DynaResource's Breakthrough Year: From Losses to Production Profitability

The company shifted to profitable production in 2025 despite liquidity pressures, leveraging its Mexican gold-silver concentrate assets.

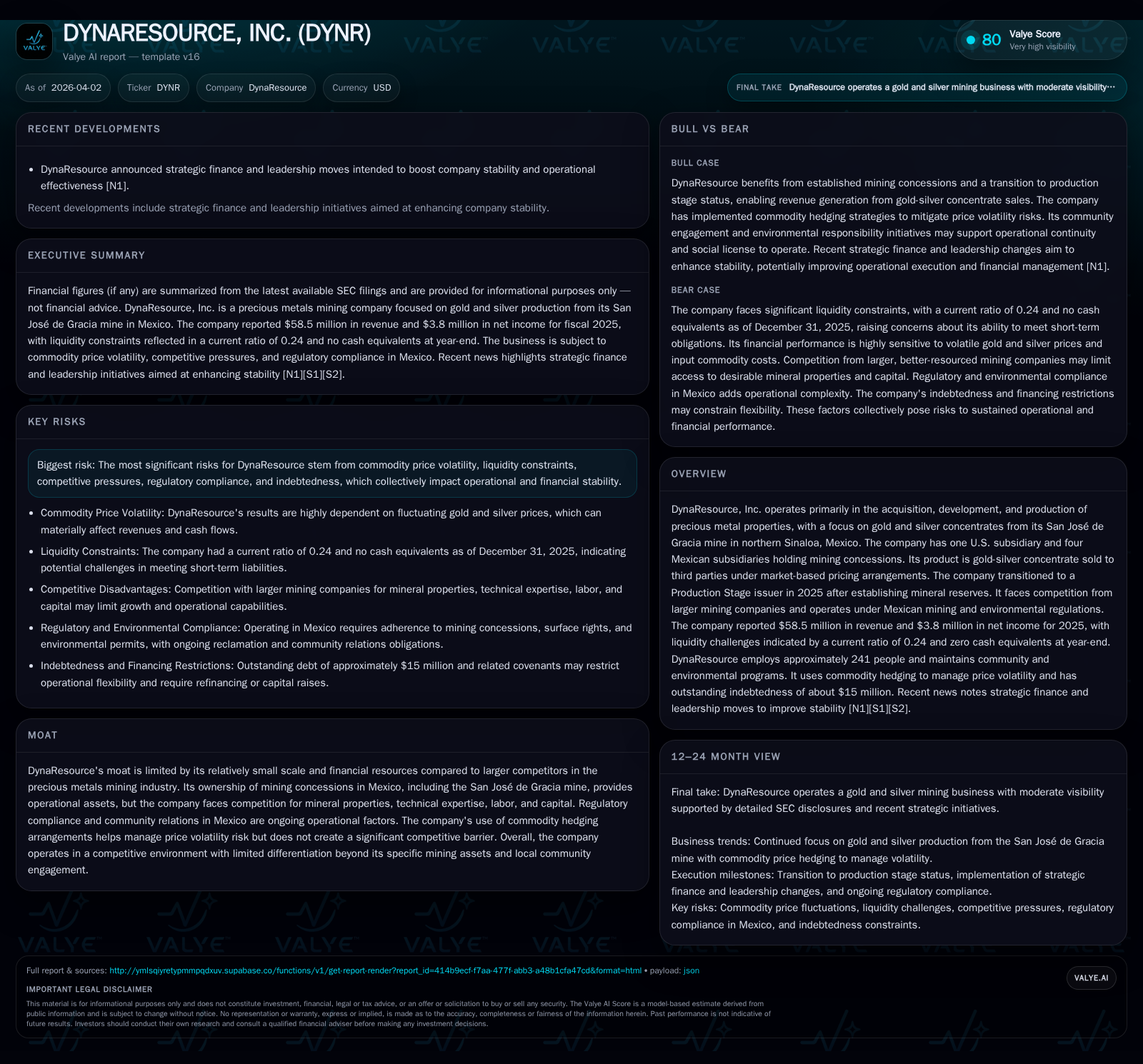

DynaResource, Inc. ended a prolonged period of losses with a transition to a Production Stage issuer in 2025, reporting $58.5 million in revenue and $3.8 million net income supported by the San José de Gracia mine operations in northern Sinaloa, Mexico. While operational footholds expanded, the company faces significant liquidity constraints with a current ratio of 0.24 and zero cash equivalents at year-end. Commodity price volatility and regulatory complexities remain critical risk factors as DynaResource continues capital-intensive mining activities with limited scale against larger competitors.

Historical Growth Trajectory and Profitability Shift

DynaResource’s financials reflect a pronounced turnaround culminating in fiscal year (FY) 2025. After enduring multi-year operating losses—highlighted by an operating income loss exceeding $15 million in FY2023—the company swung to a positive operating income of approximately $9.67 million in FY2025 [F1]. Revenue increased by 25.7% year-over-year (YoY), reaching $58.5 million for that year, driven primarily by commencement of production stage operations at its principal asset. Net income also swung from an $8.13 million loss in FY2024 to a $3.82 million profit in FY2025 [F1]. Operating cash flow similarly rebounded spectacularly from negative $8 million to positive $5.76 million, indicating improved operational cash generation [F1]. This recovery evidences the successful operationalization following the declaration of mineral reserves under SEC Regulation S-K Item 1300 effective January 1, 2025 [S1][S18].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 58 | 4 | 6 | 10 | +25.7% | +146.9% |

| 2024 | 47 | -8 | -8 | -7 | +30.7% | +44.0% |

| 2023 | 36 | -15 | -18 | -15 | -10.5% | -317.4% |

| 2022 | 40 | 7 | -2 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 3 | -348.6 |

| 2024 | -8 | -241.0 |

| 2023 | -18 | -380.9 |

| 2022 | 50.7 |

Source: SEC companyfacts cache [F1].

This table underscores how the company’s transition to recognized mineral reserves immediately transformed revenue quality and profitability metrics.

Operational Focus: San José de Gracia Mine and Product Strategy

DynaResource's flagship asset is the San José de Gracia (SJG) mine located in northern Sinaloa State within Mexico [S1]. The Company operates through four Mexican subsidiaries holding mining concessions and one U.S.-based holding entity involved mainly for compliance with Mexican corporate ownership laws [S1].

The SJG mine produces gold-silver concentrate—a finely ground mix where gangue material is separated to enrich precious metals concentration [S1]. This product type requires downstream third-party processing; thus DynaResource sells its concentrate output under contract arrangements reflecting spot market prices adjusted for 'payability'—a typical industry term denoting discounts applied based on recoverable metal content relative to assay results [S1]. Approximately twenty thousand ounces of contained gold were delivered as concentrate during the production year [S1], positioning this single-mine operation as the central revenue driver.

The exclusive focus on concentrate rather than refined metals means DynaResource’s earnings are directly exposed not only to fluctuating metal prices but also treatment charges and market demand dynamics intrinsic to concentrate markets.

Metal Price Exposure and Hedging Practices

Given all revenue emanates from selling precious metal concentrates containing gold and silver subject to spot pricing volatility [S1], DynaResource’s financial performance is heavily influenced by fluctuating commodity prices and refining costs [S1][S9]. Prices for gold oscillated drastically throughout recent years including an extraordinary spike over +100% since early 2024 [S1], affecting revenue realization.

To mitigate this price risk exposure on approximately three-quarters (~75%) of anticipated production—or around nine thousand ounces—DynaResource entered into commodity pricing arrangements effective September 2024 with fixed-price hedges set at $2,495 per ounce under their Offtake Agreement [S1]. This structured protection limits downside pricing volatility on major volume commitments but conversely caps potential upside gains during bullish price movements [S1]. Such contract mechanisms are commonly employed among mid-tier producers lacking extensive balance sheet cushion or downstream refining capabilities.

Current Liquidity Position and Capital Structure Challenges

Despite operational profit emergence in FY2025 reflecting commercial production success [F1], liquidity indicators signal marked constraints threatening near-term financial flexibility. The company ended December 31, 2025 with zero cash equivalents amid total current assets slightly above $10 million against current liabilities exceeding $41 million resulting in a severely depressed current ratio near 0.24 [F1].

Debt obligations remain material; long-term indebtedness approximates $15 million as of year-end [S7], with significant negative covenants embedded restricting financial maneuvering [S7][S22]. The company expresses concerns over its ability to meet scheduled payments without sufficient cash flow enhancements or refinancing alternatives [S7][S22]. These factors have triggered accounting disclosures highlighting substantial doubt regarding going concern status by auditors reflecting elevated business risk linked chiefly to working capital deficits and leverage configurations [S16][S18].

Trade payables and accrued expenses similarly rose markedly supporting operational scale-up but feeding into tight working capital cycles necessitating vigilant cash management [F1][S24].

Investment in Capex and Its Role in Sustaining Operations

Capital expenditures surged dramatically in the production transition year—rising almost forty-fold from nominal prior years’ levels totaling approximately $2.61 million for FY2025 compared to just several thousand dollars previously [F1][S23].

This capex intensity reflects heavy investment prioritizing plant construction completion phases plus mine development aimed at unlocking proven reserves essential for ongoing output sustainability given the relatively short mine life spans typical for such deposits (i.e., reserve conversion-driven development spending) [S23]. Operating leverage through higher fixed asset bases is characteristic of mining endeavors entering production stages after exploration-heavy phases.

While this scale-up capex exacerbates cash burn short-term amid low liquidity buffers described above—longer-term it underscores commitment to supporting continuous ore extraction volumes necessary for revenue consistency.

Regulatory Compliance and Legal Standing of Mining Concessions

DynaResource operates under Mexican mining laws requiring that its portfolio of mineral concessions—including SJG’s nine main claims—be maintained diligently through biannual duties payments plus annual filings certifying exploration or exploitation activity status ensuring ‘good standing’ classification crucial for legal protection against claim forfeiture or competing contestations [S1][S9].

Although the company asserts compliance with surface rights obligations along with environmental labor regulatory frameworks as required under evolving Mexican mining statutes including amendments effective since December 2006 consolidating concession categories into renewable fifty-year terms [S1][S9], it faces active legal proceedings probing ownership validity over some concessions which could potentially impact future operations if adverse outcomes materialize [S9][S10].

Environmental considerations weigh heavily on cost structure due to requirements for remediation measures and potential litigation exposure inherent in jurisdictions with heightened enforcement focus postulated under both domestic Mexican regulations and international compliance standards frequently monitored by investors emphasizing ESG risks within extractive industries [S17].

Community Relations and Competitive Environment

Though comparably modest in scale relative to multinational miners controlling vast international portfolios enabled by substantial capital reserves and demonstrated technical expertise pools [S12], DynaResource leverages localized community engagement initiatives helping maintain social license necessary for uninterrupted access to land and workforce continuity around SJG operations [S1].

However competitive pressures remain intense: barriers include scarce availability of attractive mineral lands due to acquisition activity by larger rivals constraining organic growth options alongside challenges sourcing skilled labor competitively due to limited resources available among smaller producers operating outside major hubs noted elsewhere within Mexico’s silver belt regions known historically for high-grade deposits yet correspondingly high competition for talent owning requisite underground mining competencies typical of precious metals extraction cycles [S12].

Capital procurement also competes against entrenched players able to finance extensive exploration/development pipelines while negotiating preferred terms across finance markets restricting DYNR’s leverage rates potentially raising cost of capital or limiting financing access particularly when coupled with liquidity weakness evident in financial statements discussed earlier.

Forward-Looking Elements: What to Monitor Next

Without explicit forward guidance disclosed as of April 2026 filings [N/A], close attention should be paid to several critical performance indicators impacting future valuations:

- Trends in gold-silver market prices vis-à-vis extent of hedge coverage protecting realized sales prices;

- Liquidity trajectory including any equity or debt raises successfully executed alleviating working capital stress or extending maturities;

- Progress resolving legal uncertainties around concession claims which pose existential material risk if decided unfavorably;

- Efficiency of capex deployment converting invested capital into sustained or growing output volumes beyond initial production ramp phase;

- Effects of evolving regulatory environment particularly environmental compliance costs that could direct capital allocation priorities or curtail mine life economics;

- Broader macroeconomic factors such as inflationary pressures impacting input commodity costs (fuel/electricity/explosives) adding upward margin pressure;

- Credit covenant compliance given non-trivial debt profile potentially triggering accelerated repayment scenarios or restrictive covenant waivers.

Stakeholders should monitor quarterly updates closely for refinement on these elements since operating leverage remains high amidst constrained financial flexibility magnifying operational risks associated with volatile metal prices common across junior precious metals miners.

This analysis synthesizes SEC-filed financial data up through FY2025 alongside regulatory disclosures describing DynaResource’s operational pivot toward profitable mining production amid pronounced financing challenges and competitive sector dynamics inherent within Mexico’s precious metals industry space. It aims solely at elucidating historical trends and forward operating context without conveying investment recommendations or valuation judgments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments