—while leveraging multimillion-dollar retail distribution agreements with Costco, Amazon.com, Walmart, Walgreens, BJ’s Wholesale Club, and The Vitamin Shoppe among others [S27]. International distribution extends into Canada and Mexico providing additional avenues for growth.

Nevertheless, this expansion strategy demands close management of partner relationships and constant product innovation cycles characteristic of rapid SKU proliferation strategies within nutraceuticals.

Navigating Competitive and Regulatory Risks in Nutraceutical Markets

The U.S nutritional supplement market is notably fragmented yet fiercely competitive with low barriers to entry fueling continuous new product introductions that can rapidly erode shelf space and consumer mindshare [S4]. Synergy contends against better-capitalized rivals capable of expediting product launches and marketing spend often backed by larger research teams supporting clinical substantiation.

Regulatory oversight imposes acute risks that have intensified over recent years across several vectors:

- The Federal Trade Commission (FTC) rigorously enforces advertising truthfulness standards requiring substantiation backed by competent scientific evidence prior to claim dissemination; failure invites costly enforcement actions including fines or consent decrees [S5][S16].

- Litigation risks arise under the Lanham Act where competitors challenge promotional claims deemed false or misleading potentially triggering treble damages or forced corrective advertising campaigns harming brand reputation [S6][S25].

- Consumer class action lawsuits alleging deceptive marketing practices have become more frequent across supplement companies affecting public perception even when claims lack merit [S6].[*]

- FDA regulations increasingly demand more detailed recordkeeping for adverse events reporting plus potential reformulation mandates should scientific consensus or law evolve unfavorably against certain ingredients or product categories; such regulatory shifts could force costly recalls or withdrawal of specific SKUs undermining sales continuity [S4][S23].

- State-level initiatives add complexity; for example New York’s Weight Loss Products Bill imposes age verification requirements adding compliance costs especially for Flat Tummy line products targeted at women seeking weight management assistance [S24].[*]

These factors collectively heighten operating risk through increased compliance costs, litigation contingencies, reputational damage potential, and added hurdles for new product development cycles.

Capital Structure and Leverage: Impact on Investment Capacity and Returns

Financial leverage remains a critical constraint shaping Synergy CHC’s strategic latitude.

As of December 31, 2025, shareholders’ equity was deeply negative at approximately -$23.1 million reflecting accumulated net losses eroding retained earnings alongside impairment charges noted historically—a stark contrast from positive $3.97 million equity five years earlier illustrating severity of financial deterioration over time [F1].

Liquidity ratios present modest cushioning: current assets totaling about $10 million versus current liabilities near $8.2 million yield an approximate current ratio of 1.22 indicating some short-term solvency but limited buffer against sudden shocks given concentrated customer base dependence (top-two customers >79% revenue) elevating counterparty risk further constraining liquidity reliability [F1][S13].

The term loan credit agreement amended March 2026 introduces stricter financial covenants tied to minimum consolidated adjusted EBITDA thresholds ($0.5M for Q2 2026 rising to $1M for Q3), leverage ratio step-downs starting at a maximum senior net leverage ratio of 20x at end-2025 resting on future reduction plans plus conditions compelling substantial equity raises totaling at least $10 million by September 30, 2026 or face interest margin penalties increasing borrowing costs materially (+200 bps if unmet) as well as mandatory partial prepayments triggered by excess equity proceeds above defined amounts—all underscoring lender impatience regarding deleveraging progress while tightening covenant discipline [S9][S21].

Despite these pressures Synergy reports ROE approximating positive 53%, primarily distorted by negative equity denominator rather than underlying profitability which remains challenged due to operating losses; thus caution regarding quality of returns measured solely by this metric is warranted [F1].[*]

Assessing Near-Term Milestones and Growth Catalysts

While explicit forward guidance remains limited publicly, several key events will be critical inflection points:

- Successful execution of RTD category rollout efforts for FOCUSfactor targeting broader demographics beyond traditional brain health supplement purchasers could unlock new sales streams leveraging existing retail networks [N1].

- Further penetration into leading retailer distributions with SKU rationalization balancing innovation breadth against category shelf economics may determine incremental margins going forward.

- International expansion growth in Canada/Mexico markets presents moderate revenue diversification potential albeit exposed to foreign exchange volatility and compliance complexity described earlier [S14].[*]

- Management’s ability to remediate identified internal control material weaknesses around financial reporting systems may influence investor confidence and compliance cost trajectories reducing risk of restatements or sanctions but remains ongoing as stated in filings [S4].[*]

- Achievement of mandated equity issuance thresholds under amended credit terms by late Q3 calendar year will be pivotal in avoiding costlier debt service conditions plus securing covenant compliance sustainment necessary for refinancing flexibility or additional capital raising opportunities [S9][N1].[*]

Investors will monitor these milestones closely as proxies for operational turnaround progress amid challenging macro backdrop.

Cash Flow Dynamics and Capital Allocation: Dividends, Buybacks, and Debt Management

Synergy’s cash flow profile presents pronounced constraints limiting discretionary capital deployment opportunities.

Operating cash flow was negative approximately $2.58 million in FY2025 representing an improvement over prior year’s wider deficit (-$4.80M), signaling reduced cash burn though still requiring financing support given ongoing expenses outpacing inflows after gross profit adjustments likely pressured by inventory write-downs or higher SG&A expense allocations tied to marketing investments as per company report narratives [F1][S26].[*]

Capital expenditure levels remain very low reflecting the firm’s asset-light model reliant on third-party contract manufacturers obviating need for heavy fixed asset spending; however this also caps long-term capacity expansion potential absent strategic investments or acquisitions which themselves represent integration risks per filings [F1][S22].[*]

Share repurchases have been negligible since mid-decade cessation highlighting absence of shareholder return policies amid liquidity preservation priorities; similarly no dividends are planned foreseeing earnings retention primarily directed towards debt reduction efforts per documented capital allocation statements in annual report section on dividends/buybacks suggesting zero foreseeable cash dividend yield for investors on common stock holdings barring substantial operational turnaround improving free cash generation prospects [F1][S26].[*]

Debt servicing dominates internal capital allocation focus underscored by amended loan terms enforcing scheduled principal payments beginning mid-2026 combined with mandatory prepayment mechanisms linked directly to equity raise success reflecting constrained balance sheet flexibility confronting the company presently [S9][S21].[*]

What to Watch: Indicators of Turnaround or Further Headwinds

Key indicators signaling positive inflection include timely achievement of minimum EBITDA targets establishing momentum toward profitability improvement as well as successful completion of planned equity capital raises mitigating interest rate step-ups enhancing liquidity stability.

Progress expanding RTD penetration beyond core supplement forms within existing retail accounts coupled with gaining adjacent wellness category traction may signal resilient demand supporting broader product portfolio scalability.

Conversely signs warranting caution involve regulatory enforcement intensification especially involving FTC complaints or state attorney general investigations impacting brand image; failure to remediate weak internal controls exacerbating audit risk might undermine market trust coupled with inability meeting debt covenants posing refinancing difficulties impairing survival prospects.

Additionally consumer trend shifts away from legacy brain health supplements toward competitive digital cognitive enhancement supplements could compress margins absent continued innovation investment hard when constrained financially.[*]

Sector specialists will recognize terms such as "omnichannel penetration" highlighting multi-channel retail strategies vital amid changing consumer buying patterns; "SKU rationalization" essential balancing assortment breadth versus shelf economics; combined with "FDA/FTC compliance risk" encapsulating regulatory vigilance—factors shaping not just Synergy's fate but broadly reflective across mid-tier nutraceutical peers striving for sustainable growth amidst tightening external scrutiny.[*]

This analysis aims solely at evaluating Synergy CHC Corp.’s operational positioning juxtaposed against its financial constraints using available SEC filings and reported data as validation points without offering investment advice nor price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments