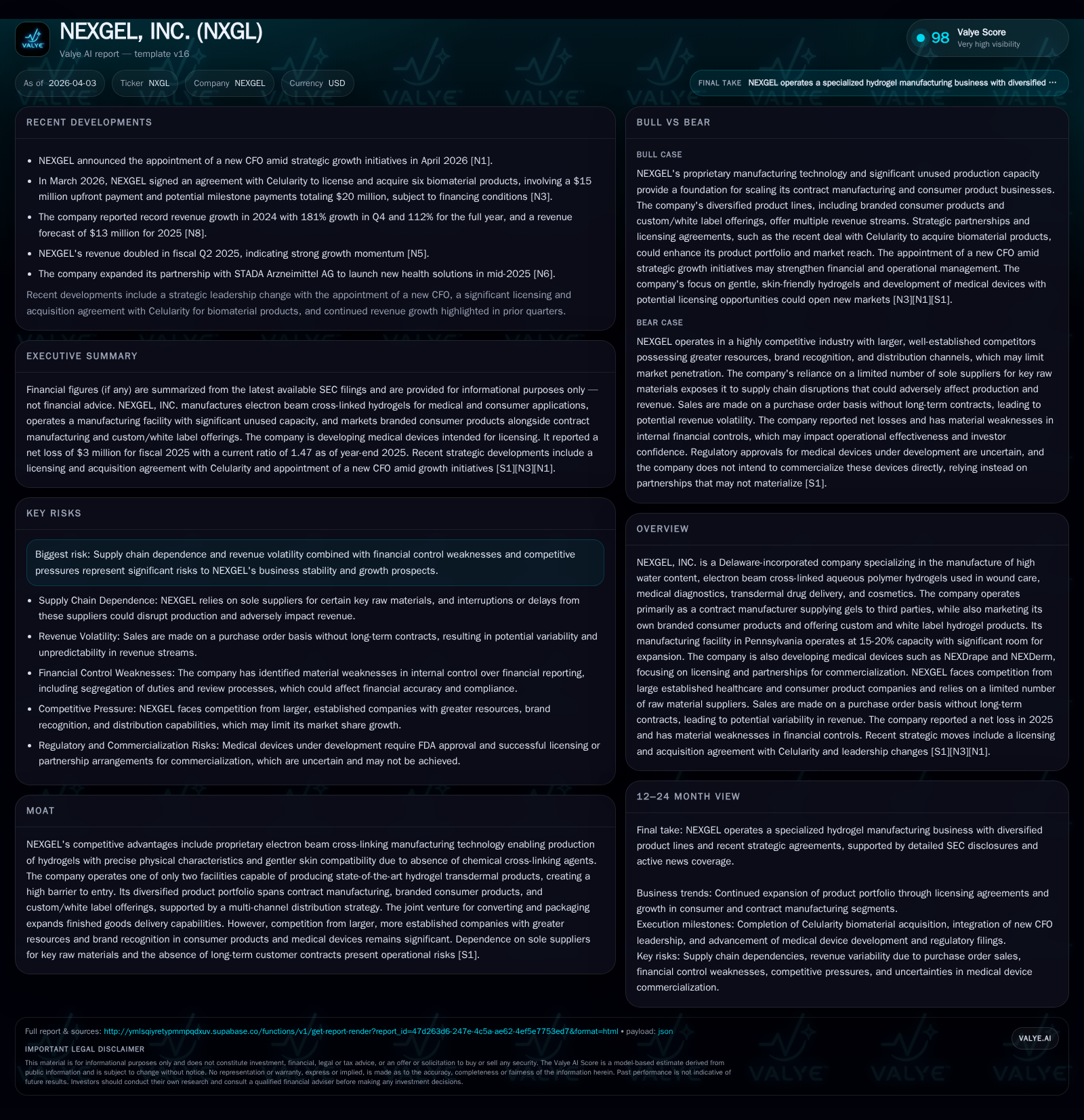

NEXGEL’s Proprietary Hydrogels: Balancing Innovation and Financial Hurdles

NEXGEL leverages its unique electron beam technology in hydrogels while navigating capacity underuse, supply constraints, and persistent losses.

NEXGEL, Inc. operates a rare electron beam cross-linking hydrogel manufacturing platform serving wound care, diagnostics, transdermal drug delivery, and cosmetics. The company’s proprietary method enables precise customization and gentle skin compatibility, positioning it among only two global producers of advanced hydrogel transdermal products. Despite technological leadership and expansion into medical device licensing and custom consumer products, NXGL faces challenges from heavy reliance on sole raw material suppliers, underutilized plant capacity (~15-20%), and ongoing operating losses. Historical financials reveal steady operating deficits with improving cash flow trends yet negative free cash flow. Strategic initiatives include biomaterial acquisitions and new CFO appointment aiming to strengthen commercialization and capital discipline. Competitive pressure from established healthcare giants combined with immature sales capabilities constrain scale gains. Key risks center on supply chain concentration, regulatory compliance, and financial control weaknesses. Upcoming milestones to watch include commercialization progress of licensed biomaterials and medical devices along with manufacturing scale-up efforts.

Innovation Roots: Proprietary Technology Driving Hydrogel Performance

NEXGEL’s core technological advantage lies in its proprietary electron beam cross-linking manufacturing process for aqueous polymer hydrogels. Unlike conventional chemically cross-linked hydrogels, this electron beam technique avoids residual chemical agents that might irritate skin, thus enhancing biocompatibility—a critical attribute in wound care, transdermal drug delivery, diagnostics, and cosmetic applications [S1][S18]. This method allows stringent control over a spectrum of physical parameters including thickness tolerance, water content uniformity, adherence properties, absorption rates, moisture vapor transmission rate (MVTR), and active ingredient release kinetics.

The company's ability to customize liners onto which these gels are coated provides clients flexibility in modulating MVTR and dosing profiles—a sector-specific capability reflecting advanced manufacturing sophistication valuable in precision transdermal therapies [S1]. Manufacturing capacity is concentrated at a Pennsylvania site that is notably one of merely two facilities worldwide equipped for such state-of-the-art hydrogel production technology—a high barrier-to-entry moat supporting competitive differentiation [S1][S26].

Historical Financial Trends: Persistent Losses and Operating Dynamics

Across fiscal years 2022 through 2025, NEXGEL has consistently operated at an operating loss that has shown slight improvement recently. Operating income moved from -$3.35 million in FY22 to -$3.48 million in FY23 before improving to -$3.55 million in FY24 and narrowing further to -$3.35 million in FY25 (approximately +5.7% YoY improvement last year) [F1]. Net income followed a similar trend with losses reducing from -$4.75 million in FY22 to -$3 million in FY25 (+8.6% YoY).

Operating cash flows have improved markedly—from negative $3 million in FY22 to approximately negative $1.31 million in FY25—indicating better working capital management or less onerous operational cash burn [F1]. Capital expenditures declined sharply by nearly 85% over these years from $696K peak expenditure in FY23 down to $68K most recently as the firm prioritizes cost containment amid growth constraints.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -3 | -1 | -3 | 68000 | +8.6% |

| 2024 | -3 | -4 | -4 | 443000 | -3.9% |

| 2023 | -3 | -3 | -3 | 696000 | +33.5% |

| 2022 | -5 | -3 | -3 | 96000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -1 | -67.3 |

| 2024 | -4 | -57.0 |

| 2023 | -4 | -67.2 |

| 2022 | -3 | -62.1 |

Source: SEC companyfacts cache [F1].

Return on equity remains negative at an estimated -67%, reflecting cumulative losses relative to shareholder equity of approximately $4.46 million as of FY25 [F1]. These trends highlight ongoing challenges scaling operations profitably while managing investments prudently.

Manufacturing Capacity and Supply Chain Dependencies Impacting Growth

NXGL operates its sole manufacturing facility at roughly 15-20% capacity utilization rate offering significant potential room for volume growth without major incremental fixed costs [S1]. However this underuse also signals current demand or operational execution limitations constraining ramp-up to more economically scalable throughput levels.

Adding complexity is the company’s reliance on single-source suppliers for core polymers—Dow Chemical provides polyethylene oxide while BASF supplies polyvinylpyrrolidone—the foundational components of their hydrogel formulations [S7][S15]. Such supplier concentration poses tangible risks: any disruption could delay production materially given difficulties swiftly qualifying alternative sources given strict quality standards required for medical-grade hydrogels.

Inventory management challenges coupled with purchase-order-based sales devoid of minimum commitment contracts exacerbate revenue volatility risks inherent to fluctuating demand cycles within regulated medical materials supply chains [S7][S21]. Reinforcing supply diversification strategies alongside sophisticated inventory forecasting is essential for operational resilience.

Strategic Growth Initiatives: Medical Devices and Licensing Agreements

A pivotal strategic thrust has been NXGL’s agreement with Celularity to license and acquire six biomaterial product lines broadening its portfolio beyond hydrogels alone—in particular advancing into medical devices aimed at reducing skin pain and irritation such as NEXDrape and NEXDerm [N2][N1][S1][S5]. These devices align with company expertise around skin integrity but require successful commercialization via partnerships given NXGL’s limited internal sales infrastructure.

While contract manufacturing remains core revenue driver supplying gels globally used for drug delivery (e.g., hormone therapy patches) plus OTC therapeutic applications (e.g., pain relief creams), segmentation into own-branded consumer products along with custom white label offerings creates diversified revenue streams albeit early-stage given competitive pressures identified elsewhere [S28]. The joint venture formed with CG Laboratories strengthens packaging capabilities enhancing finished goods market readiness.

Capital Allocation and Financial Health: Returns, Cash Flows, and Liquidity

Given ongoing operating losses yet improving cash flow dynamics recounted previously [F1], NXGL has prioritized capital preservation evidenced by plunging capex spend from $696K (FY23) down to just $68K latest year—reducing investment intensity while calibrating growth pace carefully amid continued losses.

Recent personnel changes include appointing a new CFO signaling intent to bolster financial controls amidst historical material weaknesses cited related to segregation of duties within accounting processes that could impair financial reporting reliability if unremediated [N1][S14]. Current ratio stands at approximately 1.47 indicating moderate liquidity sufficiency but no excess cushion against shocks ([F1]).

No dividends or share buybacks are reported reflecting reinvestment priorities typical for emerging companies focused on scaling.

Competitive Pressures and Market Position in Medical and Consumer Segments

Despite the unique proprietary technology moat rooted in electron beam cross-linking capability foundational to its contract manufacturing segment (one of just two global providers), NXGL faces substantial competition pressing on margins especially outside contract manufacture where larger healthcare conglomerates dominate distribution channels and brand recognition levels [S18][S26].

Consumer product lines leverage multi-channel sales platforms including Amazon and Shopify but remain contingent on maintaining these channel relationships which carry inherent risks of delisting or unfavorable terms if violated or disrupted [S21]. Limited direct sales force hinders swift geographic scaling thereby placing premium on forging strategic marketing partnerships particularly within nascent medical device verticals [S6].

Strategic Risks: Intellectual Property Protection & Regulatory Environment

NXGL maintains multiple IP protections including trademarks across product lines with patent filings for devices such as NEXDrape under the Patent Cooperation Treaty securing broad jurisdictional coverage—a tactical defense supporting commercialization prospects despite early stage device maturity [S5][S6][S7]. Additional licensed patents cover transdermal patch technologies but are non-core given impending expiry dates without significant impact forecasted on current business lines [S17].

Supply risk centers acutely around sole source vendor dependence notably Dow Chemical and BASF polymer supplies where sudden shortages or price shifts could cause costly disruptions given limited short-term alternatives suitable for clinical use demands; mitigating inventory buffers reduce vulnerability only partially [S15].

Regulatory compliance burden spans FDA cGMP requirements enforced via periodic inspections; most hydrogels qualify as Class I exempt devices limiting pre-market submission needs yet medical devices face more rigorous scrutiny imposing continuous compliance investments increasing overhead risk profile [S16][S18]. Healthcare fraud statutes amplify legal exposure dimensions requiring management vigilance amidst evolving enforcement trends [S8].

Material weaknesses detected around financial controls introduce operational risk vectors impacting investor confidence until remediated per disclosed corrective plans underway [S14].

What to Watch: Commercialization Progress & Operational Scaling Milestones

Investor attention should focus on:

- Progress commercializing recently licensed biomaterial portfolios acquired via Celularity including integration success signals or regulatory hurdles impacting launch timelines ([N2],[N1],[S1]).

- Development trajectory and market reception of novel medical devices NEXDrape/NEXDerm given dependence on third-party commercialization allies requiring partnership execution competence ([N1],[N2],[S5]).

- Efforts addressing underutilized manufacturing plant capacity potentially signaling improved demand visibility or efficiency gains providing pathway toward scalable margin improvements ([S1]).

- Resolution status regarding internal control remediation affecting financial statement reliability disclosures potentially influencing market perceptions ([S14]).

- Supply chain diversification initiatives reducing dependence on Dow Chemical/BASF polymers vital for operational continuity ([S7],[S15]).

Overall NXGL navigates a complex juncture balancing differentiated hydrogel technology leadership against operational scaling challenges compounded by financial constraints typical for emerging biomanufacturing entities striving toward sustainable commercial traction.

This analysis solely aims to provide a detailed examination of NEXGEL’s current business environment based on publicly available filings and news reports up to early April 2026; it does not constitute investment advice or an endorsement of the company’s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments