Scientific Industries Navigates Revenue Decline and Operating Losses Amid Strategic Shift to Bioprocessing

A legacy laboratory equipment manufacturer faces financial challenges as it invests in emerging bioprocessing technologies and restructures its product portfolio.

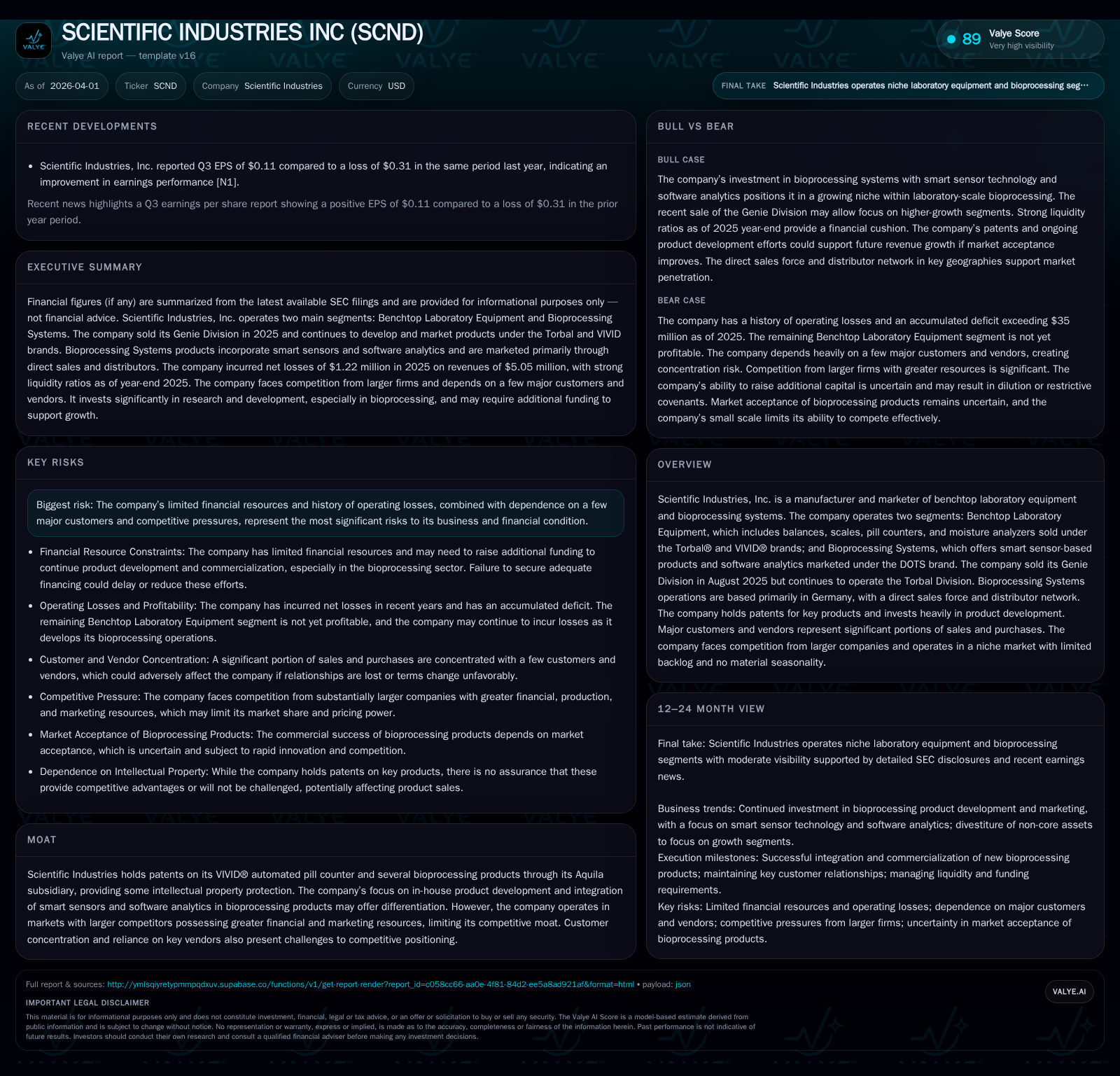

Scientific Industries, Inc. experienced a revenue decline from $10.7 million in 2024 to $5.05 million in 2025 primarily due to the divestiture of its Genie division. Operating losses expanded to $7.9 million driven by sustained research and development expenses focused on bioprocessing systems. The company’s pivot towards higher-technology bioprocessing products, leveraging smart sensors and software analytics through its Aquila subsidiary, remains early-stage and capital intensive. Customer concentration risks and supply chain dependencies persist, while the firm must secure additional financing to support ongoing product development and commercialization efforts.

Company Background and Segment Overview

Scientific Industries, Inc., incorporated in 1954, operates two main segments: Benchtop Laboratory Equipment and Bioprocessing Systems [S1][S4]. The Benchtop segment produces balances, scales, moisture analyzers, and automated pill counters marketed under Torbal® and VIVID® brands. The Bioprocessing segment develops advanced products incorporating smart sensors and software analytics through its wholly owned German subsidiary Aquila Biolabs GmbH [S1][S6].

In August 2025, the company sold its Genie division (part of Benchtop Laboratory Equipment) to Troemner LLC for approximately $9.6 million plus earn-out provisions [S1][S17]. This divestiture contributed significantly to a revenue decline from $10.7 million in 2024 to $5.05 million in 2025 as reported [F1]. The remaining Benchtop operations focus on Torbal scales and VIVID automated pill counters.

Historical Performance Overview

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5 | -1 | -8 | -52.8% | +81.1% | |

| 2024 | 11 | -6 | -4 | -7 | -3.6% | +29.1% |

| 2023 | 11 | -9 | -6 | -9 | -2.5% | -61.0% |

| 2022 | 11 | -6 | -6 | -7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -11.4 | |

| 2024 | -4 | -70.7 |

| 2023 | -6 | -65.4 |

| 2022 | -6 | -22.1 |

Source: SEC companyfacts cache [F1].

Source: [F1]

The table illustrates a substantial revenue contraction following the Genie division sale, alongside increased operating losses despite reduced scale—primarily attributable to heavy R&D spending on bioprocessing products [S17][F1]. Net losses improved year-over-year but remain significant.

Operating cash flows have been negative consistently, reflecting substantial investment outlays amid slower revenue recognition from newer bioprocessing offerings [F1][S20]. Capital expenditures decreased markedly post-divestiture but continue to support production capabilities.

Growth Outlook

Scientific Industries aims to grow through its Bioprocessing Systems segment by expanding sales of proprietary smart sensor devices and analytical software solutions targeting laboratory-scale markets [S4][S20]. Patents protecting these technologies expire predominantly between 2036 and 2039 [S7], affording some competitive advantage.

The VIVID automated pill counter line continues incremental development with recent product launches aimed at pharmacy automation improvements [S4][S20]. However, competition remains intense for Benchtop Laboratory Equipment against larger established companies such as Ohaus Corporation and A&D Company Ltd., limiting pricing flexibility [S11].

Geographically, international sales represent approximately one-fifth of revenues with exposure to currency fluctuations impacting reported results due to Euro-Dollar exchange rate volatility [S5][S6]. Customer concentration risk persists as one key customer accounted for roughly 31% of consolidated revenues in FY2025 [S4][S11].

Financial Milestones and Expectations

While explicit guidance is not provided, critical milestones include:

- Commercial ramp-up of bioprocessing products integrating sensor platforms.

- Retention or growth of key customer contracts supporting VIVID product sales.

- Progress toward operating leverage through scalable manufacturing.

- Movement toward positive operating income amidst ongoing R&D investments.

- Raising sufficient capital to sustain development activities [N/A forecast].

Management projects continued material R&D expenditures in FY2026 focused on enhancing bioprocessing systems [S17][S19]. Challenges include extended beta testing periods, absence of FDA regulatory approval requirements but competitive pricing pressures remain salient risks [S18][S20].

Capital Allocation and Returns Analysis

Scientific Industries reported operating losses nearing $7.9 million in FY2025 and negative free cash flow estimated at approximately $3.75 million (operating cash flow less capex), indicating ongoing investment exceeding current returns [F1]. Return on equity based on latest net income versus equity approximates -11%, evidencing value erosion currently.

No recent dividends or share repurchases have been disclosed; available capital appears dedicated to sustaining R&D and operational liquidity amid constrained resources [F1][S27–29]. The company holds a strong current ratio (7.7) with current assets far exceeding liabilities; however, cash balances were modest ($515 thousand as of September 2023), underscoring liquidity pressures requiring external financing [F1][S9].

Management acknowledges limited financial resources necessitating potential equity or debt raises that may dilute shareholders or impose restrictive covenants [S1][S9][S21]. This financial profile reflects typical constraints for niche players balancing innovation investments against nascent revenue streams.

Industry Context and Risks

Operating within specialized scientific instrumentation markets dominated by larger competitors with more extensive resources constrains Scientific Industries’ market penetration potential [S11]. The bioprocessing sector’s emphasis on integrating IoT-style sensors with advanced analytics aligns with broader life sciences trends but demands continuous innovation amid rapid technological evolution.

Supply chain vulnerabilities exist due to reliance on single-source suppliers for critical components manufactured overseas, exposing operations to lead-time delays, tariff impacts, and cost pressures that may compress margins if not passed through pricing [S10].

Key risks outlined include:

- Sustained operating losses with uncertain timeline for bioprocessing commercial success [S18]

- Revenue volatility due to dependence on a concentrated customer base [S4][S11]

- Competitive disadvantage relative to larger multinational firms especially internationally [S11]

- Intellectual property challenges outside core patented products potentially enabling competitor design-arounds [S10][S22]

- Funding risks heightening refinancing needs amid prior financial performance; failure to secure capital would impair strategic initiatives [S1][S9]

- Operational complexities from geographic dispersion including foreign exchange risks related to German operations versus predominantly USD revenues [S5][S21]

- Talent recruitment and retention challenges affecting critical technical roles essential for bioprocessing innovation efforts [S23]

Conclusion

Scientific Industries is undergoing a pivotal transition from legacy benchtop laboratory instruments toward technologically sophisticated bioprocessing solutions leveraging smart sensor technology combined with software analytics developed via acquisitions such as Aquila Biolabs GmbH.

This strategic shift aligns with emerging life sciences research trends yet coincides with adverse financial dynamics including sharp revenue declines post-divestiture, expanding operating losses driven by heavy R&D investments, negative cash flows necessitating capital raises likely dilutive or debt-funded, concentrated customer base risks, and competitive pressures from larger global players.

Until commercialization efforts yield meaningful revenues offsetting investment costs, Scientific Industries will remain financially constrained with limited operational flexibility.

This analysis is based exclusively on publicly available SEC filings including recent Form 10-K annual reports complemented by companyfacts numeric data extracts as of early 2026 along with internal disclosures regarding business operations, strategic initiatives, risk factors, segment performance data from subsidiaries like Aquila Biolabs GmbH located in Germany plus recent corporate divestitures impacting revenue streams.

It does not constitute investment advice but provides comprehensive industry-aligned context for institutional research purposes focused on operational performance trends and strategic positioning within scientific instrumentation sectors undergoing innovation cycles.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments