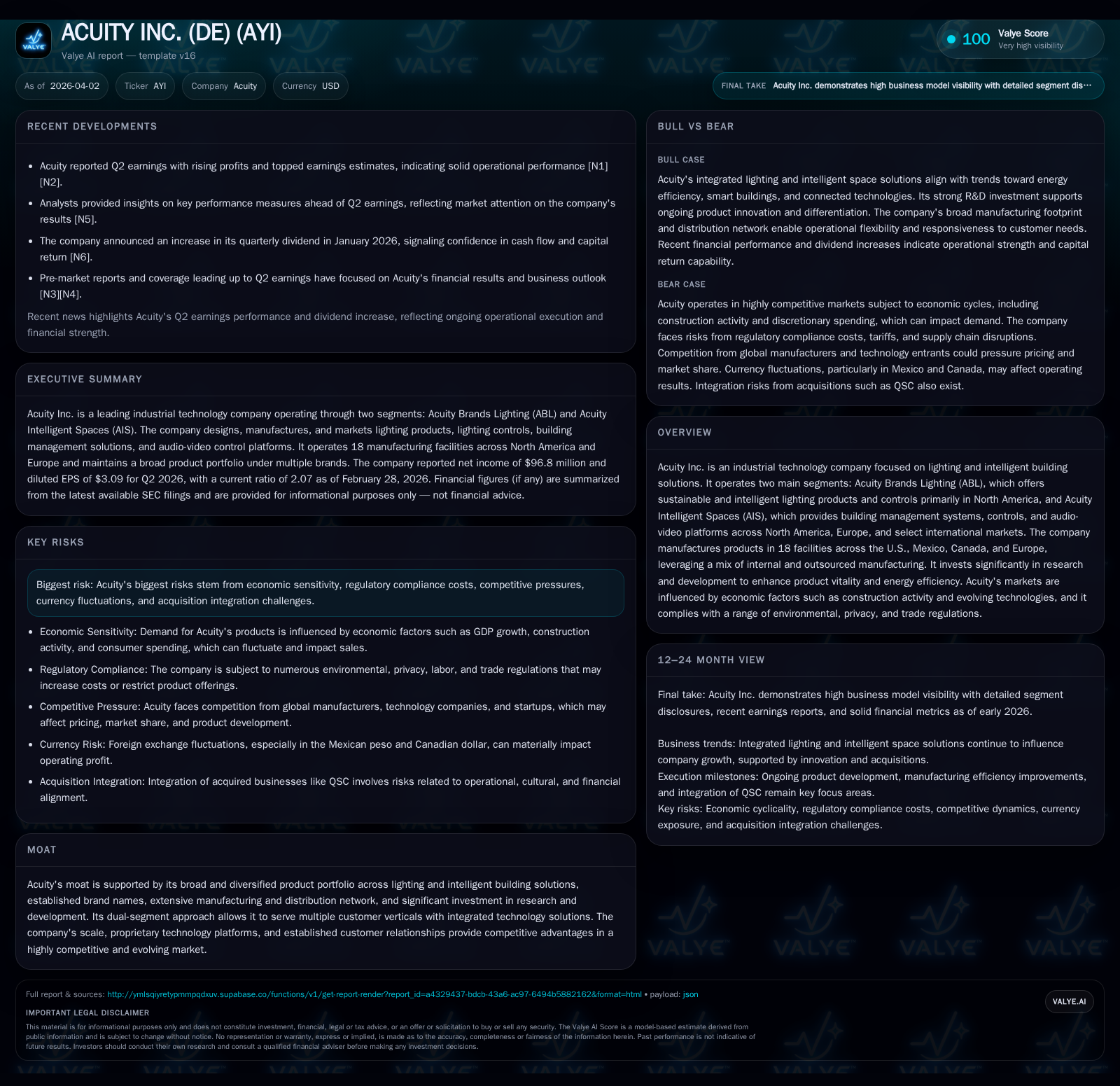

Acuity Inc.’s Dual-Segment Strategy Drives Revenue Growth Amid Margin Pressures and Strategic Investments

Acuity Inc. leverages its lighting and intelligent building solutions segments to deliver revenue growth supported by acquisitions and innovation, while managing rising costs and capital allocation for sustained expansion.

In fiscal 2025, Acuity Inc. achieved a 13.1% revenue increase to $4.35 billion, driven primarily by the QSC acquisition and organic growth in its Acuity Intelligent Spaces (AIS) segment alongside steady performance in Acuity Brands Lighting (ABL). Despite a slight contraction in operating margin due to elevated selling, administrative expenses, special charges, and higher interest costs, the company generated robust free cash flow and invested strategically in R&D and capital expenditures. Currency fluctuations and regulatory compliance remain ongoing considerations. The company’s focus on integration of recent acquisitions and scaling smart building platforms underpins its growth outlook.

Revenue Growth Driven by Acquisition and Organic Expansion

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 397 | 601 | 564 | 68 | -6.2% |

| 2024 | 423 | 619 | 553 | 64 | +22.1% |

| 2023 | 346 | 578 | 473 | 67 | -9.9% |

| 2022 | 384 | 316 | 510 | 57 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 21 | 119 | 533 |

| 2024 | 18 | 89 | 555 |

| 2023 | 17 | 267 | 511 |

| 2022 | 18 | 515 | 260 |

Source: SEC companyfacts cache [F1].

Acuity Inc. reported FY2025 net sales of $4.35 billion, marking a 13.1% increase compared with the prior year [F1][S1]. This growth was predominantly fueled by the full-year impact of the QSC acquisition within the Acuity Intelligent Spaces (AIS) segment, which contributed $428.6 million in net sales during fiscal 2025 [S1][S13]. Organic sales gains were supported by expansion of Atrius® smart building platform offerings and Distech Controls® solutions.

The Acuity Brands Lighting (ABL) segment posted modest growth of 1.1%, driven by stronger sales through expanded independent agency networks and direct channels, partially offset by decreased corporate account sales related to timing shifts in renovation projects [S13]. These results reflect the company’s dual approach of emphasizing innovation while broadening customer access.

Margin Trends Reflect Cost Pressures during Operational Leverage

Gross profit increased by $296.8 million or 16.7%, reaching $2.08 billion in FY2025 with gross margin improving by 140 basis points to 47.8%, supported by favorable material costs despite upward pressure from tariffs and production expenses [F1][S1].

Selling, distribution, and administrative (SD&A) expenses rose sharply by nearly 21% ($256.5 million), driven mainly by higher employee-related costs, amortization of acquisition-related intangibles, and nonrecurring special charges totaling $29.7 million linked to asset impairments and severance programs [F1][S1][S10].

Net interest expense moved from income of $4.5 million in prior year to an expense of $22 million in FY2025 due primarily to debt service on borrowings incurred for the QSC acquisition [F1][S15]. Miscellaneous expenses also increased significantly to $41.7 million primarily because of a non-cash pension settlement charge recorded late in FY25.

As a result, net income declined by 6.2% year-over-year to $396.6 million despite a modest rise in operating profit (+1.9%) to $563.9 million; operating margin contracted from 14.4% to 13%, underscoring integration-related cost challenges [F1][S1]. Diluted earnings per share declined from $13.44 to $12.53 reflecting reduced net income alongside share count changes.

Segment Synergies Enable Diversified Market Coverage

Acuity operates two complementary business segments that together provide resilience against market cyclicality:

ABL offers a comprehensive portfolio including luminaires under brands like Lithonia Lighting®, Aculux™, SensorSwitch®, targeting commercial new construction, renovation, retrofit applications mainly in North America through diverse channels including independent agencies, distributors, retailers, and OEM customers [S12][S18]. The segment integrates advanced electronics such as LED drivers and controls platforms enhancing energy efficiency.

AIS drives growth through Atrius® cloud-based spatial intelligence platforms combined with Distech Controls® building management systems managing HVAC, refrigeration, lighting shades plus QSC’s unified audio-video-control hardware/software products suited for complex environments like airports or enterprise campuses across North America and parts of Europe [S21].

This dual approach facilitates cross-selling opportunities while adapting product offerings based on local regulations such as energy codes and evolving customer sustainability demands.

Capital Deployment Balances Growth Investment with Shareholder Returns

Acuity demonstrates disciplined capital allocation balancing reinvestment with returns:

- Operating cash flow totaled $601.4 million for FY2025 versus capital expenditures near $68.4 million yielding free cash flow around $533 million despite inflationary raw material pressures [F1][S9].

- Dividends paid increased modestly year-over-year to $20.6 million reflecting consistent payout policies aligned with cash flow confidence [F1][N6].

- Share repurchases accelerated meaningfully to approximately $118.5 million after lower buyback levels previously indicating active capital return strategies balanced against leverage post-acquisition financing [F1][S4].

Risks from Currency Volatility and Regulatory Compliance

Key risk factors include exposure to macroeconomic conditions tied closely with U.S.-based non-residential construction trends affecting both segments’ end markets [S5]. Operational challenges arise from tariff-driven cost increases, wage inflation notably within Mexican maquiladora manufacturing facilities (accounting for ~55% of finished goods production), and complex supply chains.

Currency translation risk is significant particularly via Mexican peso fluctuations impacting manufacturing costs against predominantly U.S.-dollar denominated sales; sensitivity analysis estimates a 10% peso depreciation could favorably impact operating profits by approximately $23 million while appreciation poses downside risks near $28 million; Canadian dollar effects are smaller but meaningful; European currency exposure is immaterial [S5].

Extensive regulatory compliance spans environmental statutes (e.g., Clean Air Act), privacy laws such as GDPR/CCPA influencing product data management practices; trade agreements including USMCA impacting cross-border operations; labor regulations especially concerning union contracts at Mexican facilities due for renegotiation within the next year—all contributing incremental compliance expenses currently not materially affecting profitability but warranting ongoing monitoring [S24][S25].

Legal contingencies including patent disputes or employment claims are managed through reserves without historical material financial impact [S24].

Outlook: Integration Execution and Platform Scaling Key to Sustained Growth

Future performance hinges on successful integration of QSC operations paired with scaling adoption of Atrius® cloud platform subscriptions driving recurring revenues within AIS—a promising trend amid growing smart space demand highlighted in recent earnings beats for Q2 FY26 reported April 2026 [N1][N4].[N10]

Close attention will be needed on managing cost pressures post-special charges alongside amortization ramp-ups related to acquisition intangibles that influence margin trajectories.

Potential expansion into new verticals remains strategic focus though no specific milestones have been disclosed yet—investors should monitor upcoming earnings commentary for updates on operational leverage improvements.[N14]

Raw material price volatility linked with tariff negotiations plus labor contract outcomes at Mexico facilities may affect near-term profitability.

This analysis is based exclusively on SEC filings ([F1], [S#]) supplemented by recent market reports ([N#]), adhering strictly to disclosed data without extrapolation beyond available sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments