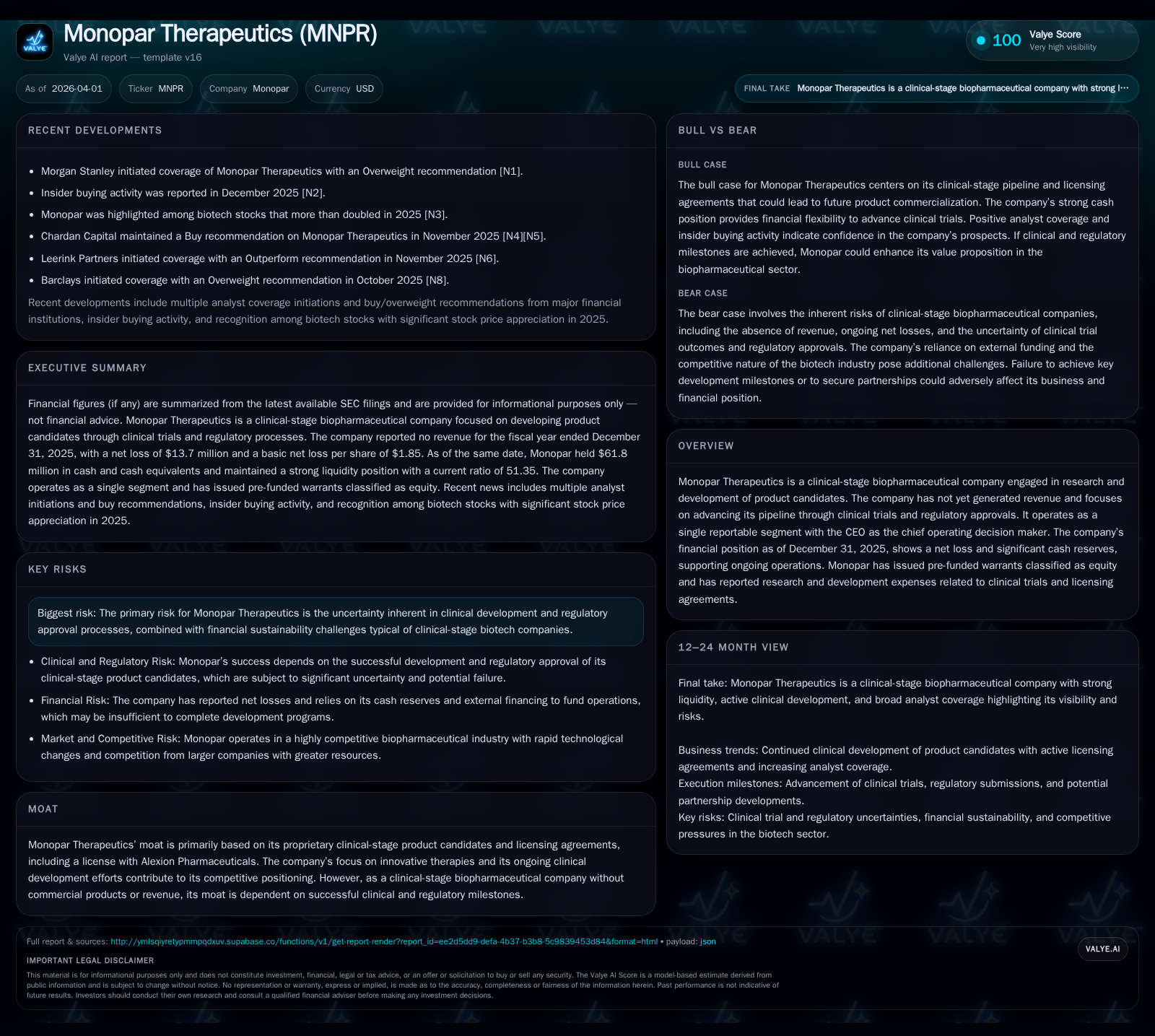

Monopar Therapeutics’ Strategic Licensing and Clinical Development Shape Its Road to Regulation and Revenue

Monopar Therapeutics maintains financial stability while progressing oncology radiopharmaceuticals and a late-stage Wilson disease candidate toward regulatory milestones.

Monopar Therapeutics remains a clinical-stage biopharma focused on innovative therapeutic development without current revenue generation but supported by strong liquidity. Its pipeline includes licensed late-stage asset ALXN1840 targeting Wilson disease and proprietary uPAR-targeted radioligand therapies in early-phase trials. Despite sustained operating losses driven by heightened R&D spend, Monopar's cash reserves and prudent capital allocation—including a reverse stock split for Nasdaq compliance—position it well to fund operations through at least 2027. Upcoming regulatory or clinical readouts represent critical milestones, though risks typical to biotech development and funding continue to weigh.

From Operating Deficits to Pipeline Momentum: Historical Financial Trends

Monopar Therapeutics has maintained a consistent operating stance characteristic of a clinical-stage biopharmaceutical company — no revenues recorded from fiscal years 2019 through 2025 as all efforts are deployed toward product candidate development rather than commercialization [F1]. Operating income has remained negative but reveals a controlled increase in losses: FY2025 operating income was -$16.7 million, worsening marginally by approximately 3.4% compared to FY2024's -$16.2 million, mainly reflecting escalating clinical trial activities and licensing expenditures tied to expanding pipeline advancement [F1]. Net income data corroborate this pattern; despite sustained losses, FY2025 net loss showed a slight improvement of about 12%, standing at -$13.7 million versus -$15.6 million in the prior year [F1]. This relative improvement suggests disciplined operating management amid heavier research expenses.

However, operating cash flow tells a cautionary tale with a sharp deterioration of -90.5% in FY2025 to a negative $12.2 million from -$6.4 million in FY2024, indicating intensified cash outlays likely related to clinical trial site activities, patient enrollment expenses, pre-funded license payments (notably to Alexion), and preparatory regulatory work [F1][S13]. This divergence between net loss improvement and deteriorating cash flow highlights ongoing investment phase dynamics common in biotech ventures transitioning from discovery into expensive pivotal trials.

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -14 | -12 | -17 | +12.0% |

| 2024 | 0 | -16 | -6 | -16 | -85.5% |

| 2023 | 0 | -8 | -8 | -9 | +20.1% |

| 2022 | -11 | -7 | -11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -10.0 |

| 2024 | -28.3 |

| 2023 | -150.4 |

| 2022 | -104.2 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary (FY2019–2025). Note: Negative percentages denote deterioration; equity surged primarily due to capital raises.

Clinical Candidates Driving Innovation: Portfolio Highlights and Development Status

Monopar's pipeline is anchored by two strategic pillars: ALXN1840—a genetically licensed product candidate sourced via license agreement with Alexion Pharmaceuticals—and its internally developed radiopharmaceutical program targeting the urokinase plasminogen activator receptor (uPAR).

ALXN1840 represents a late-stage investigational oral therapy designed for Wilson disease treatment—a genetic disorder characterized by aberrant copper accumulation [S6][S1]. As an oral once-daily candidate advancing toward potential registration-enabling studies or submissions under FDA scrutiny standards typical of orphan indications, ALXN1840 exemplifies high-risk/high-reward innovation with predicted accelerated pathway benefits if regulatory interactions proceed favorably.

Simultaneously Monopar pursues an oncology-focused radioligand therapy franchise comprising three uPAR-targeted agents designated MNPR-101-Zr (Phase 1 imaging agent), MNPR-101-Lu (Phase 1a therapeutic agent), and MNPR-101-Ac (late preclinical stage). These candidate modalities engage tumor cells expressing uPAR selectively; the radiolabeled compounds enable direct cytotoxicity combined with diagnostic imaging utility—hallmark features of emerging precision oncology treatments [S6]. The progression through early-phase clinical trials for these agents underscores Monopar’s commitment to validate target engagement and optimize dosing regimens within the complex terrain of nuclear medicine drug development.

Together with licensing assets and proprietary developments integrated via scientific collaborations—evidenced by milestone payments classified as in-process research and development expense—the company leverages dual pathways that reduce risk exposure compared to earlier-stage biotech companies that develop wholly new chemical entities [S13].

Liquidity Arsenal and Balance Sheet Position: Assessing Financial Sustainability

Maintaining robust liquidity is crucial given Monopar’s path-dependent evolution hinged on costly late-stage trials. As of December 31, 2025 Monopar held $61.8 million in cash and equivalents supported by short-term high-credit-quality fixed income instruments including U.S. Treasury securities ($30.1M amortized cost) and commercial paper ($48.4M amortized cost), predominantly classified as held-to-maturity investments ensuring minimal credit risk exposure [S6][S7][S8][F1].

Current assets totaled an impressive $140.5 million versus current liabilities amounting to $2.7 million yielding an exceptionally strong current ratio exceeding 51x—a signifier of substantial near-term solvency surpassing typical clinical-stage peers who often operate under tighter capital constraints [F1].

Management projects operational runway extending at least through December 31, 2027 based on committed capital resources without reliance on additional financing events or collaborative agreements [S6][S28]. Notably the balance sheet carries no significant debt obligations other than modest lease liabilities (~$291k) tied to right-of-use assets reported under ASC 842 accounting for office premises leases—indicative of conservative financial leverage strategy [S7].

Capital Allocation Strategy: Equity Structure, Reverse Stock Split, and Shareholder Value

Capital structure developments reflect efforts to maintain market access while managing equity dilution risks accompanying frequent fundraising rounds intrinsic to pre-revenue biotechs.

In August 2024 Monopar effectuated a reverse stock split at a ratio of one-for-five shares primarily aimed at regaining Nasdaq listing compliance after prior share price declines threatened delisting criteria [S4][S14]. This maneuver substantively reduced outstanding shares from approximately 17.6 million pre-split to about 3.52 million post-split; however did not impair existing shareholder rights or adjust par values—preserving economic ownership proportionate through proportional adjustments including rounding fractional share entitlements upward [S15].

Concurrent with this corporate action was authorization expansion of shares reserved under the amended stock incentive plan scaled post-split to approximately 1.42 million shares—demonstrating readiness for talent retention incentives aligned with R&D priorities.

There is no declared dividend policy nor share repurchases; capital returned is deferred in favor of reinvestment focused on advancing pipeline development milestones which remain pivotal given absence of meaningful commercial revenue streams at this juncture [S14][S22].

Anticipating Key Milestones: Regulatory Touchpoints and Development Readouts Ahead

While explicit forthcoming milestone dates are not delineated within recent SEC disclosures or public filings up to early April 2026 [N/A], sector norms suggest important near-term events likely center around Phase transitions or topline data reads particularly related to:

- Completion of pivotal or registrational study components for ALXN1840 supporting potential FDA submission steps.

- Dose-escalation updates or safety/efficacy signals from Phase 1a/later Phase oncologic radioligand trials (MNPR-101 series).

- Potential investigator-initiated trial results or collaborative research agreement maturities validating proprietary technology platforms.

Monitoring corporate guidance updates around these programs can offer clarity on timing of FDA engagements or Breakthrough Therapy designations which are catalytic inflection points shaping valuation trajectories within this niche therapeutic space.

Risks in Clinical Development and Funding amidst a Competitive Biopharma Landscape

As articulated in the company's formal risk disclosures [S5][S2]:

- The inherent risk demand for successful regulatory approvals cannot be overstated; setbacks in safety profile findings or demonstration of efficacy against comparator standards can stall clinical progress irreversibly.

- Financial sustainability depends significantly on continued investor appetite given protracted timelines before potential revenue generation—a common pressure point where cash burn rate must be managed prudently alongside funding round execution capability.

- Market competition within orphan disease treatment classes like Wilson disease involves established players creating barriers related to reimbursement frameworks and physician adoption patterns.

- Novel radiopharmaceuticals entail specialized manufacturing complexities along with evolving nuclear medicine commercial infrastructure that could complicate scaling post-approval supply chains.

These factors collectively reinforce need for measured optimism rooted in demonstrated operational discipline yet tempered by recognition that biotech valuation remains intimately tethered to binary pipeline outcomes beyond financial metrics alone.

Disclaimer: This report presents an analysis of Monopar Therapeutics’ financial status and development plans using publicly filed data as of April 2026 without providing investment advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments