MDJM LTD’s UK Real Estate Revival and Cost Discipline Reshape Outlook

An 85% revenue surge contrasts with ongoing losses, driven by a new sales channel and tight expense management.

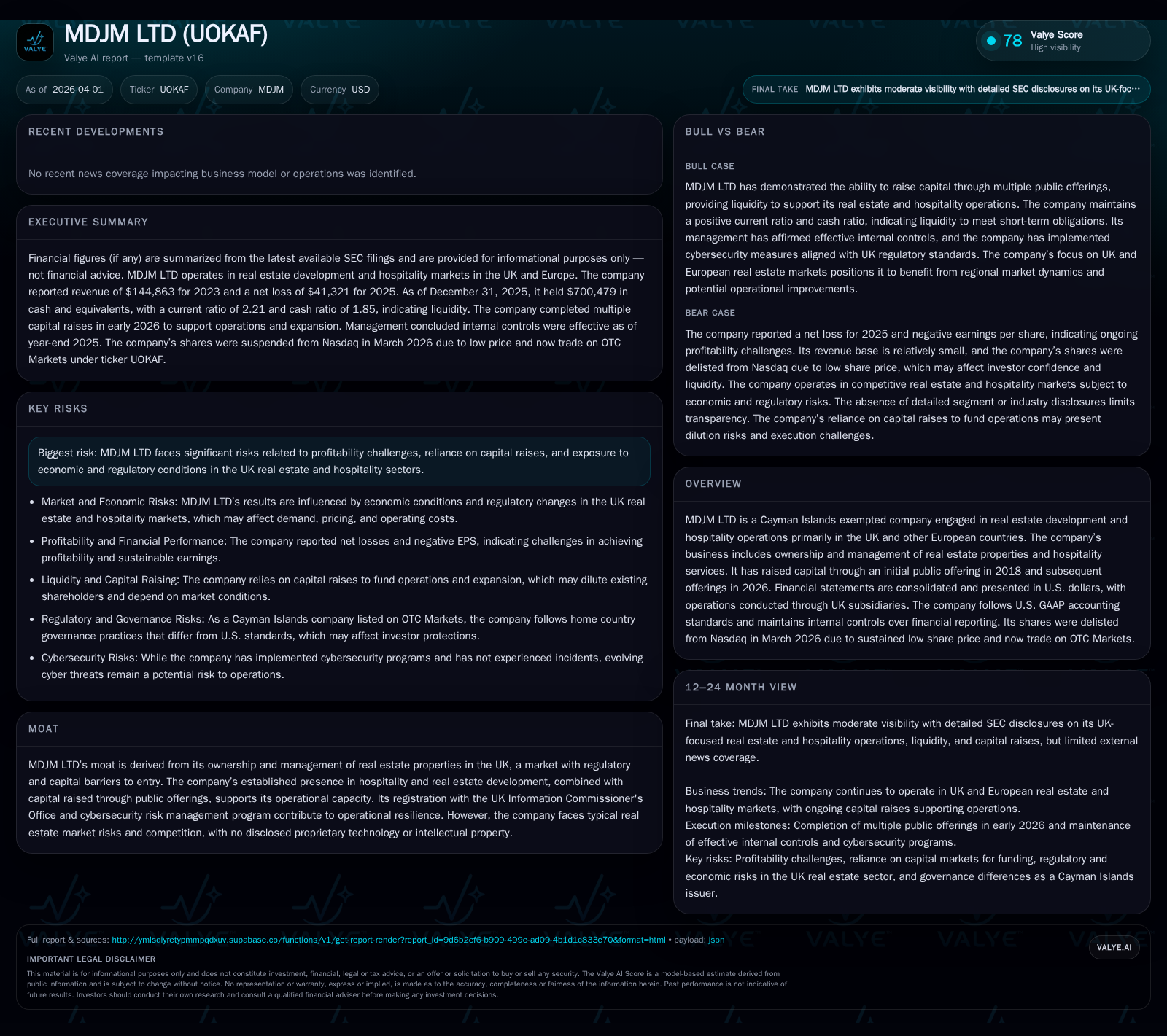

MDJM LTD reported an 85% increase in revenue for 2025 following the launch of a third-party sales channel, primarily within its UK real estate and hospitality operations. This growth coexists with persistent operating losses, albeit reduced compared to prior years, as the company executed stringent cost reductions including the removal of stock-based compensation. MDJM’s capital structure evolved through public offerings supporting its focus on UK asset acquisitions. Despite operational progress, liquidity challenges and market risks remain critical headwinds.

Revenue Surge Fueled by New Third-Party Channel in 2025

MDJM LTD experienced an exceptional revenue jump to $89.7 million in 2025, an increase of $41.3 million or 85% over the prior year’s $48.4 million [F1][S1]. This leap was primarily attributed to the strategic establishment of a third-party sales channel during the year that expanded reach within the UK hospitality and real estate sectors.

Cost Reductions and Stock-Based Compensation Absence Drive Operating Expense Decline

Operating expenses decreased sharply by $1.58 million or 56% to approximately $1.26 million in 2025 from $2.84 million in 2024 [S1]. This significant reduction stemmed mainly from the absence of stock-based compensation charges which accounted for roughly $1.49 million in payroll-related costs recognized during 2024 but wholly eliminated in 2025 following management's cost-cutting initiatives [S1]. Payroll expense itself slumped by an extraordinary 87%, accompanied by reduced office expenses and administrative overheads.

Professional fees grew by 67% to $757 thousand, reflecting increased legal, audit, investor relations, and SEC compliance demands tied to both capital raising activities and reporting obligations after delisting from Nasdaq [S1].

Evolving Capital Structure Supporting UK Expansion and Liquidity Position

Since its initial public offering (IPO) in late 2018, which generated net proceeds close to $5.7 million post-underwriting costs [S10], MDJM has deployed most of this capital into acquiring UK-based real estate assets ($3.97 million utilized). In February 2026, the company completed a follow-on underwritten offering delivering gross proceeds near $6 million before underwriting discounts [S19]. These funds were earmarked for further asset acquisition aimed at reinforcing MDJM’s focused footprint across regulated UK markets.

Cash and cash equivalents were reported at approximately $700 thousand by December 31, 2025 [F1], enabling modest liquidity cushioning as working capital rose by about 44% year-over-year [S14]. Yet, operating cash flow remains negative reflecting ongoing investment outflows and operational expenses [F1].

Profitability Pressures Continue Despite Operational Progress

Despite top-line momentum and strict expense management, MDJM continued reporting operating losses with an operating income deficit of roughly -$1.17 million for FY2025 versus a more substantial loss near -$2.79 million the prior year [F1]. Net income improved dramatically but remained negative with an approximate loss of $41 thousand compared to over -$3.19 million previously [F1].

Cash flow from operations remained negative around -$1.09 million [F1], underscoring persistent free cash flow challenges compounded by elevated capex spending.

Real Estate Asset Focus and Geographic Concentration in the UK Market

Following complete deconsolidation of its former Chinese variable interest entity (VIE) during 2025—which eliminated China-based fixed assets altogether—MDJM’s entire net fixed asset base is concentrated within the United Kingdom [S1][S4]. This narrower geographic footprint focuses competitive advantage on markets characterized by high regulatory barriers to entry for real estate developers.

The company remains attentive to sector-specific risks including cyclical exposure inherent to both real estate development cycles and hospitality demand fluctuations amid prevailing economic conditions [S21].

Capital Allocation: IPO, Follow-on Offering and Impact on Balance Sheet

MDJM deployed its IPO proceeds primarily toward purchasing UK properties ($3.97 million), adhering to its stated intent to bolster its asset base rather than returning capital through dividends or share repurchases [S10]. Capital allocation thus reflects reinvestment logic suitable for growth-stage real estate entities retaining limited profit distributions.

Registered direct offerings completed as recently as March 2026 further supplemented equity capital with over $2 million gross proceeds yet remained unutilized as of filing date [S17][S19], potentially positioning MDJM for future acquisitions or working capital needs.

Equity grew approximately 19% year-over-year reaching about $4.26 million by end-2025 consistent with these capital raises despite net losses reducing retained earnings [F1].

Key Metrics Overview: Performance Trends in Revenue, Profitability, Cash Flow, and Capex

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -1087348 | -1 | +98.7% | ||

| 2024 | -3 | -1060717 | -3 | -174.8% | ||

| 2023 | 144863 | -1 | -599365 | -1 | -67.9% | +46.1% |

| 2022 | 450634 | -2 | -1587117 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -1449874 | -1.0 |

| 2024 | -1096465 | -89.0 |

| 2023 | -29.9 | |

| 2022 | -43.7 |

Source: SEC companyfacts cache [F1].

*Capex not disclosed for FY22+

This table reveals volatile revenue patterns with declines followed by recovery aligned with structural shifts emphasizing the UK market. Despite improved operating efficiency leading to reduced losses between FY24-FY25 (-58%), MDJM remains unprofitable while expending growing amounts on property investment.

This analysis is based strictly on publicly available regulatory filings dated up to April 2026 without forward-looking statements beyond documented plans or disclosed guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments