CannaPharmaRX's Pursuit of Scale and Market Expansion Amid Financial Pressure

CannaPharmaRX balances aggressive cultivation expansion and European market entry with acute liquidity and debt challenges.

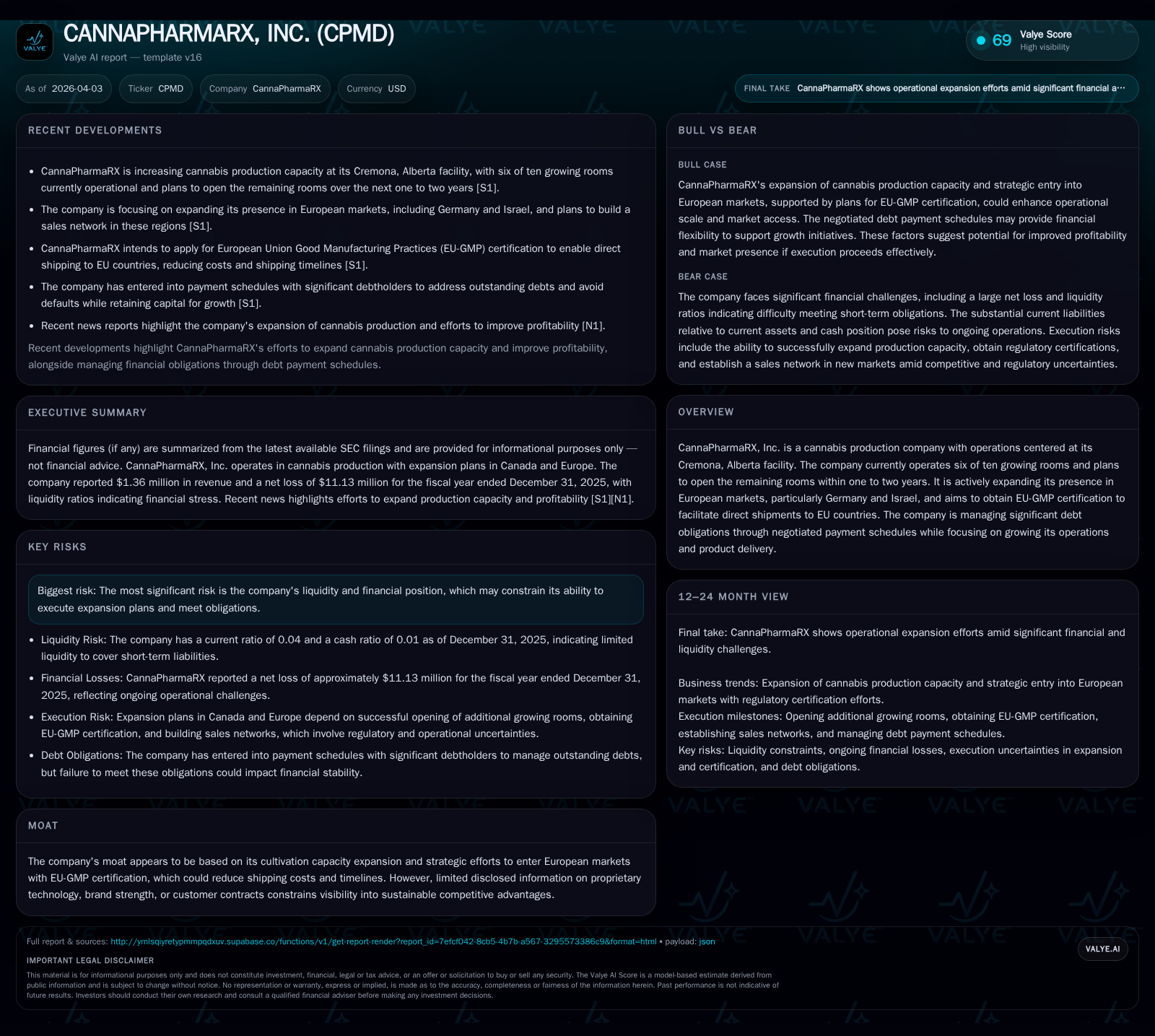

CannaPharmaRX has grown its cannabis production revenue from zero to over $1.36 million between FY2021 and FY2025, driven by scaling its Cremona facility’s cultivation footprint. The company targets medicinal cannabis markets in Germany and Israel, leveraging planned EU-GMP certification to enable direct shipments within the European Union. Despite operational progress, the company faces severe liquidity pressures with a working capital deficit near $27 million and related party debts exceeding $14 million under structured repayment plans. Operating cash flow losses have narrowed but remain negative, while net losses expanded amid restrained capital expenditures. Negative equity nearing $30 million complicates financial health metrics, though modest share repurchases have been executed as part of capital management efforts.

From Startup to Scale-Up: Tracking CannaPharmaRX’s Revenue and Capacity Growth

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1362163 | -11 | -1 | -3 | +66.1% | -12.4% |

| 2024 | 820137 | -10 | -2 | -4 | ||

| 2022 | 0 | -9 | -1 | -5 | +3.4% | |

| 2021 | 0 | -9 | -2 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($) | ROE% |

|---|---|---|---|

| 2025 | 350000 | -794621 | 36.9 |

| 2024 | 350000 | -1697232 | 50.0 |

| 2022 | 49.2 | ||

| 2021 | 68.3 |

Source: SEC companyfacts cache [F1].

CannaPharmaRX has transitioned from reporting virtually no revenues in fiscal years 2021 and 2022 to generating top-line revenues surpassing $1.36 million by the end of 2025 [F1]. This revenue growth aligns with strategic expansion of its cultivation footprint at the Cremona, Alberta facility where six out of ten planned grow rooms are operational as of early 2026 [N1]. These grow rooms are key controlled environments optimized for cannabis plant cultivation that directly influence production output.

The company achieved a notable 66% increase in revenue from FY2024 ($820K) to FY2025 ($1.36M), reflecting initial commercial traction after several years focused on infrastructure development [F1]. Partial utilization of capacity indicates a phased approach toward full deployment anticipated within one to two years, emphasizing measured scaling.

European Market Entry Strategy: Targeting Germany and Israel with EU-GMP Certification

A cornerstone of CannaPharmaRX’s growth plan is penetrating medicinal cannabis markets in Europe—specifically Germany and Israel [N1], [S6]. To facilitate this expansion, the company is pursuing European Union Good Manufacturing Practices (EU-GMP) certification. Achieving this certification will allow direct shipments into EU countries, reducing reliance on intermediaries that increase costs and extend delivery times.

EU-GMP status represents a critical regulatory credential enabling pharmaceutical-grade cannabis distribution within strict European frameworks. This could lower logistics overheads including cross-border transportation and customs clearance delays. However, regulatory environments remain complex and subject to change, presenting timing uncertainties and potential cost implications for certification attainment [S3].

Financial Position Under Strain: Managing Debt Burdens and Liquidity Risks

Despite operational advancements, CannaPharmaRX faces severe liquidity challenges underscored by a working capital deficiency around $27 million as of September 30, 2025 [S11], consistent with a current ratio near 0.04 at fiscal year-end 2025 [F1]. This imbalance indicates current liabilities far exceed current assets, elevating default risk.

A significant portion of liabilities comprises related party debt totaling approximately $10.76 million plus accrued interest of about $3.25 million as of late 2025 [S11], representing over $14 million owed internally. To address these obligations while maintaining liquidity, the company has negotiated structured repayment schedules with key creditors [S13]. These arrangements allow phased repayments aligned with cash flow generation rather than immediate lump-sum payments.

The filings highlight continued substantial doubt regarding the company's ability to continue as a going concern absent effective restructuring measures [S7], reflecting common challenges among emerging cannabis cultivators burdened by legacy debt amid fluctuating markets.

Operational Efficiency and Profitability Trends: Margins and Cash Flows

Profitability remains elusive with net losses expanding from approximately -$8.53 million in FY2022 to -$11.13 million in FY2025 despite revenue growth [F1]. Operating income remains negative but improved slightly from -$5.21 million in FY2022 to about -$3.35 million in FY2025, indicating gradual efficiency gains during production ramp-up.

Operating cash flow improved significantly (+53% YoY from FY2024) yet stayed negative at roughly -$789K in FY2025 [F1]. Capital expenditures were minimal at just over $5K for the year, reflecting tight control on spending but potentially limiting future capacity expansion or upgrades necessary for efficiency improvements.

Capital Allocation Amid Negative Equity and Cash Flow Pressures

The balance sheet shows deeply negative equity near -$30.15 million at fiscal year-end 2025 due to accumulated losses exceeding capital contributions [F1]. This distorts traditional metrics like Return on Equity (ROE), which appears positive (~37%) mathematically but does not reflect sustainable profitability.

Despite financial constraints, CannaPharmaRX conducted modest share repurchases totaling around $350K recently [F1], possibly aiming to stabilize equity or signal confidence during restructuring phases. No dividends have been declared since inception, aligning with industry norms prioritizing reinvestment or debt servicing.

These capital allocation decisions illustrate the challenge of balancing scarce resources amid ongoing losses against strategic steps intended to support shareholder value during turnaround efforts.

Milestones and Risks Ahead: Key Factors for Investors

Investors should monitor several critical milestones:

- Full activation of the remaining four grow rooms at Cremona will significantly affect production scalability.

- Successful attainment of EU-GMP certification is essential for pharmaceutical-quality market access in Europe.

- Progress in debt reduction through adherence to repayment agreements will be vital for improving liquidity.

- Regulatory developments across target markets could introduce compliance costs or access delays [S3].

- Ability to raise capital or refinance existing obligations may determine funding availability for organic growth versus dilution or asset sales.

These factors collectively shape whether CannaPharmaRX can execute its dual strategy amid evolving legal frameworks and market dynamics characteristic of the cannabis industry.

This analysis uses information solely from publicly available SEC filings through early April 2026 and verified news sources without speculative extrapolation beyond disclosed data. The case of CannaPharmaRX exemplifies the challenges faced by emerging cannabis producers balancing ambitious growth initiatives with significant financial headwinds.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments