MSC Industrial: Earnings Pressure and Capital Structure under Scrutiny

MSC Industrial faces compressed operating margins and constrained liquidity amid cautious capital allocation.

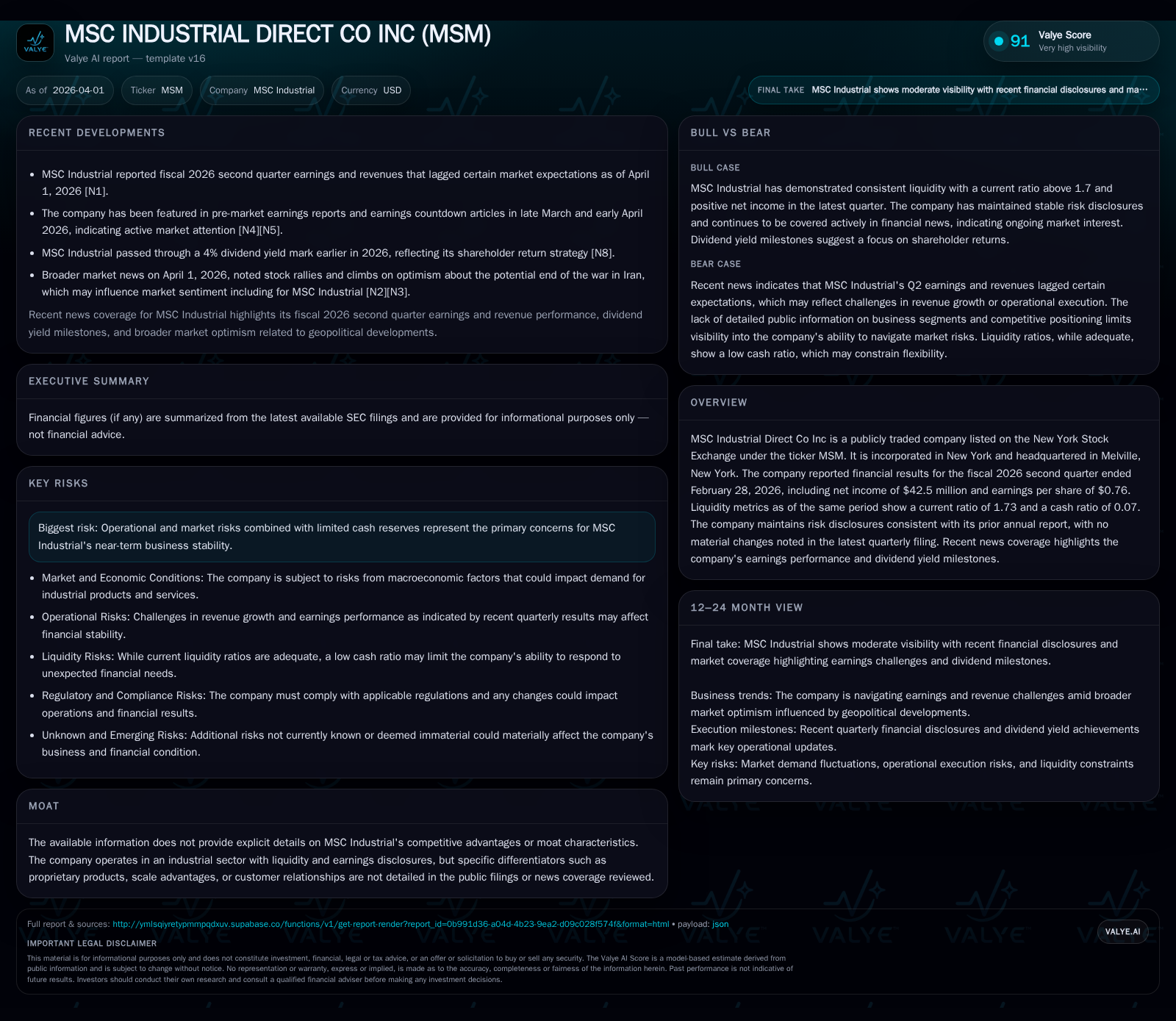

MSC Industrial Direct Co., Inc. reported modest revenue growth alongside significant declines in operating and net income for fiscal year 2025, highlighting emerging profitability pressures. The company’s liquidity profile shows a solid current ratio but limited immediate cash reserves. Capital allocation reflects consistent dividends supported by free cash flow, with a marked reduction in share repurchases, indicating prudent shareholder return management amid operational challenges. Monitoring margin recovery and free cash flow trends will be key to assessing financial health going forward.

Financial Performance Trends: Revenue Stability Meets Operating Headwinds

MSC Industrial’s fiscal year 2025 results reveal a divergence between flat revenue growth and notable profitability pressure. Revenue increased slightly by 0.6% year-over-year to approximately $842.7 million, reflecting subdued demand or pricing pressures within its industrial distribution business segments ([F1]). However, operating income fell sharply by nearly 23% to about $301.6 million compared to prior years, indicating margin compression likely driven by cost pressures.

Net income followed suit with a decline of 22.9% to around $199.3 million. Operating cash flow receded by roughly 18.7% to $333.7 million while capital expenditures decreased modestly by approximately 6.6%, suggesting management’s cautious stance on investment amid operational challenges ([F1]).

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 199 | 334 | 302 | 93 | -22.9% |

| 2024 | 259 | 411 | 390 | 99 | -24.7% |

| 2023 | 343 | 700 | 484 | 92 | +1.0% |

| 2022 | 340 | 246 | 469 | 61 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 39 | 241 | 14.4 |

| 2024 | 188 | 311 | 18.6 |

| 2023 | 96 | 607 | 23.2 |

| 2022 | 27 | 185 | 25.2 |

Source: SEC companyfacts cache [F1].

This historical snapshot highlights MSC’s profitability deceleration from stronger prior levels toward ongoing margin pressure.

Drivers Behind Growth Deceleration

The subdued revenue growth combined with profit contraction aligns with sector-wide inflationary cost pressures affecting raw materials and logistics costs as noted in recent earnings commentary ([N1]). Competitive dynamics within industrial distribution likely exerted pricing pressure as well.

Macroeconomic uncertainties impacting manufacturing capital expenditure budgets may have constrained order volumes and transaction sizes ([N3]). Risk disclosures confirm no material change in operational risks but emphasize exposure to cyclical demand fluctuations ([S2], [S4]). Supply chain conditions remain a factor influencing inventory management and working capital.

Operational Challenges Impacting Margins

Lower operating income despite flat revenues suggests margin erosion driven by cost inflation and fixed cost absorption issues ([F1]). Declines in operating cash flow point toward working capital pressures including receivables collection or inventory buildup.

Capex reductions indicate management efforts to optimize spending amid uncertain returns while maintaining necessary infrastructure support for customer service standards.

Liquidity and Capital Structure: Tight Cash Reserves Amid Adequate Current Assets

As of the second quarter ended February 28, 2026, MSC Industrial reported a current ratio near 1.73 reflecting sufficient short-term asset coverage relative to liabilities ([F1], [S2]). Contrasting this is a low cash ratio estimated at about 0.07 indicating limited immediately accessible cash balances versus current obligations.

Debt filings show continued use of financing facilities without major covenant changes or deleveraging initiatives during the period ([S6], [S8], [S10], [S11]). This underscores the need for disciplined liquidity management given industry seasonality.

Capital Allocation: Dividends Sustained While Repurchases Slow

MSM has maintained dividend payments supported by moderate free cash flow after capex—approximately $241 million—reflecting commitment to shareholder returns amid earnings pressure ([F1]). However, share repurchase activity has slowed markedly from previous years (e.g., $39 million repurchased in FY2025 versus $188 million in FY2024), signaling more conservative capital return policies aligned with balance sheet preservation ([F1], [S7], [S9], [S14], [S15]).

Recent shareholder approvals for stock plan amendments increase potential equity issuance but do not indicate aggressive buyback expansions ([S7]). Overall capital deployment appears focused on sustaining liquidity while maintaining shareholder distributions prudently.

Forward-Looking Considerations

While explicit guidance is limited, investor focus should remain on quarterly margin trends and free cash flow stability as indicators of operational recovery ([N3]). Upcoming quarterly reports covering March-end results will be key for assessing cost controls and inventory management effectiveness ([S18],[S19]).

Monitoring credit facility utilization against covenants may also provide early signals regarding financial flexibility under stress given low cash reserves.

Risk Profile Remains Consistent

Risk factor disclosures reiterate typical cyclical demand risks and liquidity concerns without new material developments or legal contingencies reported ([S2],[S4]). The absence of unique competitive advantages places emphasis on execution discipline amid market volatility.

This analysis reflects publicly filed financial statements and regulatory disclosures through April 2026 without extrapolations beyond reported data points and aims to provide an objective assessment of MSC Industrial’s recent financial trends.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments