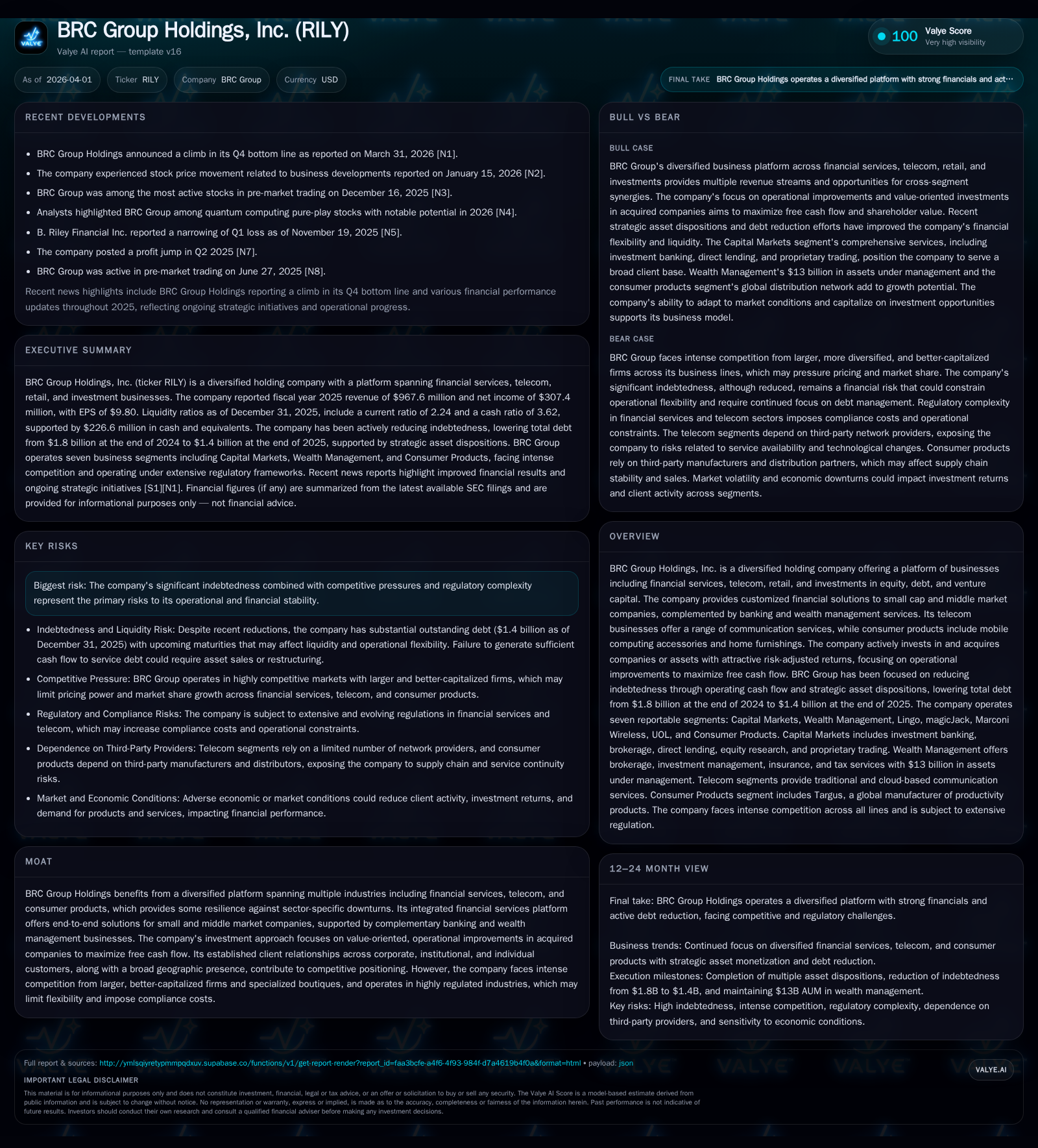

BRC Group’s Turnaround: From Sharp Losses to Financial Resilience

BRC Group Holdings transformed its financial health from a deep loss in 2024 to a robust profit in 2025 through strategic debt reduction and operational shifts.

BRC Group Holdings, Inc. demonstrated an impressive recovery trajectory in fiscal year 2025, shifting from a net loss of $764 million in 2024 to a net income of $307 million. This turnaround was fueled largely by focused debt reduction—from $1.8 billion to $1.4 billion—and operational improvements across its diversified platform spanning financial services, telecom, and consumer products. The company remains challenged by negative operating cash flow and substantial legal risks but prioritizes deleveraging and free cash flow maximization through asset dispositions and strategic capital deployment.

Transformation Overview: From Volatility to Stability

BRC Group Holdings’ FY2025 results pronounce a stark reversal from the deep financial distress seen in the prior year. Where FY2024 closed with a net loss of $764 million and an operating loss of nearly $476 million, FY2025 recorded net income surging to $307 million alongside positive operating income of roughly $76 million [F1]. This dramatic rebound underscores the success of operational restructuring efforts and aggressive deleveraging measures implemented over the period. By driving earnings into positive territory while reducing top-line volatility through targeted asset dispositions, BRC has laid the groundwork for incremental financial stability.

Historical Growth Patterns and Operational Shifts (2022-2025)

Examining the four-year trajectory reveals marked revenue fluctuations influenced heavily by divestitures and strategic repositioning. After near quadruple growth from $382 million in FY2022 to $1.64 billion in FY2023—largely reflecting acquisitions and expanded operations—revenue contracted sharply to $839 million in FY2024 amid significant asset sales [F1]. FY2025 saw a recovery to approximately $968 million (+15.4% YoY), signaling resumed operational momentum.

Operating income followed suit with initially modest profits ($10 million) in FY2022 progressing to strong gains ($145 million) in FY2023 before plunging into substantial losses (-$475 million) correlating with the disruptive impact of restructuring costs and impairments [F1]. A return to profitability ($76 million) materialized in FY2025 as cost controls took effect.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 968 | 307 | -60 | 76 | +15.4% | +140.2% |

| 2024 | 839 | -764 | 264 | -476 | -49.0% | -665.0% |

| 2023 | 1644 | -100 | 25 | 145 | +330.2% | -73.9% |

| 2022 | 382 | -57 | 7 | 10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | -179.2 | |

| 2024 | 0 | 156.6 |

| 2023 | 69 | -34.3 |

| 2022 | 7 | -12.9 |

Source: SEC companyfacts cache [F1].

Note: Capex data is not consistently available for recent years; operating cash flow indicates fluctuating liquidity generation capacity [F1].

Debt Reduction Strategy and Liquidity Management

A defining pillar of BRC’s recent turnaround is its resolute reduction of debt obligations—from $1.8 billion at the close of 2024 down to roughly $1.4 billion at the end of 2025—as it channeled proceeds from asset monetizations and operating cash flows towards deleveraging [S1][S4][S7]. Strategic dispositions such as transferring brand assets generated significant upfront payments (~$189 million) employed directly for debt paydown [S7]. Recent redemption of approximately $96 million face value of senior notes further illustrates active liability management [S4].

Despite these advances, looming maturities totaling about $355 million across senior notes due within the next twelve months impose sustained refinancing pressure on liquidity channels [S4][S6]. Covenants embedded in these debt instruments impose operational restrictions that may constrain agility should macroeconomic credit conditions deteriorate [S6][S14]. Additionally, operating cash flow turned negative again in FY2025 (-$60 million), revealing persistent free cash outflow challenges despite accounting profits [F1]. This discrepancy highlights typical timing mismatches between accrual earnings and realized cash.

Diversified Business Platform and Market Positioning

BRC’s wide-ranging platform integrates businesses across specialized financial services—including capital markets advisory, merchant banking, M&A restructuring—with telecom operations delivering voice, data, cloud-based services, alongside consumer retail offerings such as mobile computing accessories and home furnishings [S1][S5][S16]. Its core financial services segment focuses on tailored solutions for small cap and middle market companies with complementary banking and wealth management arms bolstering client retention via full-lifecycle service coverage.

Competitive advantages stem from this diversification: intersegment synergies enable operational improvements within portfolio companies aimed at maximizing free cash flow extraction [S1][S9]. However, BRC faces intense competition from larger banks and boutique specialists equipped with deeper capital resources capable of offering broader service scopes potentially exerting pricing pressure across advisory and investment product lines [S9][S10][S17]. Telecom segments compete vigorously against entrenched providers offering broadband, VoIP, mobile phone services amid accelerating technology shifts [S9][S10].

Capital Allocation: Dividends, Buybacks, and Cash Flow Trends

Reflecting both prior losses and ongoing liquidity constraints, BRC has abstained from dividend payouts since at least 2018 [F1], favoring retention for debt servicing and operational needs amid fluctuating free cash flow. Share repurchase activity plummeted after an elevated buyback program culminating at nearly $70 million in FY2023 down to zero repurchases reported for FY2024—correlating with preservation measures during heavy restructuring phases [F1][S13][S23][S24].

The firm’s equity remained deeply negative at approximately -$172 million at fiscal year-end 2025 after contracting markedly from positive territory earlier in the decade—mirror imaging cumulative retained losses reflecting difficult prior cycles [F1]. Return on equity metrics computed naively would thus appear severely impaired; this underscores ongoing balance sheet repair rather than traditional profitability performance metrics [F1].

Regulatory and Legal Challenges Impacting Strategic Choices

Legal complexities loom large for BRC as legacy issues stemming from prior investments—in particular Freedom VCM—and associations with scrutinized individuals have led to SEC subpoenas along with shareholder derivative complaints asserting breaches by officers and board members [S18][S19][N1][S25]. These proceedings have imposed reputational damage reflected also in depressed share price performance amidst heightened short selling pressures.

Further complicating matters are comprehensive regulatory compliance demands across its diverse businesses encompassing stringent broker-dealer oversight under the Exchange Act, investment adviser regulatory frameworks, plus telecommunications licensing regimes subject to federal/state approvals impacting M&A timelines [S18][S25]. Any adverse outcomes here could materially affect operational flexibility or lead to increased reserves for contingent liabilities absent recognized accounting provisions yet posing potential large-scale financial downside risks.

Forward-Looking Indicators and Key Watchpoints

Looking ahead, market participants should closely monitor BRC's ability to effectively manage imminent senior note maturities aggregating over $350 million before year-end 2026 alongside its capability to extract consistent positive operating cash flows signaling durable earnings quality improvement beyond accrual-based results [N1][S4][F1]. Additional monetization transactions remain likely given stated priorities around continued debt reduction [S7]. Macro-level developments affecting credit availability within financial services sectors will materially influence transactional activity volumes which are critical drivers of revenue generation within BRC’s core advisory units [S6][S15].

Furthermore, settlement or resolution progress regarding legal proceedings linked to historical relationship exposures should be watched for their implications on settlement costs or reputational remediation enabling normalized commercial operations [N1][S18]. Competitive responses by larger rivals or boutique investment firms expanding into middle-market domains may continue pressuring advisory fees requiring BRC’s differentiation through expertise depth and client service integration.

This analysis synthesizes publicly available regulatory filings as of April 1, 2026 ([F1], SEC documents), supplemented by news reports ([N1]). It aims only to review historical trends and forward-looking factors without issuing investment advice or forecasts unsupported by explicit disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments