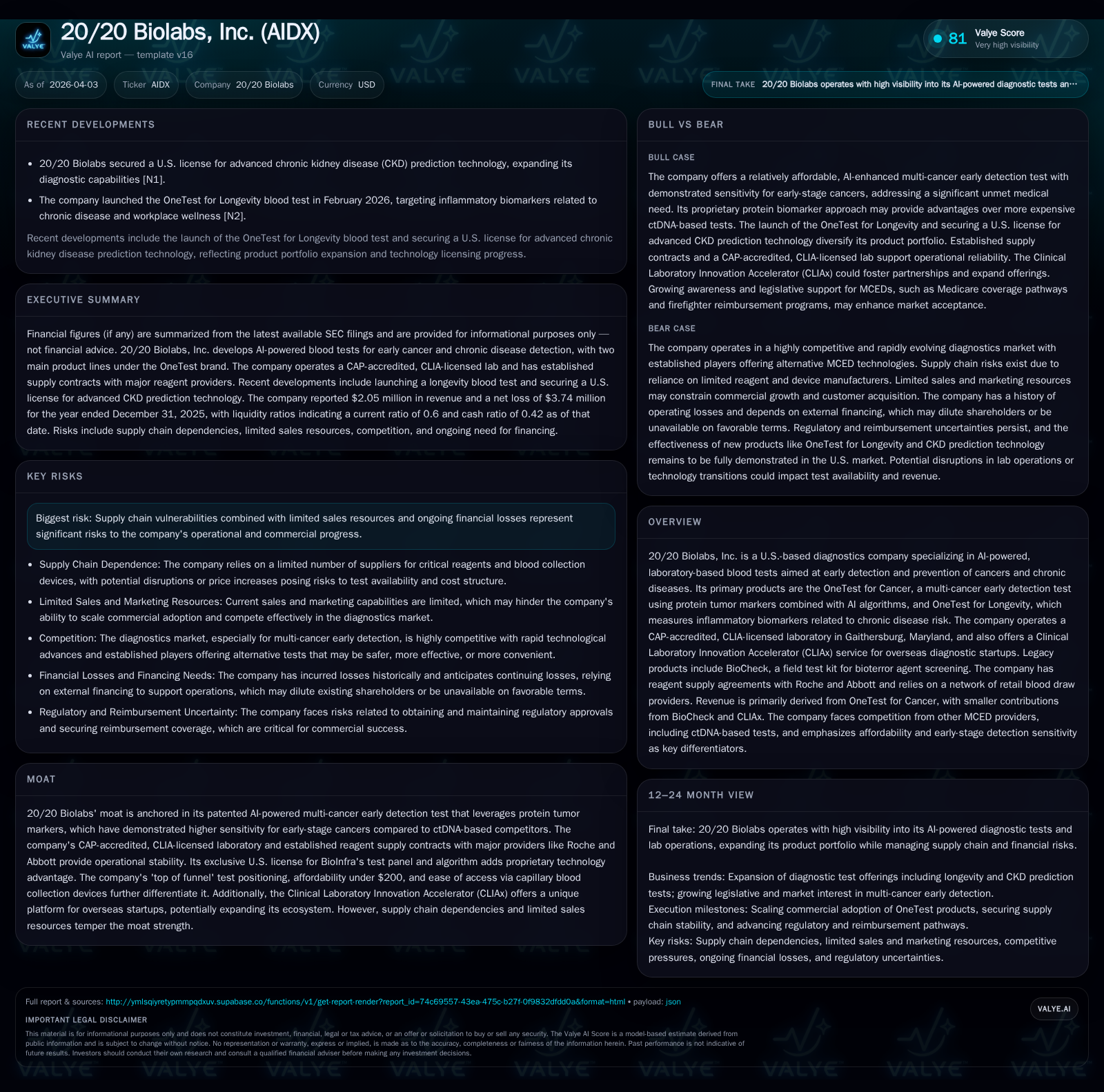

20/20 Biolabs’ Transition from COVID-Driven Profits to AI-Powered Diagnostics Growth Strains Liquidity

The company advances multi-cancer and chronic disease early detection tests amid operational losses and supply chain risks.

20/20 Biolabs, Inc. leverages patented AI-driven blood tests for early cancer detection and chronic disease risk while operating a CAP-accredited, CLIA-licensed laboratory. Historically profitable during the COVID-19 testing surge, the company has reverted to operating losses post-pandemic with revenue primarily reliant on their OneTest for Cancer product. New product launches, including the OneTest for Longevity, and a unique Clinical Laboratory Innovation Accelerator program offer paths to diversify revenue but entail commercialization challenges due to limited sales resources and complex regulatory environments. Supply chain dependencies and the need for additional capital raise significant operational risks in sustaining growth and scaling returns.

Company Overview and Historical Performance

20/20 Biolabs, Inc. is a U.S.-based diagnostics company focused predominantly on AI-powered, laboratory-based blood tests targeting early detection of cancers and chronic diseases. The company's key commercial product is OneTest for Cancer, a multi-cancer early detection (MCED) test that integrates protein tumor markers with proprietary AI algorithms. It recently launched OneTest for Longevity in February 2026, which evaluates inflammatory biomarkers to estimate chronic disease risk. The company operates a College of American Pathologists (CAP)-accredited and Clinical Laboratory Improvement Amendments (CLIA)-licensed laboratory located in Gaithersburg, Maryland. Alongside its test offerings, it runs the Clinical Laboratory Innovation Accelerator (CLIAx), a shared CLIA lab service aimed at supporting overseas diagnostics startups entering the U.S. market.

Historically, 20/20 Biolabs achieved profitability during the COVID-19 pandemic in 2021 and 2022 largely due to high-margin SARS-CoV-2 testing revenues which ceased in mid-2023. Since then, the firm has transitioned back into operating losses as it shifted focus toward its MCED solution and new product launches [S1].

Recent annual financials highlight this transition:

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

(Source: [F1])

In 2025, revenues totaled just over $2 million with net losses approaching $3.7 million reflecting investments in R&D and commercialization efforts post-COVID testing decline.

Revenue Drivers and Product Portfolio

Revenue composition remains heavily skewed towards OneTest for Cancer which accounted for approximately 88% of total sales in 2025; BioCheck—a field test kit for screening bioterrorism agents—yielded roughly 8% of revenues while CLIAx accounted for around 4% [S1]. This concentration reflects both market demand and established relationships with retail blood draw providers numbering around one thousand nationwide [S16].

The OneTest for Cancer leverages protein tumor markers identified via immunoassay technology sourced primarily through Roche Diagnostics' Cobas E411 system under long-term reagent contracts guaranteeing pricing stability. Abbott provides supplies for general chemistry markers utilized within the panel [S7]. However, Cyfra and IL-6 markers are currently only available through Roche platforms domestically; alternative sourcing pathways such as Luminex or ELISA assays exist but have not been broadly implemented.

OneTest differentiates itself by combining protein biomarker panels that offer potentially greater sensitivity for early-stage cancers versus circulating tumor DNA competitors—a critical factor given survival sharply improves when cancers are detected at stages I or II rather than later stages [S1]. Notably, recent Medicare legislation establishes coverage pathways for MCED screenings from 2028 onward potentially bolstering demand if reimbursement frameworks materialize favorably.

The recent launch of OneTest for Longevity targets inflammatory biomarkers linked to chronic illness risk—a segment adjacent to cancer screening yet unproven commercially thus far with initial public market reaction indicating investor uncertainty after launch [N2][S1]. The longevity test also offers a workplace wellness variant aimed at self-insured employers but faces hurdles around customer acquisition costs and reimbursement clarity [S23]. This strategic extension represents an effort to diversify revenue beyond oncology but requires significant sales infrastructure.

The CLIAx initiative is relatively nascent yet innovative—it provides a shared U.S.-based certification platform enabling foreign diagnostics startups to enter American markets without costly individual lab setups. While currently modest in revenue share (~4%), its induced ecosystem effects may support inorganic growth opportunities via potential investments or acquisitions through an associated fund being developed [S23].

Operational Challenges and Risks

Despite growth prospects from legislative tailwinds and product innovation, substantial operational risks persist:

Supply Chain Dependence: The company relies heavily on Roche and Abbott reagent supply agreements that assure consistent pricing but hinge on single-source components such as capillary blood collection devices produced by only three or four approved manufacturers subject to potential disruption or price increases [S7][S16]. Second-source qualification efforts are ongoing but incomplete.

Limited Sales & Marketing Resources: Commercial scalability is constrained by a nascent sales force lacking broad distribution partnerships or established payer contracts especially relevant since primary revenue derives from consumer self-pay models; sustained sales investment is requisite for broader employer or insurer penetration [S16][S23].

Capital Intensity & Liquidity: Operating cash flows remain negative with free cash flow deficits exceeding $1.9 million in the latest fiscal year amidst only $1 million in cash equivalents at year-end raising concerns regarding runway without further financing [F1][S1]. Subsequent capital raises near year-end included $5 million via private placement plus convertible debt emphasizing continued liquidity needs.

Regulatory Environment: Diagnostic products operate under evolving regulatory frameworks including FDA’s attempted expansion of LDT oversight ultimately vacated by court rulings—however future legislation could impose costly clinical trials delaying product rollouts. Compliance measures covering HIPAA/HITECH privacy laws plus healthcare fraud statutes add layers of cost and legal exposure requiring robust internal controls which historically have faced some challenges including accounting restatements implicating governance vigilance [S4][S10][S12][S18].

Future Growth Prospects

20/20 Biolabs' near-term growth depends largely on successful commercialization scaling of its OneTest franchises:

Medicare Coverage Opportunity: Passage of the Medicare Multi-Cancer Early Detection Screening Coverage Act establishes formal reimbursement from next decade—successful engagement here could unlock widespread adoption among Medicare beneficiaries catalyzing volume growth given current reliance on out-of-pocket payers ([S1]).

Longevity Test Expansion: Introduction of inflammation-driven longevity biomarker testing targets a sizable population concerned with chronic conditions offering subscription business model potential albeit unproven market acceptance creates execution risk ([N2][S23]).

CLIAx Platform Development: Expanding this accelerator may create diversified income streams through licensing or equity stakes in partner startups requiring capital deployment but promising an ecosystem play not typical among single-product diagnostics companies ([S1][S23]).

However, growth may be capped or delayed by limited internal distribution capabilities necessitating significant investment in hiring sales professionals alongside ramping payer negotiations critical to accessing insured populations beyond direct consumer buys ([S16][S23]). Furthermore, supply chain stability especially amid few suppliers of key collection devices constitutes a bottleneck that could disrupt timely test delivery ([S7][S16]). Regulatory uncertainties including potential future FDA enforcement of LDT approvals pose long-term cost burdens influencing pricing power ([S4][S10]). Lastly, continuous capital raises dilute shareholders and create financial risk if commercial returns do not accelerate sufficiently ([F1][S19]).

Returns and Capital Allocation Dynamics

Due to sustained operating losses netting nearly $3.7 million in 2025 against modest revenues just over $2 million alongside negative free cash flow exceeding $1.9 million suggests constrained capacity to generate positive return metrics at present ([F1]). The company's equity base is modest relative to losses resulting in an anomalously high calculated ROE figure driven by low equity denominator which may not be meaningful as a performance indicator under these circumstances.

No dividends or share repurchases have been declared historically consistent with typical early-stage diagnostics companies focusing financial resources towards scale-up operations instead ([F1]). Capital allocation priorities are firmly tilted towards investing in R&D, clinical validations, sales force expansion, and maintaining compliance infrastructures necessary to drive regulatory approvals and market penetration ([S1],[S23]). Further capital infusions have come through private placements and convertible debt indicating willingness from investors to support growth plans though timing and terms remain uncertain which could impact dilution levels ([F1],[S19]).

Monitoring Milestones & Outlook Considerations (Analysis)

Key milestones warranting close monitoring include real-world uptake statistics for both OneTest products notably post-Medicare policy implementation; successful scaling of workforce able to reach employers/self-insured groups; evidence of stable supply chain operations particularly capillary device availability; regulatory developments impacting LDT authority; effective integration or monetization outcomes from CLIAx partner collaborations; quarterly cash burn trends relative to fundraising activity; finally evaluation of customer retention within subscription models being trialed.

Emergence as a profitable enterprise hinges on translating technological capabilities validated clinically into volumes sufficient enough combined with improved reimbursement that can offset sales/marketing expenses while maintaining quality control integrity—all within an increasingly regulated environment fraught with competition.

Conclusion

20/20 Biolabs occupies an intriguing niche at the intersection of AI technology and precision diagnostics focused on impactful unmet needs like early cancer detection and chronic disease prevention. While their patented multi-cancer protein marker approach coupled with AI analytics differentiates them technically versus ctDNA-based peers along with novel service offerings like CLIAx enhancing ecosystem reach—the pathway forward demands addressing considerable hurdles around capital adequacy, expanding commercial reach beyond modest self-pay segments, mitigating fragile supply chains reliant on few vendors especially FDA-cleared capillary blood devices; navigating looming regulatory shifts; all without the cushion offered by large scale revenues presently.

Pragmatic focus on securing Medicare reimbursement coverage starting expectedly in two years appears pivotal alongside successful broadening into longevity-related diagnostics potentially leveraging consumers’ growing wellness awareness paired with digital engagement tools such as coupon-driven incentivization pending commercial validation.

Ultimately sustained external financing will be crucial absent near-term operating profits; investors should watch closely corporate execution against milestones specified above while recognizing inherent sector volatility characteristic of emerging biotech/digital health plays reliant on predictive AI diagnostics.

This analysis synthesizes publicly available documents including the company’s latest SEC filings and recent news releases as of April 2026. It aims solely to provide detailed insight on business fundamentals without making investment recommendations or forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments