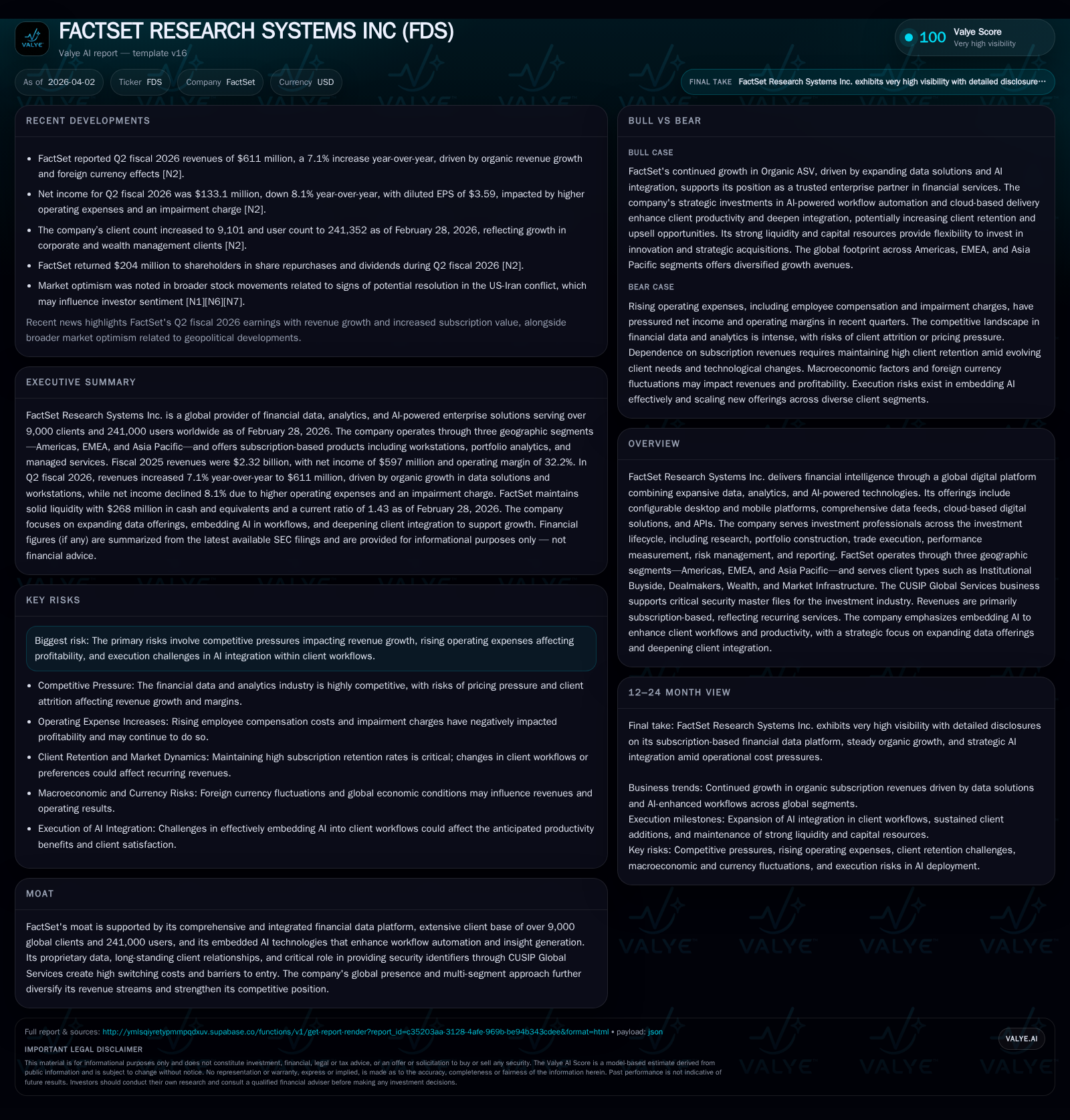

FactSet Advances AI-Empowered Financial Intelligence Amid Rising Operating Costs

FactSet Research Systems delivers steady subscription revenue growth driven by AI integration and global client expansion but faces margin pressures from rising expenses.

FactSet Research Systems Inc. has exhibited consistent revenue and income growth over recent years, fueled notably by subscription-based data and analytics platforms enhanced with embedded AI technology. Its diversified global presence across Americas, EMEA, and Asia Pacific segments supports recurring revenues from over 9,000 clients and more than 240,000 users. Despite beating quarterly estimates and raising FY26 outlook, increased employee compensation costs and a non-cash asset impairment weighed on operating margins and net income in Q2 2026. Strong cash flow generation underpins robust capital returns through dividends and share repurchases, supported by a disciplined capital structure with manageable debt maturities.

Historical Performance

SEC companyfacts cache Research Systems has demonstrated consistent top-line expansion over recent years, driven primarily by subscription services across its hosted platform encompassing workstations, portfolio analytics, enterprise solutions, and comprehensive data feeds. Fiscal year 2025 closed with total revenues of approximately $2.32 billion, representing a growth rate of 5.4% from the prior year [F1][S1]. This growth arose from a combination of organic increases (4.4%), acquisition contributions (0.9%), and favorable currency fluctuations (0.1%). The company's expansive platform services a diversified global clientele exceeding 9,000 entities comprising institutional buyside firms, dealmakers, wealth managers, market infrastructure participants, and corporate investment professionals [S1].

Operating income for FY25 stood at roughly $748 million, marking an increase of about 6.7% year-over-year despite rising costs [F1]. Net income improved by approximately 11.2%, reaching about $597 million for the same period [F1]. This performance reflects scale efficiencies balanced against salary inflation and investments in technology enhancement.

Cash flows from operations delivered strong free cash generation of nearly $665 million (operating cash flow of ~$726 million less capex around $61 million), providing robust liquidity to fund strategic initiatives including acquisitions and shareholder remuneration [F1][S15].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 597 | 726 | 748 | +11.2% | |

| 2024 | 537 | 700 | 701 | +14.7% | |

| 2023 | 468 | 646 | 629 | 61 | +18.0% |

| 2022 | 397 | 538 | 475 | 51 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 160 | 300 | |

| 2024 | 151 | 235 | |

| 2023 | 139 | 177 | 585 |

| 2022 | 126 | 19 | 487 |

Source: SEC companyfacts cache [F1].

Note: Capex reflects capitalized internal-use software plus physical assets.

Geographic Segmentation

The Americas segment dominates SEC companyfacts cache's revenue composition with approximately $1.51 billion generated in FY25, supported by corporate headquarters operations including significant data center functions and third-party data costs centralized there [S19][S20]. EMEA contributed around $580 million while Asia Pacific accounted for approximately $235 million during that year.

Each region showed organic ASV growth powered by strong demand for workstation products as well as data solutions; Asia Pacific posted an above-average organic ASV increase near double digits relative to other regions in recent quarterly disclosures [S2].

Recent Quarterly Results & Outlook

In Q2 FY26 ended February 28, SEC companyfacts cache reported revenues surpassing analyst expectations fueled primarily by core workstations and data solution offerings that continue to win new clients and deepen engagements within existing accounts [N1][N3][S2]. Organic ASV—a forward-looking metric reflecting contracted annual recurring revenue—rose sharply by approximately 6.7% year-over-year to $2.45 billion across all regions with fastest gains in Americas and Asia Pacific [S2]. Total clients increased modestly to over 9,100 while total user count climbed over 10% year-over-year driven largely by wealth management segments.

Despite this top-line strength, operating margin shrank to about 30%, down from prior year’s mid-30s level due largely to wage inflation amidst competitive talent markets plus one-time impairment expense recorded under Other assets category referenced in the latest quarter’s filings [N11][S2]. Net income declined approximately eight percent sequentially but earnings per share decreased only about four percent given share repurchase activity reducing diluted weighted average shares outstanding.

SEC companyfacts cache also upgraded its full-year fiscal 2026 outlook citing confidence in underlying recurring revenue momentum coupled with steady uptake of AI-enhanced capabilities embedded throughout its platform suite aimed at automating manual analysis tasks while amplifying analytical precision for clients globally [N10].

Innovation & AI Integration

A key component sustaining SEC companyfacts cache's competitive moat is its aggressive embedding of artificial intelligence technologies directly into its financial intelligence platform ecosystem . These capabilities improve workflow automation enabling clients to accelerate research cycles and elevate signal extraction quality — important differentiators as complex asset management increasingly relies on machine learning at scale.

Moreover, SEC companyfacts cache’s continued investment into modular cloud-based solutions along with API accessibility positions it well to appeal to a broader set of investment professionals seeking customizable integrations versus legacy monolithic software offerings common among certain competitors.

Capital Structure & Returns

SEC companyfacts cache maintains a conservative balance sheet marked by strong cash reserves nearing $268 million as of February end combined with manageable long-term unsecured debt totaling approximately $375 million drawn under credit facilities maturing between April of 2028-2030 [F1][S5][S8]. The company's weighted cost of debt is relatively low given floating rate exposure hedged through interest rate swaps executed recently aiming at mitigating SOFR volatility risk [S16][S17].

In terms of capital return strategy, SEC companyfacts cache has demonstrated a commitment to balancing growth investments with shareholder value via consistent dividend payments alongside sizable share repurchase programs totaling hundreds of millions annually — including an authorized repurchase capacity upward of $700 million still available as of early calendar year ’26 [F1][S15][S18].

Risks & Challenges

Notwithstanding solid fundamentals and strategic positioning within financial intelligence technology provision sectors, SEC companyfacts cache faces several operational challenges:

- Competitive Pressure: Increasing rivalry within the financial data analytics marketplace could constrain pricing power especially as new entrants pursue scalable cloud-native alternatives challenging incumbent desktop-centric platforms.

- Cost Pressures: Upward pressure on employee compensation reflecting talent scarcity in technical roles is compressing operating margins despite top-line growth.

- AI Execution Risks: While AI adoption may unlock differentiation advantages if executed effectively, any delays or failure integrating these tools fluidly into client workflows could undermine expected productivity benefits or cause churn among sophisticated users. These factors warrant close monitoring in future earnings cycles given their potential impact on sustainable profitability metrics.

Conclusion & What To Watch

SEC companyfacts cache Research Systems remains a leading provider delivering integrated financial intelligence solutions anchored on subscription models emphasizing recurring revenue stability paired with expanding AI-driven functionality enhancements across global markets. Key upcoming milestones include:

- Trajectory of Organic ASV Growth underpinning revenue momentum amid evolving client workflows adopting AI-enabled solutions.

- Operating Margin Trends reflecting balancing acts between investment in innovation/talent versus cost discipline.

- Client/User Expansion Dynamics especially penetration into emerging markets within Asia Pacific where digital transformation accelerates demand for sophisticated analytics products.

- Progress on Share Repurchase Plans indicating confidence regarding capital allocation priorities amid ongoing macroeconomic uncertainties. One should also carefully track technological rollout success rates alongside competitor developments reshaping the financial data industry landscape.

Disclaimer: This analysis is based solely on publicly available information as indicated; it is intended for informational purposes without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments