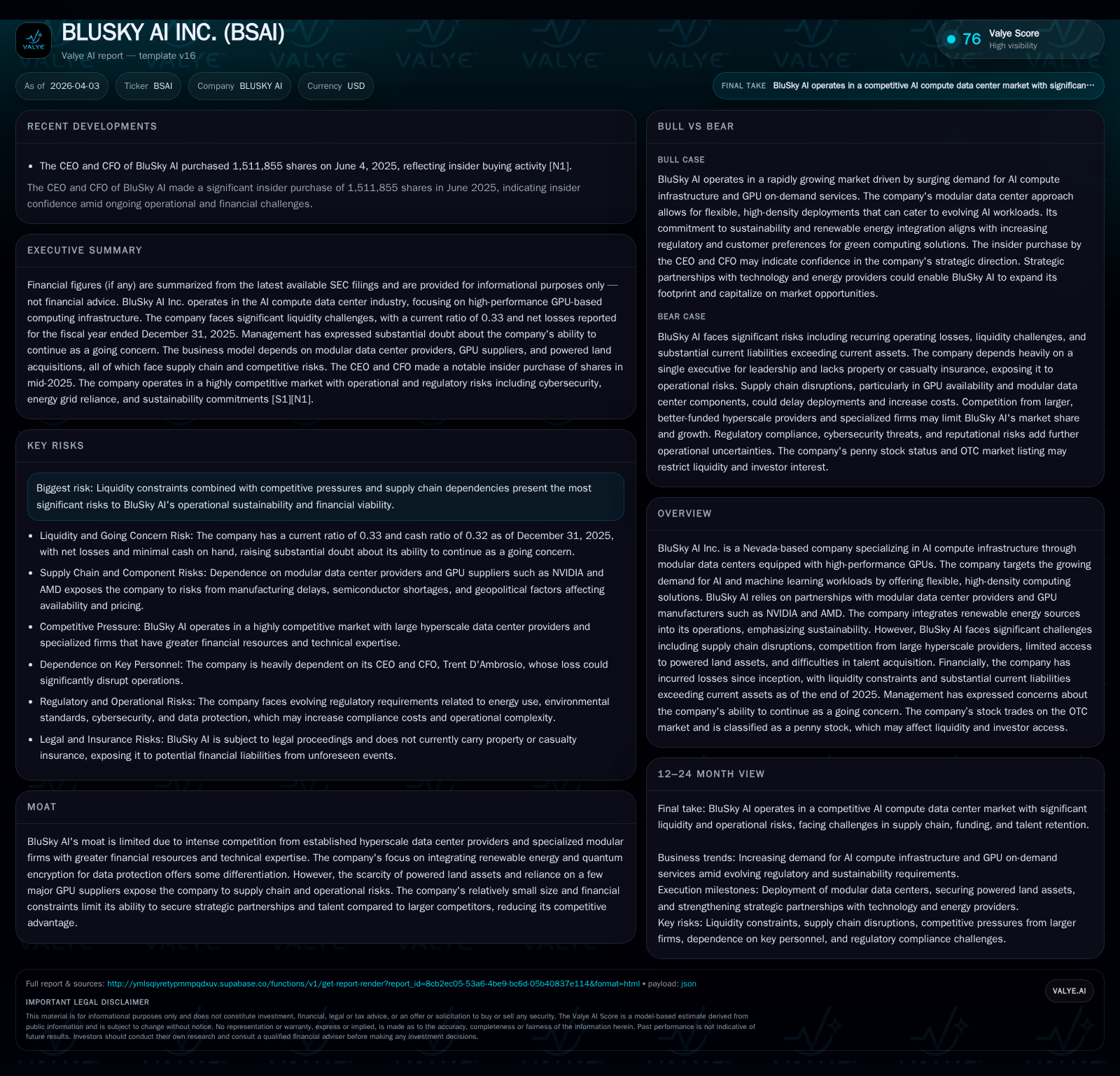

BluSky AI’s Capital Intensity and Supply Chain Constraints Undermine Growth Prospects

A financially constrained modular data center provider faces operational bottlenecks amid competitive pressures and strategic asset scarcity.

BluSky AI Inc. operates in the burgeoning AI compute infrastructure space, specializing in modular data centers with high-performance GPUs. Since its inception, the company has consistently reported operating losses and currently faces liquidity challenges, with liabilities significantly exceeding assets as of year-end 2025 [F1][S1][S5][S16]. Its growth hinges on securing powered land assets and maintaining critical GPU supply partnerships—both under pressure from established hyperscalers and supply chain disruptions [S6][S17]. Additionally, BluSky AI’s strategic emphasis on renewable energy integration adds complexity amid fluctuating costs and regulatory requirements [S8]. With no committed capital for expansion and a small, talent-constrained team led by CEO Trent D’Ambrosio, the company’s ability to scale and innovate remains uncertain [S20][S21]. Investors should monitor developments in capital raises, supply chain stability, operational execution, and regulatory compliance as key sentiment drivers going forward.

Company Overview

BluSky AI Inc., a Nevada-based company formerly known as Inception Mining Inc., has pivoted towards a niche yet fast-growing segment within the data center industry: modular AI compute infrastructure. Operational since 2007 but consistently loss-making, BluSky AI targets GPU-intensive artificial intelligence workloads through modular data centers equipped with high-performance computing units from major chipmakers like NVIDIA and AMD. Their service model emphasizes flexibility, scalability, and sustainability via integration of renewable energy sources such as solar, wind, or geothermal.

Historical Performance

Financially, BluSky AI reflects the archetype of a startup cultivating a capital-intensive technology platform under severe competitive stress. According to the latest certified financials ending December 31, 2025 [F1], revenue remains at zero—a sign either of pre-revenue status or recognition timing delays typical in early-stage deployments. Operating income deteriorated from a loss of approximately $521k in 2024 to nearly $2.67 million loss in 2025, signaling escalated spending possibly linked to capacity builds or R&D investments.

Net losses have broadened substantially from less than $1 million (negative $949k) in the prior year to more than $4.5 million at end-2025. Cash flows from operations turned negative again at -$1.16 million after a brief positive spike in 2023. Coupled with ongoing modest capital expenditures, BluSky AI posted negative free cash flow for the year.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -5 | -1156258 | -3 | -375.4% |

| 2024 | -1 | -127139 | -1 | -107.5% |

| 2023 | 13 | 1242675 | -1 | +407.2% |

| 2022 | -4 | -902422 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 485.3 |

| 2024 | 28.4 |

| 2023 | -526.2 |

| 2022 | 12.2 |

Source: SEC companyfacts cache [F1].

Note: The current ratio below 1 indicates liquidity challenges; negative equity further underscores financial distress.

Growth Drivers & Constraints

BluSky AI’s growth thesis revolves around meeting accelerating demand for AI processing capacity through scalable modular data centers with integrated green energy solutions [S1][S8]. However:

- Supply Chain Vulnerabilities: Dependence on third-party modular data center providers exposes BluSky AI to potential delays due to manufacturing or shipping issues as well as design standardization challenges across jurisdictions. Specialized equipment needs like liquid cooling systems add complexity [S1][S17].

- GPU Procurement Risks: Reliance on a limited set of GPU suppliers such as NVIDIA and AMD amidst volatile global semiconductor supply chains creates risks related to price spikes and availability that could hinder scalability [S1][S17].

- Powered Land Scarcity: The company's strategy depends on acquiring powered lands—sites pre-equipped with committed utility power—which are limited and highly contested by larger hyperscale providers leading to higher acquisition costs or restricted geographic expansion [S6][S10].

- Regulatory Environment & Grid Dependency: Operating within existing U.S. energy grids subjects BluSky AI to restrictions on energy consumption tied to sustainability mandates that may increase operational costs or require investments in backup energy solutions like onsite renewables or storage systems [S1][S8][S12].

- Talent Acquisition & Retention: Competition from larger companies offering superior compensation hampers BluSky AI’s ability to attract skilled personnel essential for innovation and efficient deployment of complex technologies such as quantum encryption [S6][S20][S21].

Outlook & Key Milestones

While explicit forward guidance is limited, management highlights the critical need for additional financing to support rapid deployment plans across multiple sites leveraging modular infrastructure capabilities [S8][S16]. Key milestones investors should track include:

- Successful capital raises sufficient to cover near-term liabilities plus incremental capital expenditure

- Progress in securing powered land assets enabling geographic expansion

- Strategic partnerships renewal or expansion with GPU suppliers mitigating supply risks

- Initial commercial deployments generating recognized revenue streams (currently unreported)

- Regulatory approvals advancing renewable energy integration efforts reducing grid reliance costs

Capital Allocation & Returns

BluSky AI has not paid dividends historically nor plans to do so given persistent accumulated deficits totaling approximately $34.4 million through end-2025 [F1][S11]. The company frequently compensates employees and consultants with stock issuances due to constrained cash resources.

Capital expenditures have increased notably alongside infrastructure build-outs but remain modest relative to operating losses resulting in negative free cash flow estimated near -$1.2 million annually based on latest fiscal data [F1]. The approximate return on equity metric appears inflated due to severely negative shareholders’ equity rather than operational profitability—reflecting financial distress rather than efficiency.

Operating cash flows have deteriorated markedly while working capital shortfalls persist alongside minimal cash reserves below $1 million at year-end confirming reliance on external financing sources with attendant dilution risks if new funding proves difficult amid volatile OTC market trading conditions [F1][S13][S19].

Competitive Position & Risks

BluSky AI occupies an emerging but highly competitive niche challenged by dominant hyperscale cloud providers with superior capital resources enabling scale economies.

Risks include:

- Chronic liquidity shortages risking solvency without timely capital injections.

- Supply chain disruptions affecting modular component delivery and GPU availability impacting margins.

- Complex regulatory compliance related to environmental standards and cybersecurity increasing operational overheads.

- Market adoption uncertainties given nascent industry status.

- Concentrated executive leadership heightening governance risk if key personnel depart.

- Stock illiquidity due to penny stock classification limiting investor participation complicating fundraising efforts.

Conclusion & Considerations Going Forward

BluSky AI Inc. stands at a crossroads balancing rapid demand growth for AI compute infrastructure against severe financial constraints compounded by supply chain fragilities and asset scarcity. Its strategy combining modularity with renewable energy aligns with industry trends but is tempered by systemic liquidity challenges and intense competition.

Key investor considerations include monitoring capital raise progress, supplier relationships stability, commercial revenue realization milestones, powered land acquisitions success, and regulatory compliance developments shaping operational costs.

This report synthesizes public SEC filings up to April 3rd, 2026 without providing investment advice. Readers should consult multiple sources before forming views related to BluSky AI Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments