SES S.A. Expands Satellite Reach with Multi-Orbit Strategy Amid Investment and Competitive Pressures

SES leverages its GEO-MEO-LEO satellite blend and recent acquisitions to grow revenue but faces margin and credit rating challenges.

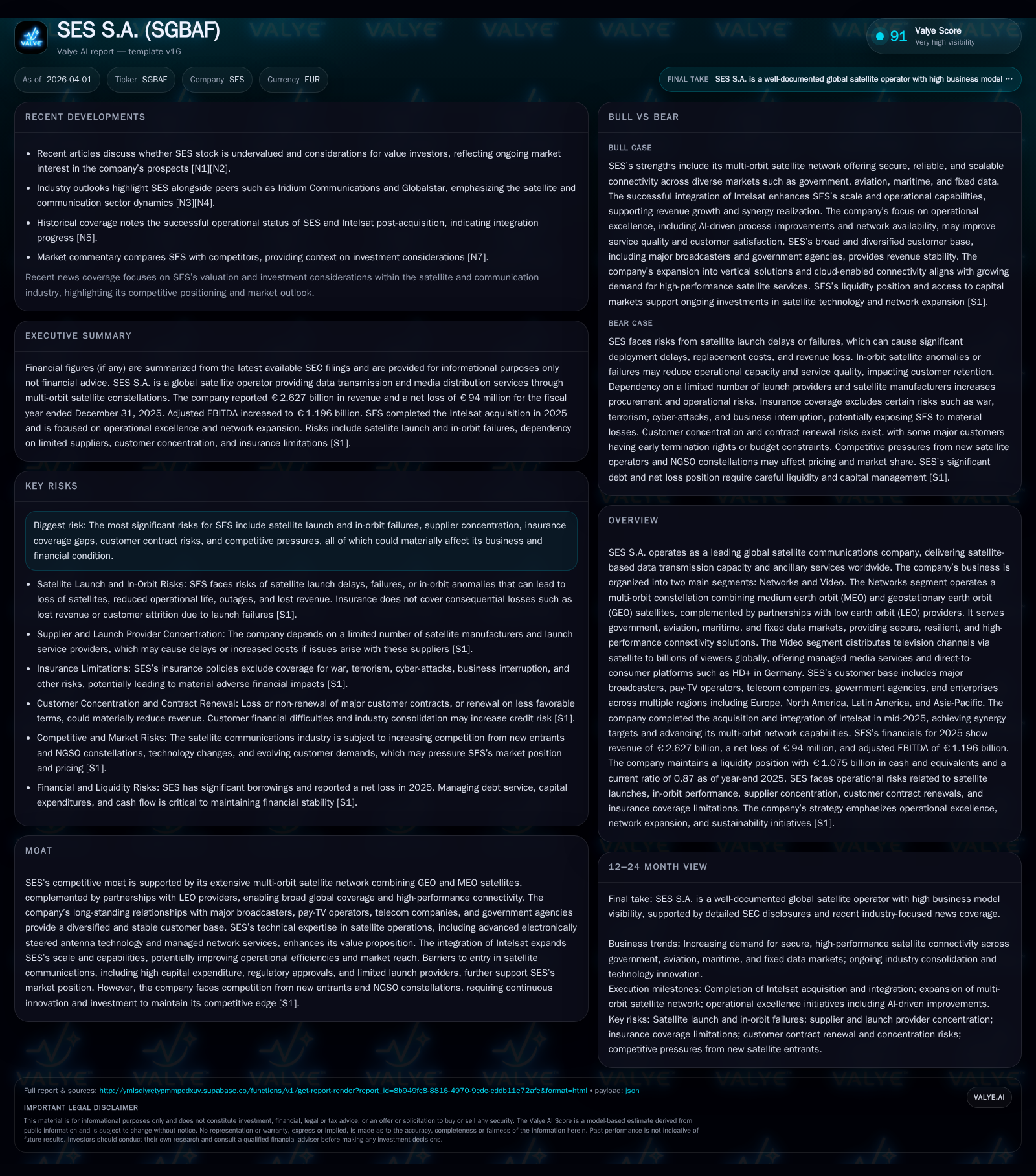

SES S.A. reported €2.63 billion in revenue for 2025, up from €2.00 billion in 2024, driven by integration of Intelsat and expansion in Networks and Video segments. The company maintains a diversified global customer base without customer revenue concentration over 10%. Despite top-line growth, SES posted a net loss of €94 million and saw adjusted EBITDA margin contract to 45.4%. Heavy capital expenditures and substantial debt raise liquidity and credit rating concerns, including a Moody’s downgrade to Ba1. Strategic focus on hybrid satellite constellations and value-added services aims to sustain growth amid intensified competition from LEO constellations and commoditization pressures.

Historical Performance

SES S.A., a leading global satellite communications company primarily organized into Networks and Video segments, has demonstrated top-line expansion driven by strategic acquisitions and multi-orbit network development. Revenue grew significantly from around €2.0 billion in 2024 to €2.63 billion in 2025 [F1], reflecting the contribution from the Intelsat acquisition completed during this period as well as organic growth across established markets.

However, this revenue growth masks profitability pressures; while adjusted EBITDA rose to approximately €1.20 billion in 2025 from about €1.03 billion in 2024, EBITDA margin compressed notably from 51.4% to 45.4% [S17][F1]. This deterioration reflects competitive pricing dynamics within traditional GEO/MEO capacity markets coupled with the growing emphasis on value-added services which tend to carry lower margins [S22]. SES recorded a net loss of €94 million in 2025 resulting in a negative ROE of about -3.5%, underscoring underlying earnings challenges despite operational scale [F1].

The following table summarizes SES’s key financial indicators over the last three years:

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: Cash flow from operations (CFO) and capital expenditure (Capex) details are not explicitly available but dividend payments and share buyback programs are documented [S11][S15][S21].

Business Segments and Market Position

SES operates two main business segments:

Networks: Focuses on data transmission via an integrated multi-orbit constellation combining MEO (notably O3b mPOWER satellites) alongside traditional GEO satellites; it serves diverse sectors including government/military secure communications, aviation, maritime mobility solutions, fixed data networks, telecom backhaul for expanding mobile services (e.g., for rural broadband or emerging markets), cloud access enhancement, and enterprise networks [S4][S28]. Partnerships with LEO providers supplement SES’s capabilities especially under its Infrastructure for Resilience Interconnectivity Secure Satellite (IRIS²) program.

Video: Delivers linear video broadcasting services globally through satellite distribution reaching billions of viewers via direct-to-home (DTH), direct-to-cable (DTC), IPTV platforms including proprietary platforms like HD+ in Germany serving around two million paid subscribers [S23]. This unit also offers managed media services such as channel playout automation and live sports/event distribution supporting major rights holders.

The company benefits from longstanding relationships with major broadcasters (e.g., Sky, Warner Brothers Discovery), pay-TV operators (Canal+, ProsiebenSat.1), telecom companies (Telefonica), government agencies across multiple regions as well as newspace entrants [S23][S28]. No single customer accounts for over 10% of revenue indicating relatively diversified cash flow sources [S18].

Future Growth Prospects

Growth momentum relies on both organic expansion within SES’s traditional markets as well as leveraging its enhanced scale from the Intelsat acquisition completed in mid-2024 which expanded fleet size, orbital slots access, and customer breadth [S8][S9]. Demand drivers include:

- Increasing global demand for secure, resilient high-performance connectivity including defense/government applications amid geopolitical tensions pushing higher satellite adoption (ISR missions require robust comms) [S4].

- Expansion of mobility markets such as commercial aviation & maritime which demand consistent broadband connectivity powered by MEO/GEO hybrids [S28].

- Telecom operator upgrades targeting underserved areas using satellite backhaul for fixed wireless access (connectivity rollouts supporting 4G/5G expansions especially in developing regions) [S28].

- Growing video distribution needs including premium live events broadcasting demand coupled with OTT convergence fueling managed service offerings [S23].

Nonetheless, barriers exist that could cap growth:

- Pricing pressure triggered by rising competition from advanced LEO constellations that offer low latency albeit with challenges such as session instability due to fast-moving satellites causing handover concerns particularly for enterprise/government clients requiring very stable connections [S18].

- Budget constraints impacting governmental customer renewals or contract scopes impose risks on predictable revenue streams [S6][S19].

- Execution risk related to ambitious ongoing programs like IRIS² involving complex consortiums with potential funding or regulatory hurdles [S22].

Capital Allocation & Financial Health

SES maintains rigorous capital deployment towards sustaining satellite infrastructure — satellite manufacturing/launch cycles typically span around three years necessitating continual investment for replacement and new capacity provision [S26]. Capital expenditures have fluctuated between approximately €400 million to over €1 billion annually recently due largely to satellite procurements including O3b mPOWER systems; forecasts suggest steady annual capex near €325 million excluding new IRIS² spending post-2025 [S11][S26].

Debt levels have grown markedly following the Intelsat acquisition financing totaling roughly €6.3 billion at year-end 2025 compared to roughly €4.5 billion at end-2024 [F1][S16]. The weighted average senior debt maturity is about five years with interest costs averaging near 4%, reflecting a modest step-up from prior years [S9][S15]. Moody’s downgraded SES’s long-term corporate family rating from Baa3 to Ba1 citing leverage increase linked to acquisition-related debt alongside industry risks but assigned a stable outlook overall [S14].

Liquidity remains strong with cash & equivalents north of €1 billion plus undrawn revolving credit lines exceeding €1.2 billion providing ready funding sources alongside committed EIB facilities totalling several hundreds of millions [F1][S9][S15]. Dividend policy remains stable/progressive with annual payouts documented at roughly €207 million in dividends paid during 2025 even amid earnings volatility last year [S21]. A share buyback program has been active since mid-2023 totaling about €150 million invested through late-2025 aimed at reducing outstanding shares [S11][S21].

Industry Dynamics & Risks

The evolving satellite sector is marked by significant shifts featuring new space entrants offering innovative LEO constellations creating alternative data transmission options that appeal strongly to consumer markets seeking low latency but often fall short on robustness for enterprise/government uses requiring secure continuous connections . SES’s strategy leverages its integrated multi-orbit approach combining GEO stability with MEO capacity enhanced by select LEO partnerships acting as a hybrid model aiming at optimal reach/performance tradeoffs.

Key risks outlined include launch or in-orbit satellite failures which could impair service availability given reliance on expensive bespoke equipment; concentration amongst critical suppliers exacerbating supply chain vulnerabilities; insurance shortfalls potentially exposing financial losses; customer counterparty credit risks heightened if contractual counterparties falter financially especially in emerging economies; regulatory compliance challenges spanning export controls/sanctions potentially constraining operations internationally; competition law scrutiny notably dominant market positions imposing restrictions; pricing pressures related to commoditization trends; geopolitical factors affecting defense/governmental demand; all combining into a delicate operating environment requiring vigilant risk mitigation programs by SES management [S7][S16][S20].

What To Watch Next

Absent explicit company guidance beyond public disclosures, key milestones will hinge on successful rollout and commercial uptake of IRIS² capabilities, integration synergies realization post-Intelsat acquisition especially regarding cost optimization and cross-selling into expanded markets; renewal rates of large government contracts vulnerable to budget scrutiny; further development or changes in competitive positioning versus new LEO constellations; leverage metrics stabilizing or improving relative to EBITDA; achievement of anticipated margin improvement through scaling value-added services without excessive cost expansion; management responses to evolving regulatory environments particularly related to licensing and export controls.

Disclaimer

This analysis is based on information available as of April 1, 2026. It does not constitute investment advice or recommendations but provides an independent review grounded strictly in SEC filings ([F1],[S#]) without speculative assumptions beyond stated company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments