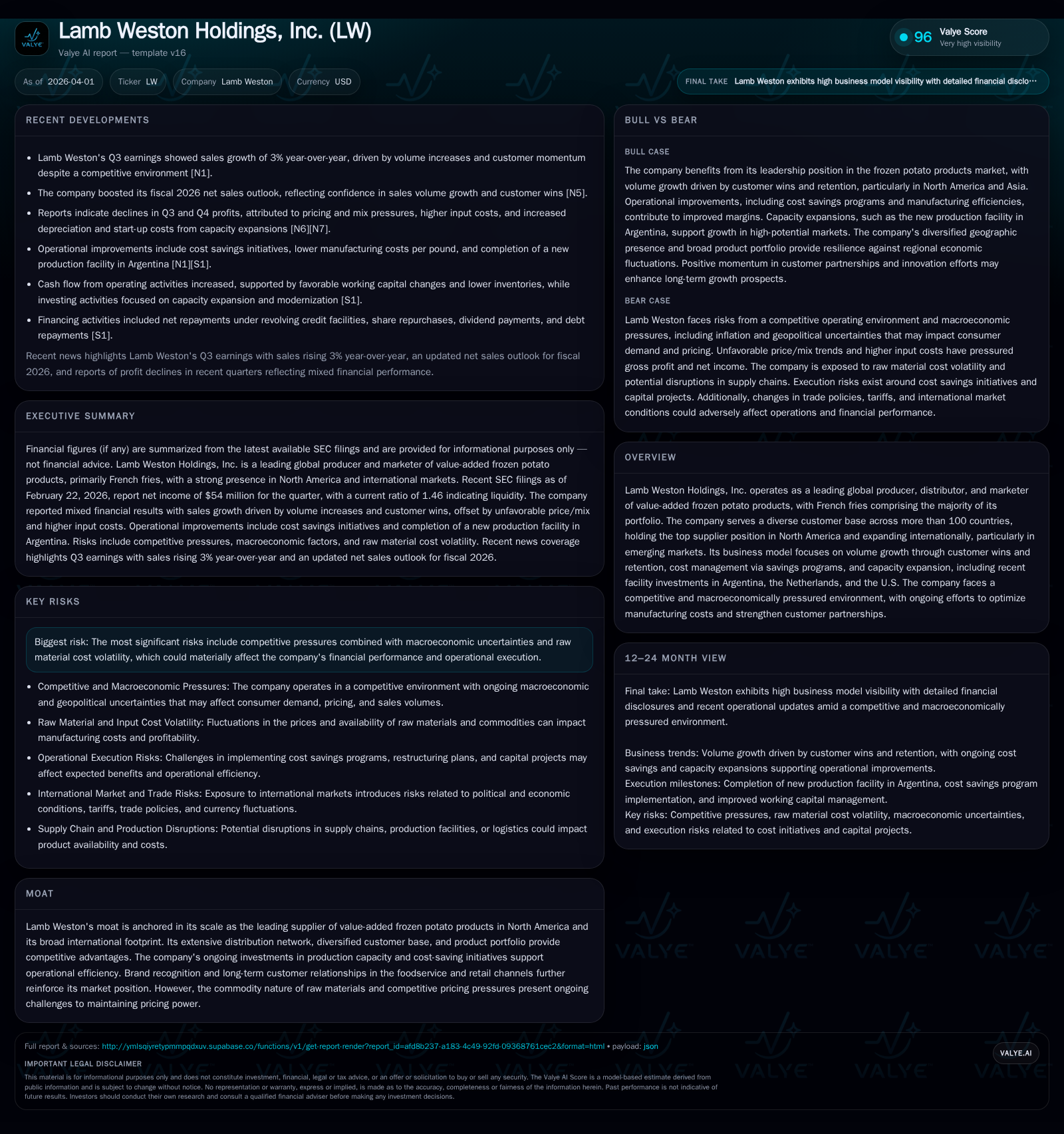

Lamb Weston Holdings: Volume Gains Offset Margin Pressures in a Competitive Frozen Foods Market

Lamb Weston balances expanding volumes and strategic investments against pressure on margins amid a challenging frozen potato product landscape.

Lamb Weston Holdings remains the leading supplier of value-added frozen potato products in North America, leveraging volume growth driven by customer wins and international expansion to partially offset pricing and mix challenges. Ongoing investments in capacity, particularly in Argentina, the Netherlands, and the U.S., are poised to support future growth but entail incremental costs. Despite operating income and net income declines over recent years, operational efficiencies and cost management initiatives have improved cash flow generation. The company’s capital allocation prioritizes dividends and prudent debt repayment, though raw material volatility and competitive pricing pressure pose significant risks ahead.

Steady Volume Growth Despite Pricing Challenges

Lamb Weston demonstrated resilient volume growth of approximately 6% year-over-year across its North American and international markets, notably driven by customer contract wins and retention in key regions including Asia [S5][S8][N1]. However, this momentum was tempered by a roughly 7% decline in price/mix, attributed to continued price and trade support initiatives for customers as well as an unfavorable channel mix shift particularly within North America [S5]. This dynamic reflects a classic trade-off often encountered in commoditized food categories where volume gains come at the expense of pricing power. The company’s net sales showed a slight increase at face value due to foreign currency benefits but were essentially flat on a constant currency basis when adjusting for mix effects [S8]. Importantly, gross profit contracted by about $13.6 million primarily due to these adverse price/mix dynamics despite lower manufacturing costs emerging from ongoing cost savings programs.

In sector vernacular, Lamb Weston's strategy leverages "trade support," a form of promotional pricing aimed at capturing or retaining shelf space or menu presence for its value-added frozen potato offerings. "Channel mix shifts" towards less premium or lower-margin customers also contributed negatively to revenue quality metrics [S5]. This combination necessitates close management of operating leverage to maintain profitability as volumes rise.

Capacity Expansion and Strategic Investments Bolster International Reach

Capital expenditures over recent periods reflect Lamb Weston's deliberate expansion into high-growth international markets alongside modernization efforts in home markets. Key projects include new or expanded production facilities in Argentina (commissioned Q1 Fiscal 2026), the Netherlands (completed Q2 Fiscal 2025), and prior investments finalized in the United States during Fiscal 2024 [S6][S17][N10]. These expansions are strategically aimed at increasing operational scale to meet rising demand from multinational chains and emerging market consumers.

These investments represent critical enablers for sustaining long-term volume growth beyond North America’s mature market environment. The ramp-up phase of these facilities incurs "incremental depreciation" expenses as well as startup costs—which have exerted near-term earnings pressure—but underscore Lamb Weston's commitment to securing future capacity and geographic diversification [S6][S17]. For instance, start-up costs related to Argentina’s new facility contributed $3.5 million expenses during recent quarters [S17]. This aligns with common capex profiles within processed foods manufacturing where timing lag between capital deployment and full productive output demands prudent margin management.

Cost Management Programs Yield Mixed Benefits

Lamb Weston has implemented a series of cost savings initiatives targeting manufacturing efficiencies and overhead controls. These efforts have successfully reduced manufacturing costs per pound of finished product while trimming adjusted selling, general & administrative (SG&A) expenses—adjusted SG&A declined by $24 million versus prior year quarters thanks partially to insurance recoveries and property tax refunds [S5]. Yet these gains were somewhat offset by inflationary pressures on raw materials (notably commodities), start-up expenses from new production lines, and normalization of employee incentive compensations extinct during peak pandemic disruption phases [S6][N1].

The complex interplay between inflationary input costs and operating leverage merits attention: while efficiencies create downward pressure on unit costs, elevated commodity prices erode margin sustainability absent corresponding price increases which may be limited due to competitive environments. Additionally, restructuring efforts aimed at consolidating operations—such as planned closure of an Argentinean plant—signal proactive cost rationalization though associated charges ($50–60 million) imply further short-term P&L impact [S24].

Financial Trends: Earnings and Cash Flow Under the Microscope

Examining four fiscal years from FY2022 through FY2025 reveals sharp earnings volatility underlying Lamb Weston's performance:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 357 | 868 | 665 | 638 | -50.8% |

| 2024 | 726 | 798 | 1065 | 930 | -28.1% |

| 2023 | 1009 | 762 | 882 | 654 | +402.2% |

| 2022 | 201 | 418 | 444 | 290 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 230 | 20.6 |

| 2024 | -131 | 40.6 |

| 2023 | 108 | |

| 2022 | 128 | 55.7 |

Source: SEC companyfacts cache [F1].

Despite the operating income halving between FY2024 and FY2025 (-37.6%), Lamb Weston notably improved cash flow from operations (+8.8%), largely attributable to better working capital management such as inventory reduction [F1][S14]. Capex retreated substantially (-31%) post-completion of major expansion projects—a cyclical normalization aiding free cash flow generation which amounted approximately to $230 million (= CFO minus capex) in FY2025.

Return on equity stands around a robust approximate level of 20.6%, calculated using FY2025 net income over year-end equity figures, underscoring efficient equity capital usage despite margin headwinds [F1].

Capital Allocation Priorities and Shareholder Returns

Consistent with generating positive cash flows amid challenging profitability trends, Lamb Weston has maintained disciplined capital distribution policies centered on dividends approximating $51.7 million paid during recent quarters [S4][S25][N9]. While share repurchases continue at modest levels—as evidenced by net cash outflows for buybacks near $18 million recently—the focus skews toward balancing debt reduction with shareholder returns [S14][N9].

Debt repayments totaling roughly $10-$16 million complemented liquidity management supported by sizable revolver availability (~$1.3 billion) ensuring flexibility for operational needs or opportunistic investments [S11][S23][F1]. Equity award-related share withholding programs address employee tax obligations on vested equity grants without full reliance on open market purchases [S4]. Overall liquidity remains healthy with current ratio near 1.46 bolstered by over $57 million cash equivalents as of early calendar year data points [F1].

Market Risks and Industry Headwinds Ahead

Primary risks emphasized include raw material price volatility—potato commodity costs alongside energy inputs—and ongoing competitive pressures that constrain ability to fully recover inflation through pricing models [S7][S9][S13]. Macroeconomic uncertainties such as geopolitical tensions influencing tariffs disrupt global supply chains affecting input availability or cost structures notably within international operations.

These risk factors also encompass uncertainties stemming from consumer demand patterns amidst fluctuating restaurant traffic levels globally; current trends suggest stagnation relative to prior years rather than growth which poses top-line limitations despite product desirability noted in "french fries" category persistence [S16][N14]. Furthermore, regulatory considerations including trade policies present potential negative contingencies with execution risks attached to ambitious restructuring or technology upgrades planned [S10][S16].

Outlook: What to Watch in Lamb Weston's Next Chapters

Although explicit forward guidance is cautious given competitive mix headwinds, management projects overall flat global restaurant traffic for fiscal year 2026 compared with prior year but anticipates volume growth reinforced by an additional operating week (53rd week adjustment) plus continued customer acquisition momentum [N10][S6][N1]. Operating earnings are expected under pressure owing primarily to input cost inflation, increased depreciation from capital assets online recently, ramp-up operating expenses related to expanded facilities plus higher compensation costs following normalization from pandemic-era deferments.

Key monitoring points include effectiveness of ongoing cost savings programs set against rising raw material prices; success metrics for ramping new capacities especially Latin America after consolidation moves (including exit from Munro site); trading margin recovery attempts amid shifting pricing/trade support balances; working capital optimization sustaining strong CFO trends; and maintenance of dividend policy coupled with manageable leverage sustainability at prevailing interest rate levels.

This analysis synthesizes reported financial data grounded in SEC filings alongside recent market disclosures without offering investment recommendations or projections beyond stated corporate communications or documented financials [F1][N#][S#]. Readers should consider industry factors comprehensively alongside company-specific insights presented herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments