Tenaris S.A.: Sustaining Market Leadership Amid the Cyclic Energy Sector

An in-depth review of Tenaris’s financial performance, operational execution, capital strategy, and outlook shaped by the energy sector's cyclical dynamics.

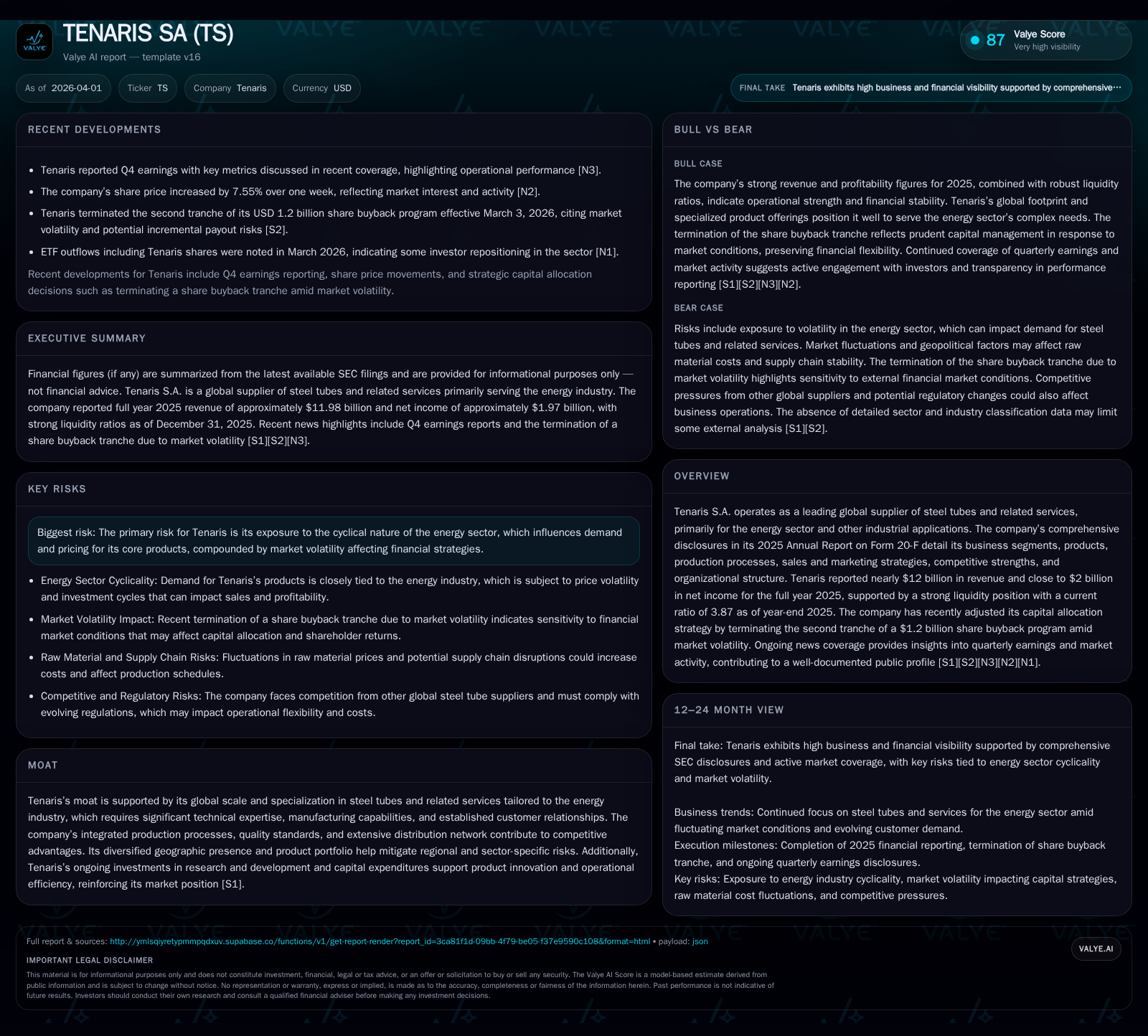

Tenaris S.A. remains a dominant global supplier of steel tubes specialized for the energy industry, generating nearly $12 billion in revenue and close to $2 billion in net income in 2025. Despite a 4.3% decline in revenue and a 5% dip in net income year-over-year fueled by sector cyclicality, the company maintained robust liquidity and a strong equity base. Strategic capital allocation saw the suspension of its share buyback program amid market volatility, balanced with continued dividend growth. Future growth hinges on sustained innovation and navigating sector risks linked to oil and gas investment cycles.

Tenaris’s Historical Financial Performance: Growth Drivers and Year-Over-Year Changes

Tenaris S.A., positioned as a foremost global supplier specializing in steel tubes for the energy sector, recorded revenues of approximately $11.98 billion in FY2025. This represented a decline of 4.3% compared to $12.52 billion in FY2024 [F1]. The decrease correlates primarily with diminished capital expenditure cycles within the upstream oil and gas sector that historically dictate demand for tubular goods. Net income similarly contracted by about 5%, falling from $2.08 billion to around $1.97 billion year-over-year [F1]. These figures reflect the intrinsic cyclicality inherent in Tenaris’s primary end markets.

Despite this pressure on top-line and profitability metrics, Tenaris sustained uninterrupted operations across diverse geographies, leveraging scale and segment breadth to partially offset regional swings [S1][S5]. The comparison against prior years illustrates volatility typical for sectors tied closely to commodity price-driven capex decisions:

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 12.0 | 2.0 | -4.3% | -5.0% |

| 2024 | 12.5 | 2.1 | -15.8% | -47.5% |

| 2023 | 14.9 | 4.0 | +26.4% | +55.3% |

| 2022 | 11.8 | 2.5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 932 | 11.7 |

| 2024 | 764 | 12.4 |

| 2023 | 655 | 23.2 |

| 2022 | 542 | 18.2 |

Source: SEC companyfacts cache [F1].

Table: Tenaris annual financial summary highlighting revenue fluctuations largely driven by energy sector capex cycles alongside dividend increases supporting shareholder returns [F1].

Operational Highlights and Segment Insights: Production, Products, and Markets

Tenaris operates primarily within the tubular goods manufacturing realm, serving the complex needs of the global energy industry—mainly oil and gas exploration and production—as well as other industrial applications [S1][S5]. The company’s integrated production model spans upstream steps from raw steel processing through finishing treatments designed to comply with rigorous product quality standards vital to subsea and high-pressure environments.

Its vertically integrated supply chain extends globally with manufacturing hubs strategically located near key oil-producing regions, enabling logistical efficiencies that bolster its competitive moat [S5]. This comprehensive footprint allows Tenaris to manage delivery lead times effectively while tailoring products such as premium connections or casing/tubing solutions to customer specifications.

The company's extensive product portfolio includes seamless and welded steel pipes designed under stringent mechanical property regimes reflecting API standards prevalent across exploration equipment specifications [S5]. This specialization distinguishes Tenaris within a marketplace where technical reliability under extreme operational conditions is essential.

Capital Allocation Strategy: Buybacks Halted Amid Volatility and Dividend Trends

In pursuing shareholder returns while maintaining balance sheet prudence amidst an uncertain commodity price environment, Tenaris executed a substantial share repurchase program announced in May 2025 with an aggregate target of $1.2 billion split into two tranches [S4][S11]. After repurchasing approximately $583 million worth of shares during the second tranche starting November 2025, management determined early termination following heightened market volatility risks related to fluctuating oil prices that could impose disproportionate payout obligations under its buyback agreements [S4].

Concurrently, dividends steadily increased each fiscal year culminating in approximately $932 million distributed in FY2025—an endorsement of management’s commitment to consistent cash return despite caution on capital redeployment via repurchases [F1][S15]. Tenaris’s capital strategy thus demonstrates a calibrated approach that favors liquidity preservation without sacrificing shareholder income streams.

Future Growth Prospects: Innovation, Market Risks, and Sector Dynamics

The company's future revenue trajectory heavily depends on cyclical oil & gas activity levels which dictate tubular goods demand.[S6] To mitigate cyclicality impacts, Tenaris invests strategically in research & development concentrating on innovations that enhance product quality, operational efficiency, and environmental compliance.[S9] These efforts help sustain differentiated offerings essential when facing cost pressures during capex downturns.

However, risks remain notable given external uncertainties about oil price fluctuations which can abruptly alter upstream spending patterns.[S6] Management highlights these cyclic trends explicitly among principal risk factors affecting sales volumes and pricing power.

Against this backdrop, Tenaris’s commitment to maintaining technical leadership through sustained capex directed at manufacturing process upgrades underpins its ability to capture emerging opportunities as new exploration technologies develop.[S1][S9]

Financial Health Indicators: Liquidity, Debt Structure, and Return Metrics

At year-end December 31, 2025, Tenaris demonstrated solid liquidity with current assets exceeding liabilities by a factor of nearly four (current ratio of 3.87), reinforcing short-term financial flexibility [F1][S13]. Cash equivalents were substantive at roughly $573 million supporting working capital needs.

The company adopted a conservative leverage stance preserving capacity for strategic investments or navigating extended industry downcycles.[S13] Equity remained stable near $16.8 billion illustrating a robust capitalization base sustaining approximately an 11.7% annual return on equity based on trailing net income figures from FY2025 [F1]. This level indicates effective use of shareholders’ equity despite margin pressures.

Expectation Setting: Key Milestones and Analytical Triggers to Monitor

While no explicit forward guidance has been issued post-annual report filings,[N1] stakeholders should monitor forthcoming quarterly earnings announcements for updates on demand trends and margins within core tubular segments.[N1]

Attention will also focus on any board decisions concerning renewal or modification of share repurchase initiatives given prevailing volatility concerns.[S4]

Finally, broader macro considerations such as global oilfield services capex intentions will significantly influence top-line visibility for the coming periods.[N3] ETF flows related to energy subsectors provide auxiliary sentiment signals warranting close observation.[N3]

This analysis synthesizes comprehensive SEC disclosures alongside recent news coverage without providing investment advice or forecasts beyond documented disclosures ([F1],[S#],[N#]). Readers should undertake independent due diligence when interpreting company prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments