Andina Bottling Co. Advances Regional Scale with Steady Earnings and Strategic Capital Use

Strong brand association and regional diversification underpin Andina’s 2025 financial results and operational positioning.

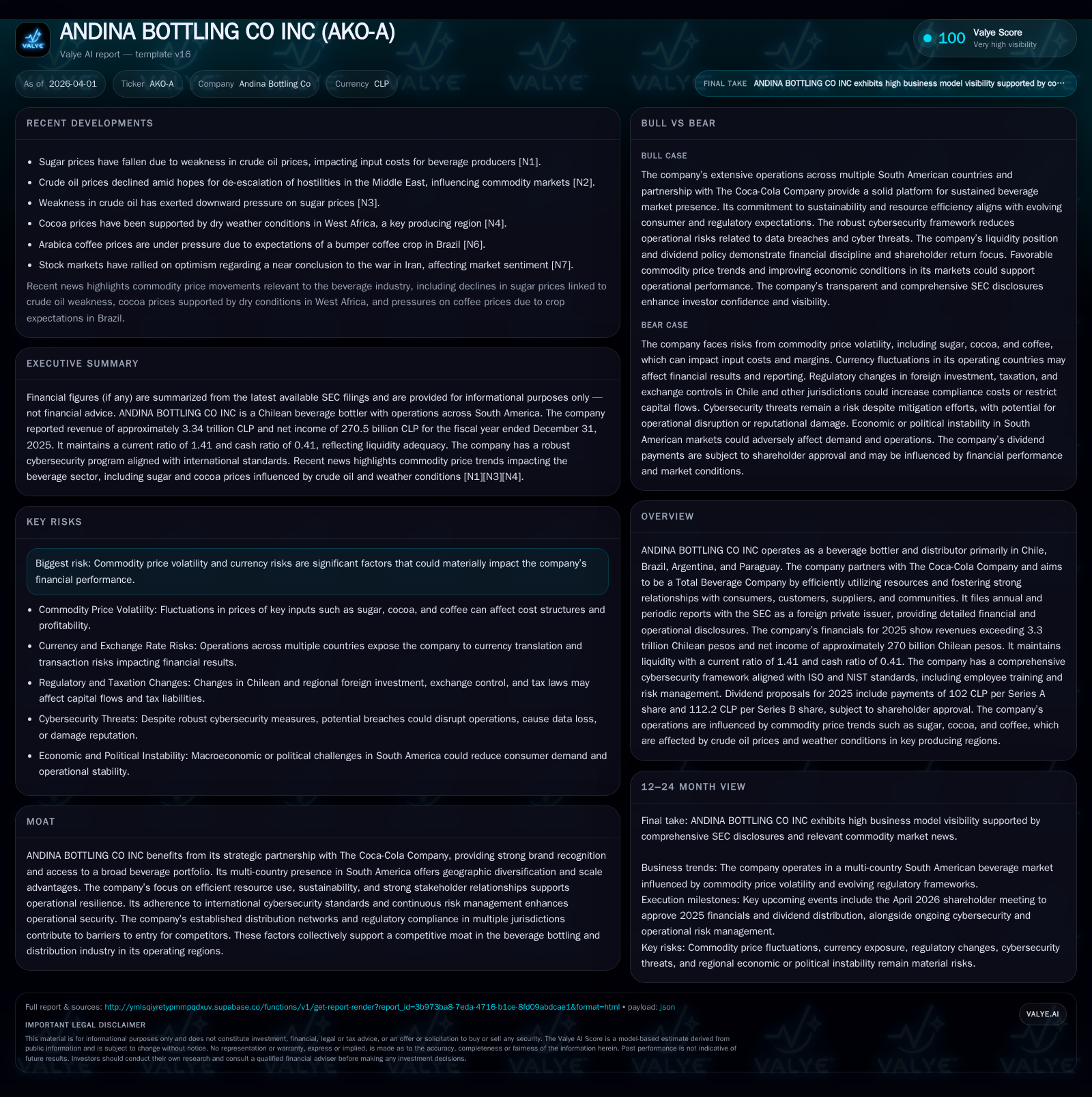

Andina Bottling Co Inc, operating across key South American markets with partnership ties to The Coca-Cola Company, reported solid revenue growth of 3.7% in 2025 to over 3.34 trillion CLP, driven by expanded sales volumes and pricing initiatives. Net income rose 15.3% year-over-year to approximately 270 billion CLP, reflecting operational efficiencies amid inflationary pressures. The company’s balance sheet shows disciplined liquidity management with a current ratio of 1.41, and it sustained shareholder returns through dividends albeit at a reduced level from the prior year. Its multi-country presence combined with strong distribution and compliance frameworks supports a defensible competitive moat; however, exposure to currency fluctuations and commodity cost volatility poses ongoing risks.

Company Overview and Market Footprint

ANDINA BOTTLING CO INC (ticker: AKO-A), known also as Embotelladora Andina S.A., operates as a primary beverage bottler and distributor in South America, notably across Chile, Brazil, Argentina, and Paraguay [S1]. The company maintains a strategic alliance with The Coca-Cola Company which provides access to a broad portfolio of global beverage brands, creating significant brand equity leverage in these markets.

The company emphasizes efficient resource utilization alongside strong engagement with consumers, customers, suppliers, and community stakeholders fostering durable business resilience .

Historical Financial Performance

In fiscal year 2025, Andina posted revenues of approximately 3.345 trillion Chilean pesos (CLP), marking a growth rate of about 3.7% from the previous year’s revenue of around 3.224 trillion CLP [F1]. This rise reflects effective volume growth supported by value pricing adjustments despite persistent inflationary pressures across its operating regions.

Net income advanced notably by roughly 15.3% to about 270 billion CLP in the same period compared to nearly 235 billion CLP in FY2024 [F1]. This outperformance indicates successful margin management through cost-containment measures and operational leverage.

Equity capital at year-end stood at roughly 1.197 trillion CLP in 2025 versus approximately 1.014 trillion CLP the prior year, underpinning a return on equity near 22.6%, reflecting strong capital efficiency [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 3344.8 | 270.5 | +3.7% | +15.3% |

| 2024 | 3224.2 | 234.6 | +23.1% | +34.5% |

| 2023 | 2618.4 | 174.5 | -1.4% | +35.8% |

| 2022 | 2656.9 | 128.5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | ROE% |

|---|---|---|

| 2025 | 54.7 | 22.6 |

| 2024 | 266.8 | 23.1 |

| 2023 | 168.7 | 18.9 |

| 2022 | 275.4 | 14.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue and net income figures are rounded for readability.

Liquidity and Capital Structure

The company maintains solid liquidity with current assets totaling approximately 1.033 trillion CLP against current liabilities near 730 billion CLP at the close of FY2025, resulting in a current ratio of about 1.41 [F1]. Cash and equivalents amounted close to 297 billion CLP providing ample short-term flexibility.

Debt primarily comprises a blend of international bonds denominated in USD and CHF as well as local currency obligations (Chilean peso, Brazilian real, Argentine peso, Paraguayan guaraníes). The firm employs currency swaps and cross-currency derivatives effectively to hedge against exchange rate volatility particularly on USD- and CHF-denominated bonds [S7][S9][S10].

The weighted average interest rates on public debt instruments fluctuate between approximately 3.35% to over 4%, indicating manageable borrowing costs considering the diverse currency exposures [S8][S10].

Dividend Policy and Capital Allocation

In the fiscal year ending December 31, 2025, Andina declared dividend payments aggregating roughly 54.7 billion CLP, significantly lower than dividends paid out in previous years such as nearly 267 billion CLP in FY2024 [F1][S4][S6]. Series B shares receive dividends at a rate approximately ten percent higher than Series A shares reflecting different economic rights embedded in the two classes alongside voting distinctions outlining governance control mechanisms [S6][S14][S15].

Share repurchases are not prominently disclosed; capital allocation appears oriented toward maintaining moderate leverage while supporting consistent dividend distributions.

Future Growth Prospects

Growth drivers include expanding beverage consumption trends within Latin America’s sizable population centers coupled with ongoing penetration into diverse beverage segments as part of its Total Beverage Company strategy . Leveraging Coca-Cola's evolving product portfolio enables responsiveness to consumer trends such as low/no-sugar variants or functional beverages.

Regional geographic diversification reduces concentration risk although macroeconomic volatility associated with currencies such as the Brazilian real or Argentine peso could constrict margins [S23]. Ongoing investments into sustainability initiatives and supply chain efficiencies are expected to foster long-term operational resilience.

Regulatory updates like Chile’s CNCI reform facilitate smoother capital flows for foreign investors simplifying access and reporting for ADR shareholders which may positively impact the firm’s capital market profile [S1][S13][S19].

Close monitoring of commodity cost cycles—particularly sugar prices sensitive to crude oil movements—and currency exchange fluctuations remain imperative given their material impact potential [N7][N12].

Risk Factors

Key risks prominently flagged include commodity price volatility which can inflate input costs unpredictably affecting gross margins and pricing power dynamics regionally [S23]. Currency fluctuations pose translation risk on both earnings from operations abroad and servicing foreign currency debts despite hedging instruments employed.

Cybersecurity emerges as critical given the company's investments into ISO/NIST-aligned controls underpinning secure information systems continuity—essential for uninterrupted operations amid increasing digital threats [S23]. Regulatory compliance across multiple jurisdictions adds complexity requiring continual vigilance.

Observations on Industry Context (Analysis)

South American beverage bottlers face unique challenges including inflation pass-through capacity constrained by consumer purchasing power shifts amidst cyclical economic pressures accentuated by political uncertainty especially within Argentina or Brazil’s regulatory landscapes. Strategic alliances like that between Andina and Coca-Cola provide scale advantages enabling cost efficiencies through centralized procurement yet require adaptability to localized consumer tastes.

Capital structures incorporating index-linked local debt instruments (UF bonds) common in Chile help mitigate inflation exposure reducing real interest burden – an important feature for companies operating in inflationary environments common across LATAM markets.

Key Milestones & What to Watch Next (Analysis)

Investors should observe quarterly revenue growth trajectory relative to input cost inflation rates to assess margin sustainability as well as updates to capital expenditure plans targeting capacity expansion or technology upgrades highlighted during earnings releases or investor presentations.

Developments around further currency regime reforms or trade agreements within Mercosur impacting cross-border logistics could influence operating leverage favorably or unfavorably.

Additionally, dividend policy shifts or debt maturity profile refinements reveal management’s confidence in free cash flow generation capabilities under evolving macro conditions.

Summary Table: Selected Annual Financials (FY2022–FY2025)

| Metric | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|

| Revenue (CLP t) | 2,657B | 2,618B | 3,224B | 3,345B |

| Net Income (CLP b) | 128B | 175B | 235B | 270B |

| Equity (CLP t) | 883B | 921B | 1,014B | 1,197B |

| Dividends Paid (CLP b) | 275B | 169B | 267B | 55B |

| Current Ratio | - | - | - | 1.41 |

The table underscores consistent top-line growth punctuated by significant net income progress evidencing operational gains despite volatile local economic environments.

Conclusion

ANDINA BOTTLING CO INC continues to consolidate its leadership position among regional beverage bottlers by harnessing brand synergies with The Coca-Cola Company while executing robust financial discipline evident through stable liquidity metrics and prudent capital structure management amidst challenging macroeconomic conditions prevalent across its operating footprint.

Ongoing risks remain linked chiefly to external factors such as commodity pricing swings alongside currency exposure mitigated somewhat via derivative contracts but still warrant careful attention going forward.

Management's approach focusing on sustainability initiatives coupled with expanding product breadth positions Andina well strategically though navigating geopolitical uncertainties intrinsic to Latin American markets remains an imperative dimension of its growth narrative.

This report is based solely on publicly available documents including SEC filings ([F1], [S#]) and verified news sources ([N#]). It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments