LightInTheBox's Transition to Brand-Centric Apparel Unlocks Profitability After Revenue Compression

The company’s strategic pivot from broad e-commerce retail to proprietary apparel brands drove a profit rebound despite steep revenue declines.

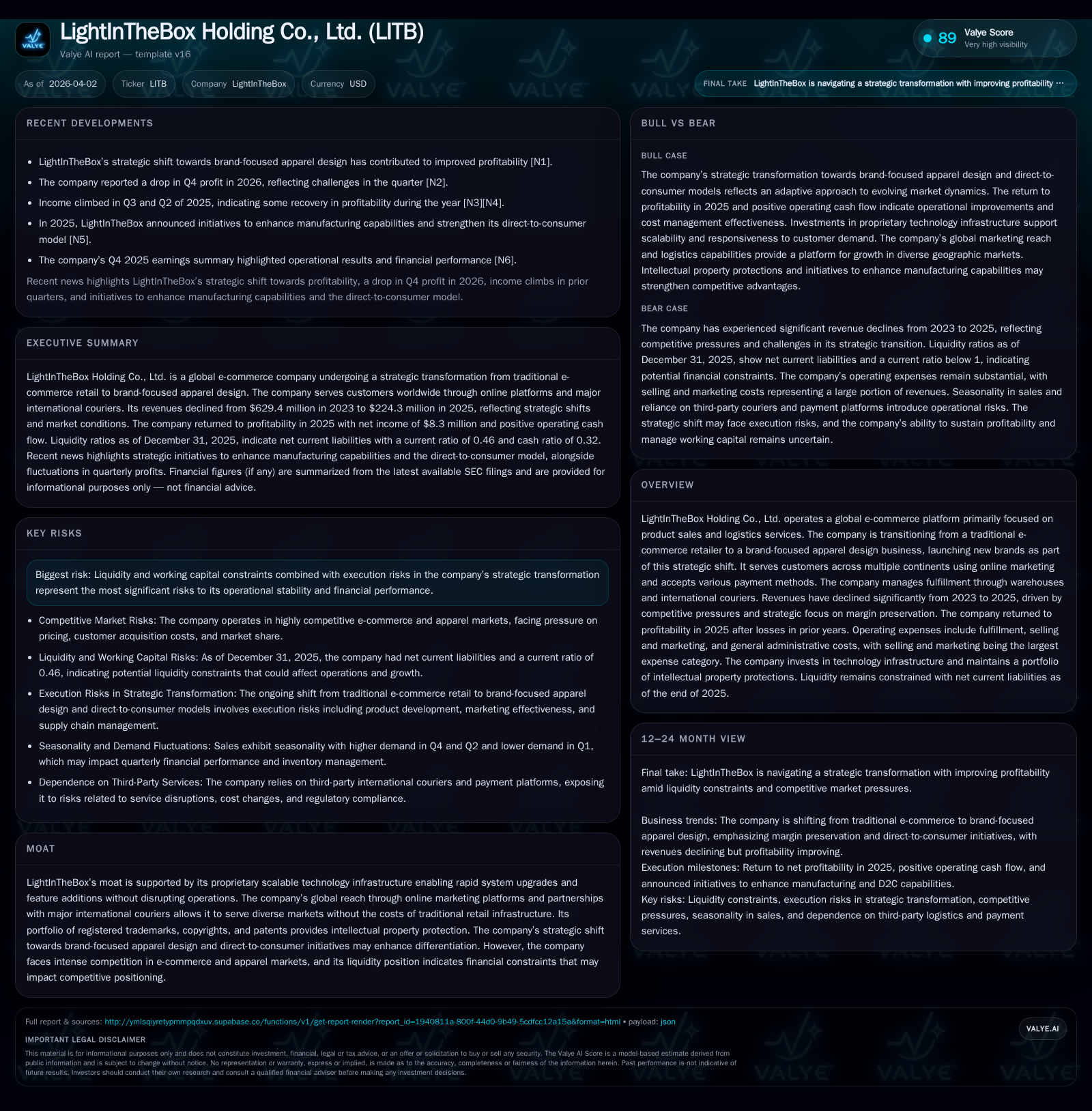

LightInTheBox faced a sharp revenue contraction from $629 million in 2023 to $224 million in 2025 amid intense competition and a deliberate shift towards margin preservation. The transition towards brand-focused apparel design has enabled the company to reverse net losses and return to profitability, supported by operational cost controls and enhanced gross margins reflecting higher-value product lines. Liquidity constraints remain a critical risk as the firm balances capital allocation between technology investment and shareholder returns. Going forward, execution of the transformation and sustainable revenue stabilization will be key milestones to monitor.

From Scale to Specialty: Historical Performance and Revenue Dynamics

LightInTheBox's financial trajectory over the recent three-year period reflects a significant contraction followed by strategic recalibration. Revenues declined from $629.4 million in 2023 to $224.3 million in 2025, marking a reduction of over 64%, driven by intensified market competition and a deliberate strategic pivot towards margin preservation through an evolving product mix focused increasingly on proprietary apparel brands [S1][F1].

Operating income improved from a loss of approximately $10.4 million in 2023 and $2.2 million in 2024 to a positive $7.96 million in 2025, indicating successful cost realignment despite reduced scale [F1]. Net income followed this trend, reversing losses of $9.6 million and $2.5 million into an $8.28 million profit by year-end 2025 [F1]. Operating cash flow strengthened substantially, shifting from outflows of $20.7 million in 2023 and $48.2 million in 2024 to a positive inflow of $6.21 million in 2025, evidencing improved working capital management during restructuring [F1].

Capital expenditures contracted sharply alongside revenues—from about $1.15 million in 2023 down to just $42 thousand in 2025—reflecting disciplined spending aligned with prioritization of modular technology infrastructure investments rather than large-scale physical asset outlays [F1][S8].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 8 | 6 | 8 | 42000 | +432.6% |

| 2024 | -2 | -48 | -2 | 782000 | +74.0% |

| 2023 | -10 | -21 | -10 | 1149000 | +83.1% |

| 2022 | -57 | 36 | -14 | 817000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 1 | 6 |

| 2024 | 1 | -49 |

| 2023 | 2 | -22 |

| 2022 | 3 | 35 |

Source: SEC companyfacts cache [F1].

Note: Financial figures rounded; YoY percentages based on reported values [F1].

Strategic Shift: E-Commerce Retail to Brand-Focused Apparel Design

LightInTheBox is transitioning from traditional e-commerce retail towards launching proprietary apparel brands aimed at differentiating its product offerings and improving pricing power and customer loyalty potential [N1][S1]. Faced with commoditized products and intense competition, this shift seeks sustainable growth via direct-to-consumer appeal anchored on unique designs.

This new focus targets enhanced repeat purchase rates—a critical metric for profitability in branded apparel sectors where customer lifetime value outweighs single sales volume [S4][S14]. The transition is complex given established competitors but leverages proprietary design capabilities combined with print-on-demand bespoke products that create distinctive value propositions difficult for resellers to replicate swiftly.

Operational Efficiencies Amid Market Pressures

Cost control remains pivotal: selling and marketing expenses—the largest expenditure—declined substantially from approximately $302.7 million (48% of revenues) in 2023 to $102.5 million (45.7%) in 2025, reflecting optimized digital marketing spend through targeted platforms like Google and Facebook while managing customer acquisition costs carefully [S7][S18]. Fulfillment expenses similarly decreased both absolutely and proportionally, maintaining around ~7% of revenues despite shrinking scale, indicating logistic efficiency gains [S18][S24].

General administrative expenses also contracted significantly, balancing cash flow pressures while preserving organizational capacity for transformation execution.

These efforts converted earlier gross profit pressures into positive operating income by fiscal year-end 2025, underscoring disciplined unit economics essential for long-term sustainability [S7][N1].

Technology Infrastructure as Competitive Advantage

The company's proprietary modular technology infrastructure enables rapid system upgrades and feature rollouts critical for agile brand development without operational disruption or heavy fixed costs [S9]. This platform supports graphics-rich design tools, personalized shopping experiences, diverse payment integrations including PayPal, Klarna, Apple Pay, Shop Pay, Visa, MasterCard, plus real-time inventory management aligned with print-on-demand manufacturing.

Investment emphasis favors software scalability over heavy capital expenditures, reducing risk while enhancing flexibility needed for direct-to-consumer engagement where responsiveness drives satisfaction and retention [S16][S21].

Global Reach Without Traditional Retail Overhead

Operating across Europe, North & South America, Oceania, and Asia, LightInTheBox leverages online platforms alongside partnerships with major international couriers such as DHL, UPS, FedEx, EMS to deliver globally without the costs of conventional multinational retail infrastructure [S1][S3].

Customer acquisition benefits from sophisticated online marketing leveraging demographic segmentation crucial for penetrating diverse markets amid competitive user acquisition cost inflation.

Challenges include currency fluctuations and import regulations impacting cross-border logistics; these are managed through agile supply chain configurations supported by technology-enabled track-and-trace systems built on the scalable backend architecture [N1][S13].

Liquidity Profile and Capital Allocation

Liquidity remains constrained as reflected by a current ratio near 0.46 at year-end 2025—a challenge heightened by investment needs against cash flow timing inherent in the evolving apparel DTC model [F1][S5]. Incremental borrowings have historically supplemented liquidity but require prudent leverage management aligned with long-term strategy.

Positive operating cash flow generation ($6.21 million) coupled with minimal capex ($42 thousand) marks a shift from prior years' heavier investments consistent with downsizing legacy operations while focusing resources on high-return technology areas [F1][S8].

Share repurchases proceeded cautiously with approximately $724 thousand deployed during fiscal year 2025—signaling measured capital returns balanced against financial discipline needs amid transformation efforts [F1][S10][S11]. Dividend payments remain minimal or absent given reinvestment priorities.

Outlook and Execution Risks

While explicit guidance is limited publicly, key metrics such as sustained revenue stabilization post-transition; success indicators for proprietary brands; normalized customer acquisition costs relative to lifetime value; plus maintenance of positive operating cash flows amid scaled marketing campaigns will be critical to track progress toward growth acceleration supported by ongoing technology enhancements [N1][S25].

Risks include liquidity sufficiency under tightened working capital management; competitive pressures especially from fast-fashion incumbents; plus execution challenges inherent in reshaping business models amid volatile consumer demand affected by global macroeconomic factors influencing disposable incomes.

Continued technological innovation paired with agile supply chain management will be essential levers alongside vigilant cost control measures if LightInTheBox is to cement its repositioned identity as a specialized brand-focused e-commerce apparel operator rather than a commoditized retailer.

This analysis integrates financial data through fiscal year-end 2025 alongside disclosures up to April 2026 without offering prescriptive investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments