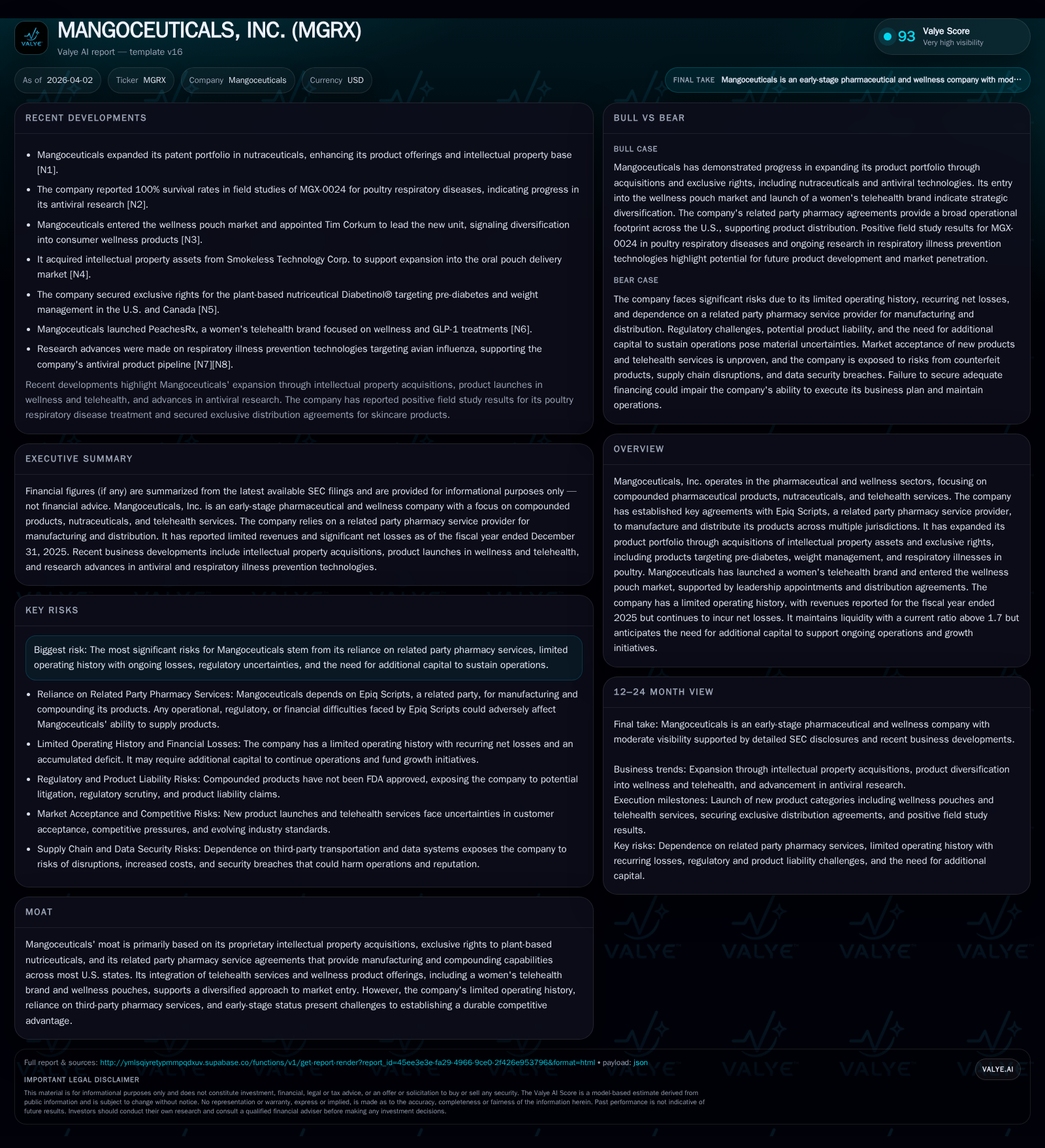

Mangoceuticals' Intellectual Property Push Amid Structural Headwinds

Mangoceuticals pursues growth through related-party pharmacy agreements and patent acquisitions yet faces mounting losses and regulatory pressures.

Mangoceuticals, Inc. continues to expand its pharmaceutical and wellness portfolio primarily via intellectual property acquisitions and exclusivity arrangements, leveraging a related-party pharmacy provider for manufacturing and distribution. Despite this strategic breadth, the company’s limited operating history is marked by declining revenues and widening operating deficits that underscore persistent financial challenges. Regulatory complexities around compounded pharmaceuticals and reliance on licensing progress add layers of uncertainty; meanwhile, liquidity remains manageable with a current ratio near 1.74 but negative cash flows deepen the cash burn profile.

Early Trajectory: Revenue Decline Against Rising Operating Deficits

Mangoceuticals’ brief operational history reveals a contraction in sales alongside markedly increasing operating losses. Revenues fell from $731,493 in FY2023 to $456,021 by FY2025—a decline of approximately 26% over two years [F1]. This descending top line contrasts sharply with an expanding operating deficit that surged from -$9.2 million in FY2023 to nearly -$18 million by the end of FY2025, doubling the rate of loss year-over-year (-126.2% YoY) [F1]. Net income followed suit with an increasingly negative trajectory, registering -$20.6 million in FY2025 compared to -$9.2 million two years prior [F1]. Operating cash flows remain negative as well, indicating fundamental cash burn from core operations that worsened by roughly 20% over the same period.

This financial pattern highlights operational challenges inherent in evolving a compound pharmaceutical business faced with limited market traction, capital constraints, and costs associated with product development and scaling efforts.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 456021 | -21 | -6 | -18 | -26.0% | -137.1% |

| 2024 | 615873 | -9 | -5 | -8 | -15.8% | +5.5% |

| 2023 | 731493 | -9 | -7 | -9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -135.8 | |

| 2024 | -5 | -62.4 |

| 2023 | -7 | -1189.1 |

Source: SEC companyfacts cache [F1].

Data sourced exclusively from SEC filings [F1]; Fiscal years end December 31.

Strategic Use of Intellectual Property and Product Acquisitions

Mangoceuticals has actively pursued growth through targeted intellectual property acquisitions concentrating on compound pharmaceutical and nutraceutical innovations. Recent announcements highlight the acquisition of patents involving plant-based compounds aimed at indications such as pre-diabetes control and weight management—segments gaining prominence amid growing chronic disease awareness [N1][S1]. Additionally, Mangoceuticals expanded into a niche agricultural market addressing respiratory illnesses in poultry through exclusive rights arrangements.

These IP transactions not only imbue Mangoceuticals with proprietary formulations that can be defended legally but also support diversification beyond traditional pharmaceutical offerings into complementary wellness domains. This portfolio development aligns with the company’s broader strategy to capitalize on compounded pharmacy product flexibility combined with emerging nutraceutical trends.

Operational Dependencies: The Role of Epiq Scripts

Central to Mangoceuticals' operating model is a Master Services Agreement (MSA) with Epiq Scripts LLC—a pharmacy services provider that holds licenses across forty-nine U.S. states plus DC but is pending licensure in Alabama [S1][S6][S7]. Epiq Scripts is controlled largely by Jacob D. Cohen, Mangoceuticals’ CEO and Chairman, representing a significant related-party relationship imbued with both synergy and governance complexity.

This arrangement grants Mangoceuticals exclusive access to specialty compounding services essential for manufacturing and distributing its pharmaceutical products sold via online channels tied to telehealth consultations [S7]. However, regulatory nuances around state-specific licensure create geographic limitations—Alabama remains a conspicuous gap—and any licensing failure or revocation could curtail sales reach abruptly.

Moreover, the MSA excludes explicit indemnity provisions concerning product liability claims; should adverse events arise linked to compounded products shipped by Epiq Scripts’ facilities, Mangoceuticals may need to initiate legal recourse to recover damages or defend claims [S6][S13]. These risks are noteworthy given the stringent regulatory environment governing compounding pharmacies.

Growth Opportunities Tied to Telehealth and Wellness Ventures

Broadening its footprint beyond compounded pharmaceuticals alone, Mangoceuticals has launched a women-focused telehealth brand coupled with entrance into the wellness pouch market targeting consumers seeking convenient health supplements [N1][S1]. Supported by recent leadership hires specifically aligned with digital health service scaling initiatives and new distribution contracts for these offerings, this pivot exemplifies an effort to diversify revenue streams through consumer-facing telemedicine platforms integrated closely with its proprietary compound formulations.

Despite these innovations and potential cross-marketing synergies between telehealth consultations and proprietary product sales under the 'MangoRx' label, the nascent stage of commercial operations manifests clearly in continued net losses and subdued revenues. Scaling these ventures profitably will require navigating competitive pressures alongside compliance challenges inherent in health service delivery models.

Regulatory and Litigation Risks Shaping Operational Dynamics

Mangoceuticals operates within a complicated regulatory framework surrounding compounded pharmaceuticals which notably lack FDA approval—a stark contrast from conventionally approved drug products subject to rigorous clinical trial validation [S4][S5]. The company asserts exemption under Section 503A of the Federal Food Drug & Cosmetic Act; however, the FDA retains authority to reclassify or restrict such exemptions potentially constraining product offerings.

Additionally, persistent litigation exposure looms due to absence of formal indemnification clauses protecting Mangoceuticals against product liability suits related to adverse patient outcomes stemming from unapproved compounded substances [S6][S14]. Legal proceedings currently pending introduce variability into future financial outcomes given uncertainties inherent in complex IP disputes and safety concerns raised about certain ingredients such as Sildenafil analogues used in their ‘Mango ED’ product line.

Furthermore, evolving federal and state privacy regulations impose operational costs necessary for compliance often without clarity on long-term interpretations—a risk compounded when telehealth activities span multiple jurisdictions each governed by their own data protection statutes such as HIPAA amendments enforced variably across states including California and Texas [S4][S9][S22].

Assessing Liquidity, Capital Allocation, and Shareholder Returns

From a capital perspective, Mangoceuticals maintains sufficient liquidity buffers with current assets of approximately $1.55 million compared against liabilities near $0.89 million yielding a current ratio around 1.74 as of FY2025 end—a metric suggesting short-term obligations are covered reasonably [F1][S26][S28]. Nevertheless, cash flow generation remains deeply negative; operating cash flow stood at roughly -$5.85 million for FY2025 while capital expenditures held static at $3.5K annually indicating negligible investment capex activity consistent with early-stage operations focused predominantly on operational scaling rather than fixed asset expansion [F1].

Return metrics highlight acute challenges: approximated return on equity based on net loss relative to shareholders’ equity was near -136% underscoring sustained capital consumption absent positive earnings contributions [F1]. There is no record of dividend distributions or share repurchases reflecting typical early venture reinvestment priorities amid losses.

These figures embody typical liquidity tradeoffs for start-up pharma enterprises where cash preservation must be balanced against fulfilling promising growth initiatives predicated on intellectual property exploitation.

What to Monitor: Upcoming Milestones and Market Inflection Points

Absent explicit forward guidance from the company, stakeholders should watch several pivotal developments shaping Mangoceuticals’ trajectory: progress towards full licensure for Epiq Scripts in Alabama will remove significant geographic barriers expanding addressable markets domestically [S7][N1]. Regulatory determinations concerning the FDA status of compounded drugs underpinning their primary product lines remain critical—they dictate permissible marketing scope fundamentally influencing revenue potential [S4][S10].

In addition, successful commercial launches under the ‘MangoRx’ brand—both pharmaceutical products backed by proprietary IP portfolios and newly established telehealth channels for women’s health services—will serve as early indicators of scalable operations beyond clinical proof-of-concept phases reported thus far.

Finally, as noted internally through strategic alternative reviews underway per recent SEC disclosures, opportunities or transactions perceived beneficial by management could materially reshape business operations or capitalization structures moving forward signaling tactical shifts responsive to market dynamics or liquidity needs [S6][S3].

This analysis reflects information available as of early April 2026 derived exclusively from official SEC filings ([F1],[S#]) and verified news sources ([N#]). It does not offer investment advice or predictions about future performance but strives to provide a detailed yet balanced understanding of Mangoceuticals’ operational model, growth strategy, and associated risks within the current regulatory environment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments