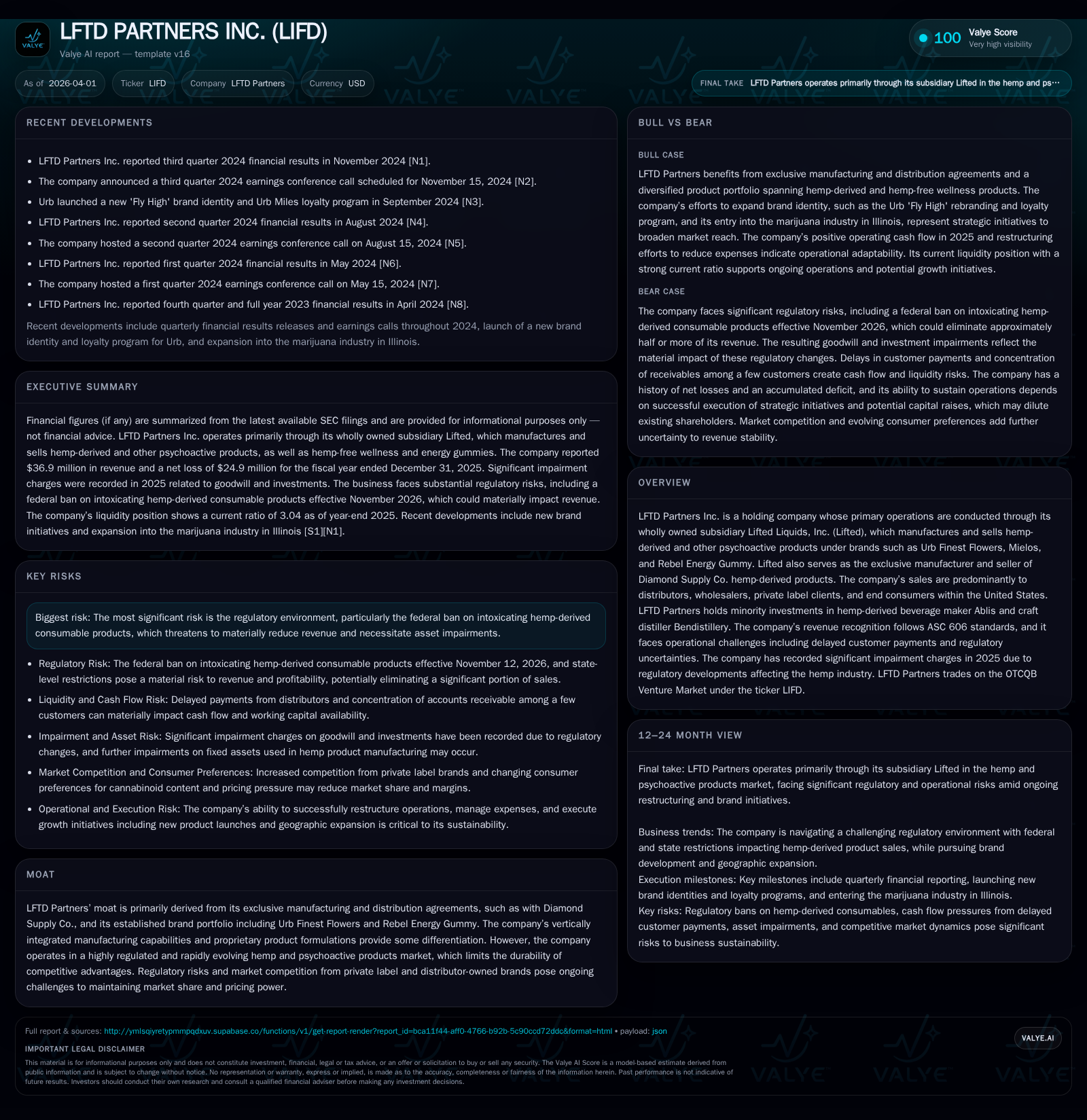

LFTD Partners Balances Revenue Stability with Impairment Pressures and Regulatory Challenges

Despite stable sales in 2025, LFTD Partners faces goodwill impairments and regulatory uncertainty threatening its core hemp-derived product business.

LFTD Partners Inc., primarily operating through its subsidiary Lifted Liquids, reported largely stable revenues near $37 million in 2025 but recorded a significant net loss driven mainly by goodwill impairments related to pending legislation banning intoxicating hemp products nationally. The company's diversified brand portfolio and exclusive manufacturing agreements underpin its market position, yet federal regulatory risks loom over half of its sales derived from hemp-based items. Operationally, LFTD contends with delayed receivables from wholesale and distributor clients, affecting cash flow, though it maintained positive operating cash flow for the year. Considerable write-downs of goodwill and investments weighed on profitability, and going forward, legislative outcomes and customer payment behaviors will be key indicators of financial health.

Company Overview

LFTD Partners Inc.'s primary business operates via its wholly owned subsidiary Lifted Liquids, which produces and markets a portfolio of hemp-derived and psychoactive products under brands such as Urb Finest Flowers, Mielos, and Rebel Energy Gummy. It holds exclusive manufacturing and distribution rights for Diamond Supply Co.’s hemp-based products. Sales are predominantly generated in the United States through distributors, wholesalers, private label arrangements, and direct consumer channels.

The company also holds minority stakes in Ablis (a hemp-derived beverage maker) and Bendistillery (a craft distillery). These investments have faced impairment pressures amid challenging industry dynamics [S1].

Historical Performance

LFTD’s revenue has trended downward since its peak in FY2022:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 37 | -25 | 1 | 1 | -1.1% | -2096109.9% |

| 2024 | 37 | 0 | -1 | -1 | -27.7% | -95.0% |

| 2023 | 52 | 0 | 1 | 2 | -10.1% | -96.1% |

| 2022 | 57 | 1 | 3 | 10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 1 | -196.8 |

| 2024 | 240240 | -1 | 0.0 |

| 2023 | 0 | 0 | 0.1 |

| 2022 | 150000 | 2 | 1.8 |

Source: SEC companyfacts cache [F1].

Revenue contracted by approximately 36% over the three-year period from FY2022 to FY2025. The dip between FY2023 to FY2024 was more pronounced (-27.7%), followed by a modest decline (-1.1%) from FY2024 to FY2025 [F1]. Operating income swung from robust profitability in earlier years to a slight positive margin of approximately $0.9 million in FY2025 after losses in FY2024.

Net losses ballooned sharply to nearly $25 million last fiscal year driven largely by substantial goodwill impairments tied to legislative developments affecting the hemp market [F1/S1].

Operating cash flows reversed prior negative trends significantly in FY2025 to generate about $1.3 million despite net losses — signaling normalized working capital management or non-cash impairment adjustments contributing favorably [F1]. Capital expenditures dropped markedly in FY2025 relative to earlier years.

Business Drivers and Segments

All revenue is generated via Lifted Liquids. No meaningful sales derive directly from other subsidiaries or equity investments like Ablis or Bendistillery [S1].

Sales channels breakdown places distributors as the majority customer base (67% of total sales), followed by wholesalers (14%) and end consumers (~12%) [S9]. Distribution customers supply vape/smoke shops and related retail outlets across the US.

In recent years Lifted acquired assets of Oculus CRS LLC enhancing product offerings but goodwill recognized during these purchases became subject to impairment given deteriorating industry outlooks post-legislation [S1/S4/S19].

Regulatory Impact & Risks

The pivotal development is the federal enactment on November 12th 2025 of H.R. 5371 which includes a national ban effective November 12th 2026 on intoxicating hemp-derived consumable products. This legislation targets a core segment representing about half Lifted's sales volume ([~52% full year; ~47% Q3 2025]) which will severely curtail revenue if it remains effective [S1/S2].

Consequences include:

- Full impairment of goodwill previously recorded on Lifted ($22+ million) and Oculus acquisitions ($800k), both written down to zero.

- Total write-offs of inventory related to banned hemp products after November 12th 2026.

- Increased allowance for doubtful accounts due to distributor/wholesaler credit difficulties leading up to enforcement date.

- Impairment losses or disposals anticipated on fixed assets primarily dedicated to hemp product manufacturing.

- Impairment of equity investment in Ablis reduced fully to zero [$399k original cost] due to unavoidable exposure [S1/S2/S16].

While there remains uncertainty regarding whether these provisions will be amended or rescinded before enforcement date via Congressional action or legal challenge—management discloses severe downside implications on revenue trajectory and asset values if ban proceeds unamended [S7/S10].

Tennessee’s state-level restrictions introduced mid-2025 also foreshadow localized revenue headwinds starting in fiscal year 2026 [S2].

Future Growth Prospects and Constraints

Potential growth drivers include leveraging exclusive manufacturing agreements like Diamond Supply Co., introducing novel cannabinoid-based formulations within regulatory constraints, expanding non-hemp psychoactive product lines like Rebel Energy Gummy portfolio across existing channels.

Conversely exposure remains significantly capped by:

- Federal legislation banning key product categories.

- Customer concentration risk given that three customers each carry more than a 10% share of accounts receivable balances.

- Persistent delayed payments from wholesale/distributor clients requiring continuous conservative credit loss provisioning impacting liquidity.

- Highly competitive market landscape involving private label manufacturers diluting pricing power.

- Residual uncertainties surrounding enforcement timelines and secondary regulations [S7/S16].

Forecasts / Milestones / Expectations

The company has not provided explicit forward revenue or profit guidance but highlights critical milestones including November 12th 2026 enforcement of federal ban as a key risk event determining viability of its hemp product lines [S2/S7]. Observers should monitor:

- Legislative developments altering the scope or enforcement of the ban.

- Quarterly trends in accounts receivable collection rates.

- Inventory write-offs as reporting periods approach prohibition implementation.

- Litigation outcomes related to ongoing lawsuits questioning product contents or representations [S7/S16].

- Any announced changes to capital structure or equity financing activities aimed at sustaining operations during transition periods [S17].

Returns & Capital Allocation

The firm shows an approximate return on equity near -197% for FY2025 reflecting large accounting impairments overshadowing underlying operations based on net income over equity figures [F1]. Despite net losses it delivered positive operating cash flow ($1.32 million) resulting in modest free cash flow (~$1.2 million after capex), suggesting some operational resiliency amid financial stress.

Dividends are nonexistent recently reflecting conservative capital preservation posture; share buybacks ceased entirely after minor repurchases ($240k) made in FY2024 [F1]. Debt facilities with Surety Bank ensure secured capital availability with relaxed covenants following partial loan paydowns during late FY2025 enhancing liquidity headroom though loan maturities extend into late 2028 [S11/S15]. The current ratio exceeds three times underscoring sufficient short-term liquidity coverage at year-end [F1].

Management contemplates sustaining the company via continuing Lifted operations alongside pursuing complementary acquisitions or developing profitable new businesses plus private placements that could dilute current shareholders but provide necessary capital infusions [S17].

Operational Challenges & Other Factors

Delayed payments from customers pose persistent risks to liquidity requiring sizable allowances for doubtful accounts currently exceeding one million dollars against trade receivables totaling about two million dollars at year-end—indicating significant credit risk exposure intertwined with industry economic conditions [S21]. The firm elects practical expedients under CECL accounting standards assuming balance sheet date conditions persist over remaining receivable lives while updating allowances conservatively based on trailing historical loss rates [S14/S21].

Recent cybersecurity incidents involving theft of digital cash equivalents highlight additional operational vulnerabilities though reportedly promptly addressed with law enforcement involvement [S4].

Legal disputes generally seem managed with dismissals or amicable settlements except two ongoing lawsuits targeting alleged misrepresentation or product compliance matters that remain appealable [S7/S16/S18]. These represent cost exposures but do not appear imminently threatening solvency at present.

Industry Context (Analysis)

The hemp-derived cannabinoid product sector is highly fragmented with intense competition among vertically integrated producers competing on both branded specialist formulations and white-label supply agreements. Regulatory volatility remains paramount limiting institutional capital inflows relative to other wellness fields and pressuring margins via complex state-by-state licensing requirements alongside emerging federal statutes restricting specific forms such as intoxicating consumables. Companies must balance aggressive innovation with compliance vigilance while managing distributor networks who often receive extended payment terms—challenging working capital management innate complexities common within cannabis-adjacent markets.

Summary Table: Key Financial Data — LFTD Partners Inc.

| Metric | FY2025 | FY2024 | FY2023 |

|---|---|---|---|

| Revenue | $36.92M | $37.33M | $51.61M |

| Operating Income | $913K | $(773K) | $2.41M |

| Net Income | $(24.86M) | $1K | $24K |

| Operating Cash Flow | $1.32M | $(960K) | $639K |

| Capex | $122K | $314K | $790K |

| Buybacks | $0 | $240K | $0 |

Results show decline since peak levels driven mainly by impairments linked to regulatory changes impacting core hemp-derived consumable products.

This analysis synthesizes publicly filed financial disclosures for LFTD Partners Inc., highlighting material factors shaping the company’s performance including recent legislative-induced challenges affecting its main operating subsidiary Lifted Liquids’ core business lines. The evolving regulatory environment underscores significant downside risks while operational execution around collections and cost control remains critical near-term priorities.

Disclaimer: This report presents factual analysis based on SEC filings dated up to April 1st 2026 without providing any investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments