Cartesian Growth Corp II Navigates Deadline Extensions Amid Liquidity Challenges

Cartesian Growth Corp II, a blank-check company, continues to pursue its initial business combination with looming liquidity constraints and extended regulatory deadlines.

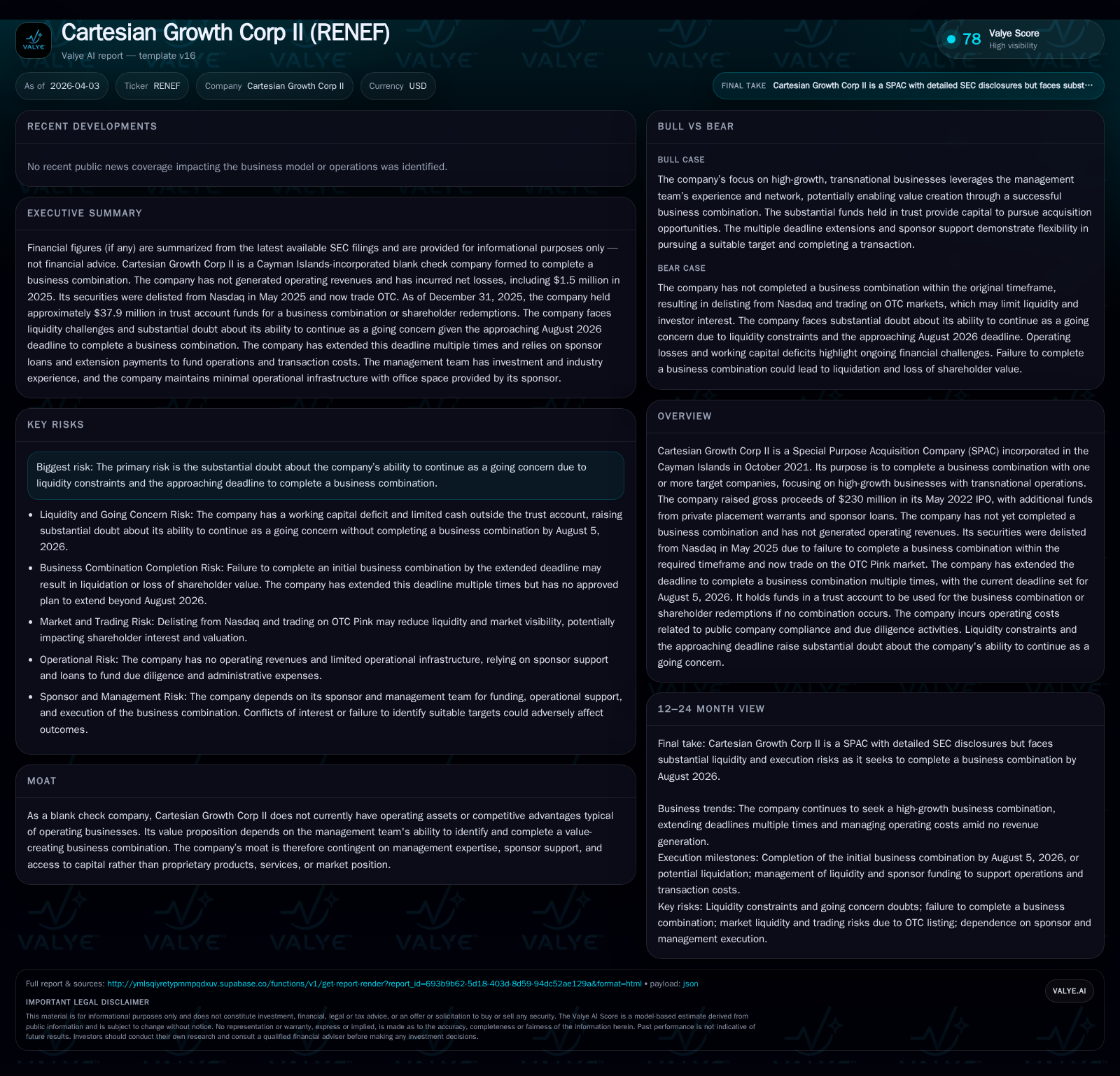

Cartesian Growth Corp II (RENEF) has yet to complete a business combination since its May 2022 IPO. Delisted from Nasdaq in May 2025 for failing to meet the transaction deadline, the company now trades on OTC Pink. Despite raising $230 million gross proceeds, trust account funds declined from $84.6 million at end-2024 to $37.9 million at end-2025 due to redemptions and sponsor notes. Operating losses persist, with net income turning negative in 2025 and working capital deficits exceeding $5 million. Sponsor loans via unsecured promissory notes provide additional runway but add complexity to capital structure. The current business combination deadline is extended to August 5, 2026, but going concern risks remain significant without transaction closure [S1][S3][S4][S6][S7][S10][S12][S17][S19][F1].

Company Overview and Historical Financial Performance

Cartesian Growth Corp II (RENEF) was incorporated on October 13, 2021 as a Cayman Islands exempted company structured as a Special Purpose Acquisition Company (SPAC). Its principal purpose is to effectuate an initial business combination with one or more target companies, focusing on high-growth entities with transnational operations or potential [S12].

The company completed its Initial Public Offering (IPO) on May 10, 2022, issuing 23 million units at $10 per unit including the full exercise of underwriters’ overallotment option, generating gross proceeds of $230 million [S1][F1]. Each unit comprises one Class A ordinary share and one-third of a warrant exercisable post-combination.

To date, Cartesian Growth Corp II has not commenced operations beyond fundraising activities and has no operating revenues. Financial results mainly reflect costs related to maintaining the blank-check entity structure, interest income generated on IPO proceeds held in trust accounts, fair value adjustments on convertible notes and warrants, and equity-related changes [F1][S12].

Key Financial Metrics (USD)

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -2 | -773847 | -1 | -118.4% |

| 2024 | 8 | -814232 | -1 | -28.3% |

| 2023 | 11 | -922735 | -2 | +132.1% |

| 2022 | 5 | -842878 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 51 | 5.7 |

| 2024 | 100 | -40.5 |

| 2023 | 77 | -61.7 |

| 2022 | -27.3 |

Source: SEC companyfacts cache [F1].

Operating losses improved year-over-year between FY23-FY25 by about 10%, while net income turned sharply negative in FY25 largely due to changes in warrant liabilities and operational expenses [F1].

Cash Position and Trust Account Developments

At the IPO close in mid-2022, Cartesian Growth Corp II placed approximately $236.9 million into a trust account invested primarily in U.S. Treasury securities or money market funds adhering to regulatory maturity limits [S1]. The trust account balance decreased significantly from approximately $84.6 million at December 31, 2024 to roughly $37.9 million at December 31, 2025 due predominantly to substantial redemptions following deadline extensions and share repurchases alongside deferred underwriting fees remaining constant at $11.5 million [S17][S20][F1].

Cash held outside the trust account—available for transaction-related expenses such as due diligence—was limited to about $163K as of fiscal year-end 2025 [F1][S20]. Operating costs persisted around $930K annually including office lease fees paid monthly ($10K) to an affiliate of the sponsor plus administrative expenses and amortization of offering costs [F1][S6].

Sponsor financing includes unsecured promissory notes totaling roughly $4.2 million issued between late 2023 and late 2025 bearing no interest that mature upon consummation of the initial business combination or winding up of the company. These notes are convertible into warrants exercisable at $1 each at sponsor discretion adding complexity to capital structure [S7][S14][S15].

Business Combination Deadlines and Regulatory Status

The company was originally required to complete an initial business combination within approximately three years from IPO registration effectiveness (May 5, 2025). Failure to meet this milestone resulted in Nasdaq delisting effective May 13, 2025; securities now trade over-the-counter on OTC Pink under tickers RENEF (units), REEUF (Class A shares), and REEWF (warrants) [S1][S12].

To extend operational flexibility beyond delisting—and maintain shareholder confidence—the board approved multiple monthly deadline extensions through November 2025 with corresponding sponsor deposits into the trust account via promissory notes totaling several million dollars. The current extended deadline is August 5, 2026 providing additional time but also increasing obligations under these notes which remain contingent on successful transaction completion [S19][S23].

Operational Expenses and Going Concern Considerations

Operating expenses include ongoing monthly fees for office space provided by an affiliate of the sponsor ($10K/month plus utilities) commencing post-IPO closure in May 2022 along with administrative and legal costs associated with pursuing transactions [F1][S6].

By December 31, 2025 accumulated working capital deficit exceeded $5 million against very limited cash reserves outside the trust account prompting management's recognition of substantial doubt regarding ability to continue as a going concern absent successful completion of an initial business combination before the extended deadline expiry [F1][S19].

Sponsor obligations remain limited under indemnification provisions tied primarily to protecting trust account funds supporting investor redemptions; no borrowings have occurred under working capital loans aside from formalized promissory notes described above [S25].

Capital Structure and Shareholder Composition

As of December 31, 2025:

- Approximately 8.8 million Class A ordinary shares were issued with about 3.1 million shares subject to possible redemption valued near $37.9 million computed using redemption prices around $12.33 per share reflecting escrowed funds pending liquidation or business combination outcomes [F1][S20].

- Sponsor holds Class B ordinary shares convertible one-for-one into Class A shares; two Class B shares outstanding represent nominal positions [S11].

- Warrants outstanding include public warrants exercisable post-combination at $11.50 per share plus private placement warrants linked with sponsor loans adding dilution risk if converted [S16][S27].

- Shareholders’ deficit stood near negative $26.3 million reflecting accumulated losses and redemption liabilities carrying implications for residual equity value post-redemption or liquidation events [F1][S20].

No dividends have been declared nor are expected prior to consummation of any business combination consistent with typical SPAC structures given lack of operating profits so far [S10].

Outlook: Opportunities Amid Constraints

Prospects rely exclusively on consummating an initial business combination involving high-growth targets with international operations—a strategic focus established at inception [S12]. Key factors influencing success include:

- Identifying suitable target companies within tightening timelines ahead of August 5th deadline;

- Maintaining sufficient capital resources balancing dwindling trust funds against sponsor financing commitments;

- Managing regulatory scrutiny following Nasdaq delisting impacting investor sentiment;

- Navigating market conditions affecting valuation multiples and financing availability;

- Controlling shareholder redemptions that reduce available cash for deal execution;

- Leveraging management’s expertise and sponsor network for deal sourcing.

Failure to complete a business combination by the current deadline or secure further extensions would likely precipitate liquidation proceedings returning remaining trust funds pro-rata less accrued liabilities—with warrant holders potentially facing total loss.

In summary: Cartesian Growth Corp II exemplifies challenges confronting SPACs amid evolving market dynamics including delayed deal execution cadence compounded by redemption-driven capital erosion plus regulatory setbacks impacting trading liquidity and solvency considerations. While management experience may mitigate some transactional risks ahead, the absence of visible acquisition milestones heightens uncertainty over near-term viability without transformational developments.

This analysis is based exclusively on publicly available filings as of early April 2026 and does not constitute investment advice or recommendations regarding Cartesian Growth Corp II or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments