Aureus Greenway Holdings’ Capital Improvements and Seasonal Dynamics Shape Growth in Orlando’s Competitive Golf Market

The company operates two public golf country clubs near Orlando, emphasizing affordability and comprehensive amenities amidst profitability challenges.

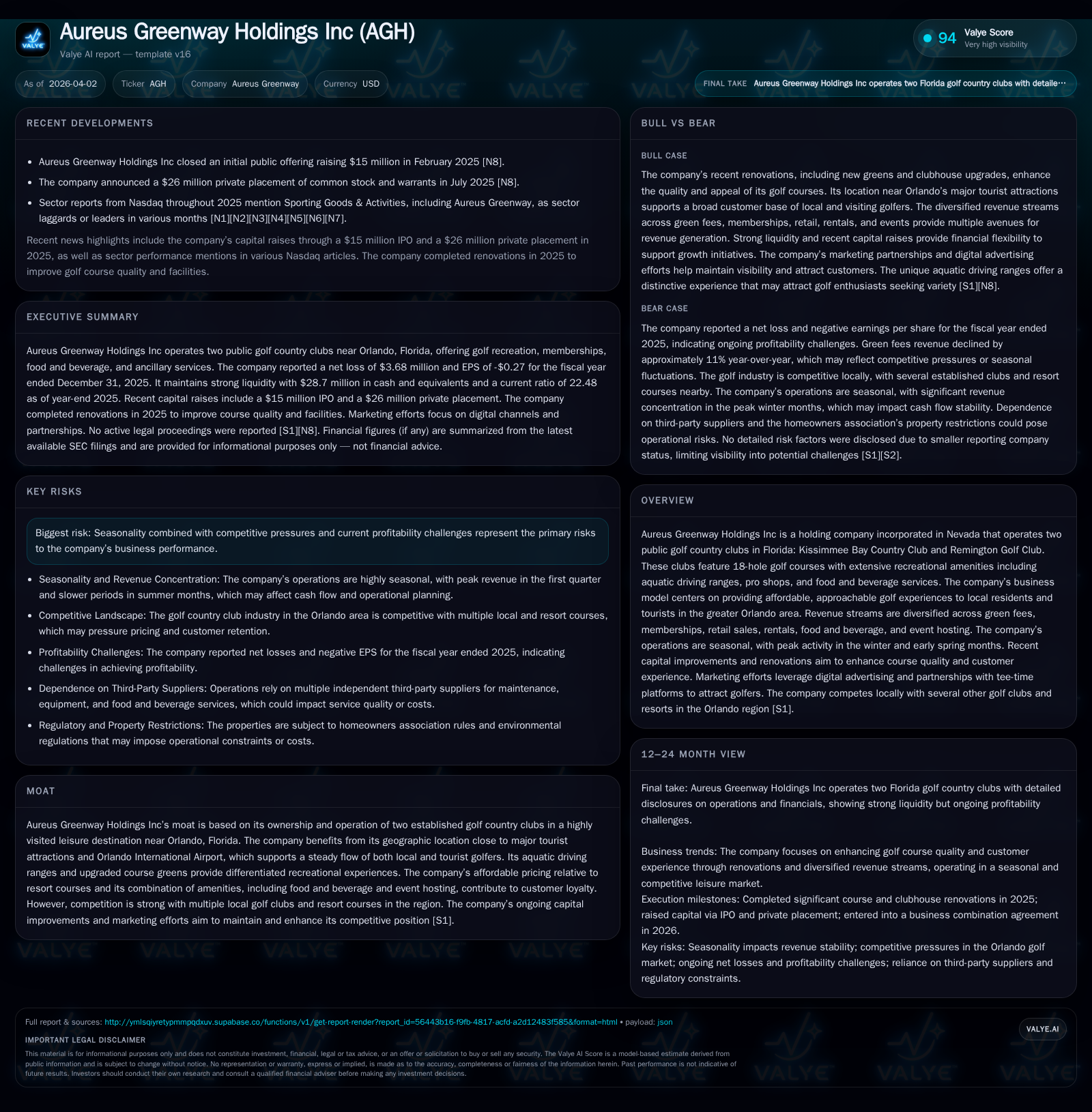

Aureus Greenway Holdings Inc manages two public golf clubs in the greater Orlando area, leveraging location and facility upgrades to bolster customer appeal. While it has demonstrated revenue diversity across green fees, memberships, food and beverage, and event hosting, the company faces significant seasonality and competition pressures that have impacted recent profitability. Substantial capital investments and marketing initiatives aim to fuel future growth, but operational cash flow remains negative as of fiscal year 2025 with ongoing losses.

Company Overview

Aureus Greenway Holdings Inc (AGH) operates two public golf country clubs—Kissimmee Bay Country Club and Remington Golf Club—in the greater Orlando area of Florida [S1][S8]. Incorporated in Nevada but headquartered in Florida, AGH’s assets comprise over 289 acres including two 18-hole golf courses with over 13,000 combined yards of fairways. Both clubs feature aquatic driving ranges—a distinctive amenity where golfers hit floater balls over water—pro shops offering retail golf products, clubhouses with food and beverage services, and event hosting capabilities [S1][S8][S12].

The clubs serve both local residents and tourists visiting the region’s popular attractions like Walt Disney World Resort. Their geographic proximity to Orlando International Airport positions them favorably for leisure travelers seeking approachable golf experiences priced significantly below exclusive resort courses [S1][S6][S10].

Historical Performance

AGH’s revenues derive from multiple segments: daily green fees form the largest share at approximately 64% of total gross revenue for FY2025; food & beverage services contribute around 21%; membership dues about 10%; with ancillary services rounding out the remainder [S7][S13]. This diversification helps stabilize cash flows somewhat during off-peak periods.

Despite revenue diversification, AGH reported operating challenges through recent fiscal years. Operating income declined from a near breakeven position (-$182k) in FY2024 to a significant operating loss of approximately -$4.4 million in FY2025 [F1]. Correspondingly, net income worsened from -$183k to -$3.7 million over the same period. Operating cash flows reversed from positive $89k in FY2024 to negative $2.0 million in FY2025 [F1]. The company’s capital expenditures notably increased by nearly eightfold—from roughly $127k in FY2024 to $1.07 million in FY2025—reflecting substantial renovation projects on course greens and clubhouse facilities [F1].

Across these years AGH maintained healthy liquidity with cash & equivalents totaling nearly $28.7 million as of December 31, 2025 [F1], giving it runway to invest through lean operational stretches caused by seasonality.

Financial Summary

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -4 | -2 | -4 | 1074008 | -1901.6% |

| 2024 | 0 | 0 | 0 | 126679 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | -11.2 |

| 2024 | 0 | -17.2 |

Source: SEC companyfacts cache [F1].

Operating income and net income show significant deterioration year-over-year largely driven by investment phases and competitive pressures [F1].

Business Model and Operations

AGH's strategy centers on providing affordable yet quality golfing experiences combining natural aesthetics, course variety, and multiple recreational offerings [S1][S8]. Both courses are under one mile apart offering players the opportunity for extended play (36 holes). Course layout variability—including tee box colors corresponding to skill levels—and ongoing course condition improvements aim to maintain customer engagement [S25].

Unique aquatic driving ranges utilize special floater balls rented by customers; these lightweight balls remain recoverable easily from water hazards, providing operational efficiencies versus traditional ranges [S12]. Pro shops stock apparel and equipment tailored more toward immediate needs rather than large inventory sales—with custom golf club orders handled on a pre-paid basis—minimizing capital tied up in inventory [S12].

Membership programs are relatively small—about 100 total members between the two clubs as of end-2025—reflecting a strategic focus on daily fee-paying golfers rather than emphasizing club memberships heavily [S13][S23]. This approach frees tee times for tourist guests during peak seasons.

Food and beverage is an important ancillary segment accounting for roughly one-fifth of revenues with targeted net margins near 20% through fresh menu offerings prepared onsite by experienced culinary staff [S13][S21]. This segment benefits from strategic bar areas functioning as social hubs within clubhouses.

Event hosting constitutes a growing part of ancillary revenue streams with rentable banquet rooms (notably at Kissimmee Bay), catering packages, and local tournaments contributing additional income diverse beyond pure golf play [S6][S13].

Industry Context and Competition

Orlando’s broader leisure market sees intense competition among more than six notable public golf courses within a two-hour radius including prestigious resort-linked venues such as Ritz-Carlton Orlando Grande Lakes and Disney’s Magnolia Golf Course [S14]. Compared to these upscale alternatives, AGH positions itself primarily on affordability while upgrading greens quality (notably Champion G12 greens installed at Kissimmee Bay in 2017) and improving clubhouse facilities [S14][S15]. These improvements also include sizeable renovations recently completed at Remington’s greens (seeding practices) aimed at mitigating aging turf risks [S15].

The company’s marketing leverages digital channels heavily—Google Ads targeted campaigns alongside partnerships with tee-time booking platforms like Tee Times USA—which advertise AGH facilities nationwide during peak seasons to capture tourist traffic [S14][S15]. This multi-pronged marketing effort attempts to offset regional seasonality where golfing slows considerably during Florida’s summer months (June–September) due to heat/humidity conditions [S11]. Peak revenue months concentrate strongly between January-Mid April annually.

Future Growth Prospects

AGH’s short-to-medium term growth strategy hinges on continuing capital investment focusing on:

- Further facility enhancements including clubhouse modernization especially at Kissimmee Bay,

- Maintaining top-tier course conditions via greens upkeep,

- Expanding event hosting capacities,

- Enhancing marketing reach through technology-driven platforms,

- Leveraging geographic advantages within high-tourism Orlando corridors.

While membership programs currently provide more stable recurring revenue streams less sensitive to seasonality (~10% share), management’s deliberate choice not to aggressively advertise memberships supports optimized utilization for daily fee golfers during peak periods [S13].

However, the sector-wide seasonality combined with fierce regional competition caps upside potential absent breakthrough brand differentiation or expansion into new assets or markets [S14][S18]. Moreover, profitability challenges stemming from rising labor costs (minimum wage pressures), regulatory compliance for food & alcohol services, environmental regulations concerning water usage and maintenance add further operational complexity [S11][S22][S24].

Continued dislocation from COVID-era tourism patterns or macroeconomic downturns affecting discretionary leisure spending could also constrain demand elasticity given reliance on both tourists and locals alike.

Financial Outlook & Milestones to Watch

No explicit forward guidance was disclosed for upcoming fiscal periods [N#],[S#], though investors should track:

- Post-renovation revenue trends,

- Membership growth rates versus daily fee usage,

- Food & beverage margin improvements,

- Event hosting uptake,

- Changes in operating leverage relative to fixed cost base.

Liquidity remains strong supported by a substantial cash position (nearly $28.7 million) providing flexibility for ongoing capex or strategic initiatives without immediate refinancing pressure despite current negative operating cash flows (-$2 million CFO in FY25) [F1],[S26],[S28]. Monitoring shifts in working capital or debt issuance will be relevant moving forward given recent private placement transactions raising ~$9 million gross proceeds early 2026 [S26],[S28].

Returns & Capital Allocation

ROE approximated -11% for FY2025 based on net losses relative to shareholder equity around $32.7 million — reflective of investments outpacing returns currently while repositioning occurs [F1].

No dividends or share buybacks were noted; capital allocation currently prioritizes reinvestment into course/clubhouse upgrades and marketing support aligned with growth objectives rather than shareholder returns at this stage [F1],[S29].

Risks Summary

Notable risks include pronounced seasonality effects leading to earnings volatility through weaker summer months; intense local competition limiting pricing power; regulatory burdens encompassing labor laws, health/safety standards especially around alcohol sales; environmental compliance obligations relating to land use by waterways; plus potential litigation or claims though none active presently according to filings [S4],[S9],[S18],[S27],[N#]. Negative operating incomes have widened substantially signifying operational leverage pressure amid investment cycles requiring careful management attention going forward.

Conclusion

Aureus Greenway Holdings operates in an attractive leisure market supported by favorable location characteristics near one of the world’s premier tourism hubs—Orlando—with asset improvements designed to enhance long-term competitiveness against well-funded competitors. The firm exhibits significant revenue diversity capped by dominant green fee contributions complemented by food/beverage event activities serving broad client demographics. However, its recent financially challenging profile characterized by widening losses amid rising costs/competitive intensity highlights the inherent difficulty balancing growth capex cycles against profitability targets within seasonal leisure industries. Liquidity is robust enabling pursuit of needed investments despite short-term negative cash flow metrics yet earnings recovery remains contingent upon optimizing utilization trends post refurbishment efforts while navigating external cost/regulatory pressures. Stakeholders monitoring this business should weigh subsequent period performance against incremental capex impact along with close tracking of market dynamics influencing discretionary consumer spend patterns locally vs tourist inflows.

This analysis is based solely on publicly available information summarized herein without any speculative assumptions or undisclosed projections. It is intended solely for informational purposes without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments