Aspira Women's Health: Recalibrating Growth Through AI-Driven Diagnostics

Aspira Women’s Health faces steep revenue declines but leverages AI-powered assays and a strategic pipeline expansion to address gynecologic diagnostic gaps.

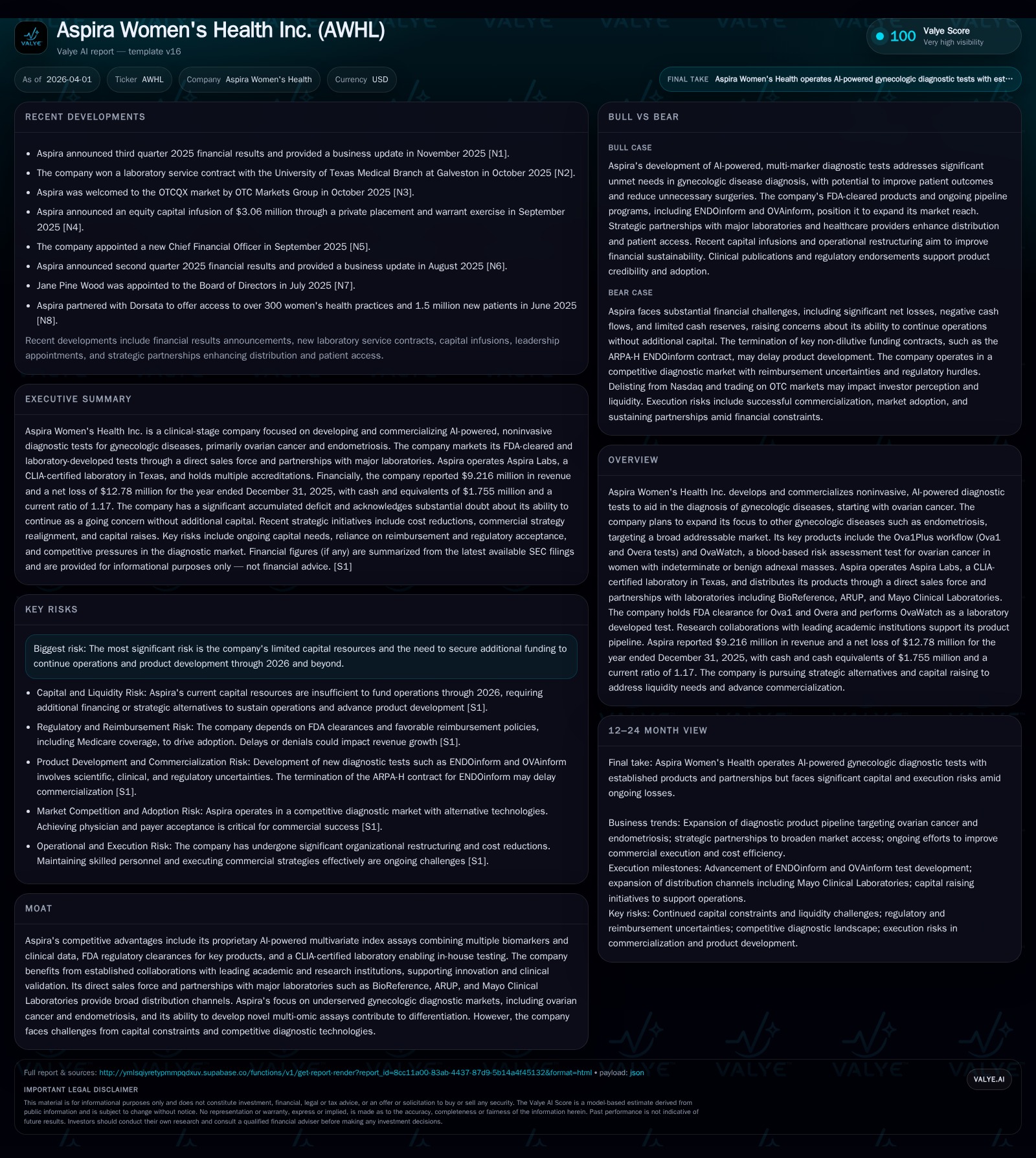

Aspira Women’s Health has experienced a precipitous drop in revenue, declining over 91% from $9.15 million in 2023 to $0.343 million in 2025, driven by operational shifts and market pressures. Despite this, the company is harnessing its proprietary AI-enabled multivariate index assays and FDA-cleared diagnostics as competitive moats while expanding into the larger endometriosis diagnostic market. Financial challenges persist with constrained capital resources and negative operating cash flows, but management is improving operating efficiency and pursuing new commercial contracts to stabilize performance. Key milestones include broadening Medicaid access and advancing pipeline launches, with funding availability representing the critical risk factor for sustained operations.

Severe Revenue Contraction: Tracing Historical Performance Drivers

Aspira Women’s Health’s revenue trajectory has undergone a stark contraction over the past three fiscal years, plummeting from $9.15 million in FY2023 to just $0.343 million in FY2025 — an over 91% decrease [F1]. This dramatic drop stems principally from strategic reconfiguration of its commercial footprint, notably a substantial reduction of sales efforts in markets lacking favorable reimbursement environments [S8]. The company also narrowed focus toward higher-margin opportunities which supported improved average unit pricing even as sales volumes contracted.

Operating expenses concurrently shrank markedly by approximately 36% year-over-year to $13.8 million in FY2025 driven by lower sales & marketing spend (down 63%) and reduced general administrative overheads [F1][S8]. The operating loss narrowed more than half to -$7.9 million in FY2025 from -$16.3 million the prior year [F1], highlighting some improvement in operational efficiency despite persistent unprofitability.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -13 | -7 | -8 | -91.4% | +2.4% |

| 2024 | 4 | -13 | -12 | -16 | -56.3% | +21.5% |

| 2023 | 9 | -17 | -16 | -19 | +11.9% | +44.2% |

| 2022 | 8 | -30 | -31 | -31 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | 184.4 |

| 2024 | -12 | 510.9 |

| 2023 | -16 | 705.7 |

| 2022 | -31 | -428.2 |

Source: SEC companyfacts cache [F1].

Despite revenue erosion by scale factors — likely contraction or exit of certain channels — management's actions on pricing optimization and selective account targeting have somewhat softened profitability erosion [S8]. Notably absent is meaningful top-line growth evidence post-2023 signaling a fundamental shift rather than cyclical variation.

Artificial Intelligence and Proprietary Assays as Differentiators

At its core Aspira leverages proprietary AI-driven multivariate index assays (MIA), integrating multiple biomarkers with clinical metadata to deliver superior diagnostic accuracy over conventional single-marker tests such as CA-125 [S1]. Its flagship OvaSuite products—including FDA-cleared Ova1Plus assays (Ova1 and Overa) complemented by OvaWatch—enhance ovarian cancer risk assessment capabilities particularly for women with indeterminate or benign adnexal masses.

Operating Aspira Labs under CLIA certification ensures in-house testing control critical for assay reliability and regulatory compliance [S1]. This vertical integration strengthens pathways for iterative assay improvements critical in biomarker-driven diagnostic validation frameworks prevalent within the medical diagnostics sector.

FDA clearance underscores regulatory endorsement conferring competitive moat protection rare among early-stage women’s health diagnostics companies [S1][F1]. Combined with academic collaborations enhancing clinical evidence bases for assay performance differences across diverse populations further underpins differentiated positioning.

Strategic Shift Toward Endometriosis: Expanding Market Reach

Recognizing ovarian cancer’s niche market size limitations inherent in diagnostics adoption curves Aspira has pivoted toward endometriosis—a chronic gynecologic condition affecting approximately 10% of reproductive-age women in the U.S., equating to roughly 6.6 million affected individuals [S1]. Its ENDOinform program aims to develop a non-invasive multi-marker test combining serum proteins with microRNA signatures plus rich clinical metadata inputs.

This approach responds directly to the significant unmet need in endometriosis diagnosis characterized by invasive procedures or delayed detection hampering treatment outcomes [S1]. The projected enlarged addressable patient base offers potential revenue growth expansion past ovarian cancer test offerings.

Operational Efficiency Gains Amid Financial Constraints

In light of financial headwinds management undertook sizable operational realignments focusing sales force allocation toward regions yielding better insurance reimbursement outcomes while trimming efforts elsewhere [S8]. Marketing investments were pruned aggressively where return visibility was lacking; sales training revised with compensation structures linked more intensively to profitability metrics [S8].

Vendor agreements were renegotiated downwards or shifted to lower-cost alternatives maintaining service standards [S8]. The company fortified entry into marquee institutional accounts securing contracts with Mayo Clinical Laboratories and beginning volume generation via Cleveland Clinic Foundation collaborations.[S8]

Collectively these measures contributed materially to a halving of operating losses year-over-year alongside a significant reduction in operating cash consumption [F1][S8]. Nonetheless net loss levels remain elevated reflecting ongoing scale-down consequences somewhat blunting margin leverage benefits.

Capital Structure and Liquidity: Navigating Funding Challenges

Aspira faces acute capital constraints evident from shrinking cash reserves ($1.76 million end-2025) confronted by current liabilities exceeding $3.46 million yielding a modest current ratio of ~1.17x [F1][S10]. This liquidity squeeze drove multiple capital raises including issuance of convertible notes totaling approximately $1.37 million during March 2025 along with subsequent equity private placements and ATM offerings netting multimillion inflows partially offsetting imminent repayment obligations [S5][S12][S13][S27].

Loan obligations include the Connecticut DECD loan secured against company assets now subject to troubled debt restructuring due to payment deferrals extending maturities into mid-2027 range [S9][S11][S18], underscoring strained debt service capability amid lackluster earnings.

Further exacerbating capital burdens was the April 2025 delisting from Nasdaq after failure to maintain minimum stockholders’ equity threshold ($2.5 million), shifting shares trading venue to OTC QX Market under ticker "AWHL" which typically reduces liquidity profile for investors seeking listed stock exposure [S4][S21].

No dividends or share buybacks have been executed since at least FY2016 reflecting prudent capital conservation aligned with operational needs [F1][S16]. Equity deficit deepened substantially during FY2025 to near -$6.93 million eroding shareholder value proxies though somewhat expected given cumulative losses trajectory.

Forecasting Recovery: Pipeline Milestones and Commercial Execution

Absent formal numeric guidance the company's narrative highlights anticipated commercial progress concentrated on launching endometriosis diagnostics leveraging ENDOinform assay advances alongside ongoing maturation of ovarian cancer test adoption [S1][S8]. Expansion into Medicaid patient populations is prioritized aligned with corporate mission promoting care accessibility across socioeconomic strata.

Legislative advocacy aimed at securing biomarker coverage mandates among public/private payers alongside incorporation of tests into professional clinical guidelines represent pivotal catalysts underpinning broader reimbursement acceptance trajectories outlined by management [S1].

Market uptake success depends critically on navigating payer acceptance complexities inherent for novel biomarker-driven blood diagnostics competing within diagnostic reimbursement ecosystems often entailing protracted evidentiary reviews.

Risk Outlook Centered on Capital Availability and Competitive Dynamics

Per official risk disclosures capital resource limitations constitute existential threats potentially curtailing research progress or operability beyond late-2026 absent successful financing rounds or alternative revenue surges [S22]. The termination of a large ARPA-H contract related to ENDOinform milestone failures further removed non-dilutive funding fueling near-term development expenditures underscoring volatility risks [S21][S28].

Competitive pressures emanate not only from traditional biomarkers or reagent kit providers but increasingly from liquid biopsy platforms applying next-gen sequencing or multi-cancer early detection paradigms potentially overlapping women's health diagnostics space demanding continuous innovation investment [S22]. Regulatory scrutiny post-market surveillance demands add ongoing cost layers complicating scaling dynamics while legal/labeling compliance enforcement risks persist due to strict FDA medical device regulations governing AI-enabled diagnostics.

Evaluating Returns: Cash Flow, ROE, and Capital Allocation

Financial health indicators underline continuing stress despite operational improvements; operating cash flow consumption improved by approximately 42% YoY narrowing from -$12.11 million in FY24 to -$7.03 million FY25 [F1]. Capital expenditure plummeted nearly 57% YoY reflecting austerity measures though free cash flow remains deeply negative near -$7 million indicating few immediate self-sustaining qualities absent funding inflows.

Equity position deteriorated markedly rendering reported ROE mathematically inflated at over +184%, yet effectively meaningless given extensive accumulated deficit surpassing equity base size [F1]. No dividend payouts nor share repurchases have been undertaken consistent with prioritizing liquidity preservation amid uncertain near-term profitability prospects [F1][S16].

Disclaimer: This analysis is intended solely for informational purposes using publicly available data as of April 2026; it does not constitute investment advice or recommendations regarding Aspira Women's Health Inc.'s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments