Smart Powerr Corp.'s Declining Revenue and Losses Challenge Growth Amid Energy Sector Transition

Smart Powerr Corp. faces steep revenue declines and persistent losses while shifting from waste energy recycling to energy storage solutions.

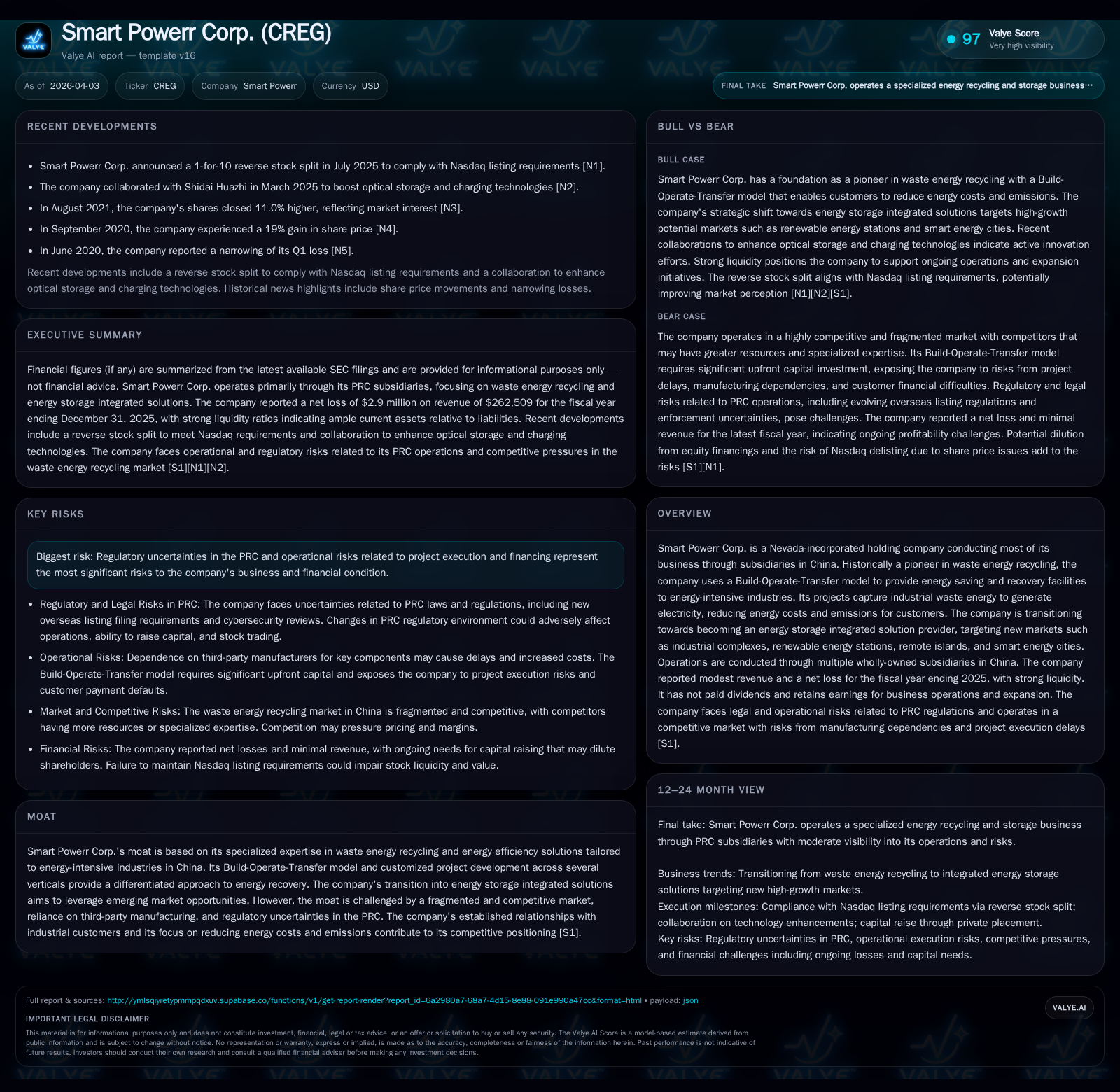

Smart Powerr Corp., incorporated in Nevada with operations primarily in China, experienced a nearly 70% revenue decline and deepening net losses through 2025 amid reduced project activity and economic headwinds. The company historically pioneered waste energy recycling using a Build-Operate-Transfer (BOT) model in heavy industries but is transitioning toward integrated energy storage solutions targeting new sectors. Despite strong liquidity and a substantial equity base, ongoing project delays, competitive pressures, and regulatory uncertainties in China challenge growth prospects. Operating cash flow turned positive in 2025, reflecting working capital dynamics rather than core operational improvements.

Company Background and Historical Performance

Smart Powerr Corp. is a Nevada holding company conducting most operations through subsidiaries in China. Formerly known as China Recycling Energy Corporation before rebranding, it pioneered waste energy recycling projects based on a Build-Operate-Transfer (BOT) model serving China's energy-intensive industries such as steel, cement, coking, and metallurgy plants [S1][S3][S9].

The BOT model involves significant upfront investment to build facilities that capture otherwise wasted industrial heat, pressure, and gases to generate electricity. These projects help customers reduce electricity costs by approximately 5–20%, lower emissions, and extend equipment lifespans through processes like desulfurization of flue gas [S1][S9].

However, revenues depend on the availability of industrial waste energy inputs; any slowdown or disruption at customer sites directly impacts Smart Powerr's income given compensation tied to actual energy supplied [S4].

Financial Performance Snapshot

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -3 | 67 | -3 | -86.0% |

| 2024 | -2 | -11 | -1 | -108.8% |

| 2023 | -1 | -68 | -1 | +83.2% |

| 2022 | -4 | 0 | -4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -2.0 |

| 2024 | -1.5 |

| 2023 | -0.7 |

| 2022 | -4.0 |

Source: SEC companyfacts cache [F1].

(All financial figures sourced from latest SEC filings as of fiscal year-end December 31)[F1]

Revenues sharply contracted by nearly 70% from the prior period to just over $260K in 2025 during fewer active projects and subdued customer demand. Operating losses deepened substantially exceeding $3 million annually while net income losses also widened.

Operating cash flow notably reversed from negative territory to positive $67 million in 2025 largely due to working capital management rather than improved core profitability or project performance.[F1] The company has not paid dividends historically nor announced plans to do so as it prioritizes funding ongoing operations and strategic initiatives.[S23]

Industry Context and Competitive Positioning

Smart Powerr’s competitive advantage lies in its proprietary technology for capturing industrial waste energy tailored for heavy industry clients within China’s manufacturing sector. This enables cost savings under tightening environmental regulations.[S1]

Its BOT contracts establish long-term customer relationships via customized projects producing continuous power generation revenues post-completion. Ancillary pollution control features add value by reducing equipment wear on client production lines.[S9]

Nonetheless the market is fragmented with increasing competition from firms specializing in particular technologies or verticals who may possess stronger financial resources or longer operating histories.[S18] Macroeconomic headwinds including slowing Chinese industrial output limit new project orders and available waste energy volumes.

Regulatory risks are material given the company's cross-border structure operating primarily through Chinese subsidiaries subject to evolving laws governing data security,[S10] foreign investment,[S19] anti-corruption enforcement,[S25] and overseas securities offerings.[S28]

Strategic Transition and Growth Outlook

Smart Powerr is actively shifting focus toward integrated energy storage solutions targeting sectors beyond legacy waste energy recycling. These include industrial complexes outside traditional metals industries; large-scale photovoltaic (PV) and wind power farms; off-grid remote islands lacking electricity access; and emerging "smart energy" cities integrating multiple clean energy sources.[S1][S3]

This strategy aligns with China's national priorities on renewable integration and carbon emission reduction. Success depends on disciplined entry into these nascent markets coupled with efficient engineering design through construction phases.

Risks that could restrain growth include government approval delays impacting project timelines; supply chain volatility affecting manufacturing; persistently weak demand if Chinese industrial activity remains subdued; pricing pressures from competitors; plus evolving policies potentially restricting overseas capital access needed for expansion.[S4][S8][S18]

Key Risks Identified

- Economic Sensitivity: Slowing or contracting Chinese economy reduces industrial activity and availability of waste energy critical for revenue generation under BOT contracts.[S4]

- Project Delivery Risks: Complex assembly processes create risk of delays or failures leading to lost sales or penalties.[S21]

- Customer Credit Risk: Dependence on customers' financial viability affects collections despite collateral arrangements under BOT agreements.[S21]

- Regulatory Complexity: Evolving PRC regulations on foreign listings,[S10] data privacy,[S25] anti-corruption,[S19] and securities oversight increase compliance burden.

- Competitive Pressures: Fragmented market with better-capitalized rivals threatens margin erosion.[S18]

- Capital Needs: Frequent external financing at potentially dilutive terms may be necessary given negative operating cash flows historically except for recent working capital effects.[S8][S24]

Returns and Capital Allocation

Return metrics remain deeply negative given persistent net losses approximating a negative two percent Return on Equity (ROE), calculated as net income divided by equity ($2.9 million loss against $143 million equity at FY end 2025).[F1]

The company has not declared dividends historically nor engaged in share repurchases as cash is reinvested to sustain operations amid ongoing losses.[S23]

Capital expenditures have been minimal relative to cash flows indicating focus on managing existing assets rather than aggressive new builds recently.[F1]

Liquidity remains robust supported by a very healthy current ratio near 14x driven by high current assets ($157 million) versus low current liabilities ($11 million), alongside substantial cash reserves carried forward from prior years ($139 million at end FY2022).[F1][S21]

Nevertheless the capital-intensive BOT model necessitates intermittent fundraising which could dilute shareholders if profitability does not improve promptly.[S24]

Outlook Considerations and Milestones To Monitor

Key indicators to watch include:

- New BOT project contract awards or order backlog updates signaling near-term revenue pipeline health.

- Progress reports confirming deployment of integrated energy storage solutions beyond traditional heavy industry customers validating strategic pivot.

- Regulatory developments affecting cross-border capital flows impacting financing options.

- Customer production trends reflecting stability of raw material supply essential for contracted power generation revenues.

- Competitive landscape shifts including entry of larger green technology players potentially compressing margins further.

Conclusion

Smart Powerr Corp.’s legacy strength as an innovator in waste energy recycling serving China's industrial sector faces significant challenges including steep revenue declines and mounting operating losses through FY2025. While strong liquidity provides short-term resilience, successful execution of its strategic pivot toward integrated energy storage solutions will be critical amid intensifying competition and complex regulatory environments.

Investment returns remain negative driven by unprofitable operations but future growth potential exists if new market strategies aligned with China's clean energy agenda are effectively realized.

Disclaimer: This analysis is based exclusively on publicly available SEC filings up to April 2026. It does not constitute investment advice but aims to provide an informed overview of Smart Powerr Corp.'s historical performance and strategic outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments