Indigo Acquisition Corp. Charts Its Path From SPAC Formation to Value Creation

An incisive look into Indigo Acquisition Corp.’s establishment, financial underpinnings, and strategic outlook as it pursues its inaugural business combination.

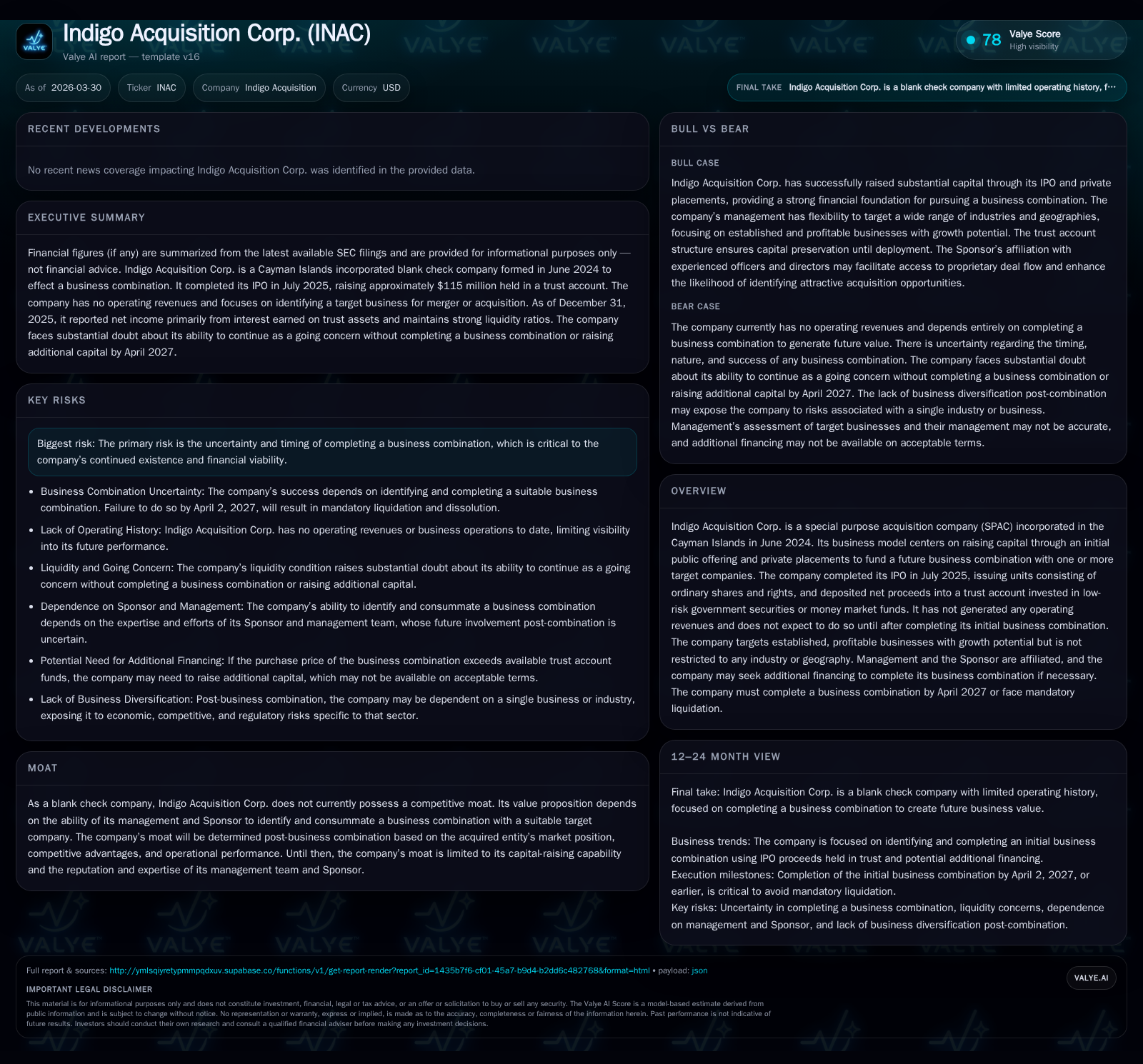

Indigo Acquisition Corp. is a newly formed special purpose acquisition company (SPAC) that completed its IPO in mid-2025, raising substantial capital earmarked exclusively for a future business combination. Since inception, the company has generated no operating revenues and remains focused on deploying its capital in a high-quality target acquisition across industries or geographies. Key financial metrics highlight strong liquidity retained in a trust account, alongside typical pre-combination expenses and share-based compensation. The critical path forward hinges on accomplishing a business combination before April 2027 to avoid liquidation, with capital structure details emphasizing Sponsor influence and redemption mechanics designed to protect public shareholders.

From Inception to IPO: Establishing a Financial Foundation

Indigo Acquisition Corp. was incorporated on June 7, 2024, as an exempted Cayman Islands company formed specifically as a blank check entity aiming to complete one or more mergers, asset acquisitions, or similar business combinations [S1]. The management team and Sponsor are affiliated entities aligned in the deployment of raised capital toward strategic acquisition targets.

The company consummated its initial public offering (IPO) on July 2, 2025, issuing 10 million Units priced at $10 each, generating gross proceeds of $100 million [S1][S2]. Each Unit comprises one ordinary share plus one accompanying right to receive one-tenth of an ordinary share upon successful completion of the initial business combination. Concurrently, it issued 350,000 Private Placement Units at the same unit price for an additional $3.5 million gross proceeds largely purchased by the Sponsor and EarlyBirdCapital’s affiliate (EBC) [S1][S7]. On July 11, 2025, the underwriters exercised their full over-allotment option resulting in the issue of an additional 1.5 million Units plus a small number of Private Placement Units totaling $15.3 million gross proceeds [S1][S19]. After underwriting fees ($2.3 million cash paid + $4.025 million deferred) and other offering costs ($416k), the company deposited approximately $115 million into a Trust Account [S1][S7].

This Trust Account holds cash and cash equivalents invested primarily in U.S. Treasury Bills maturing within 185 days or less or government-backed money market funds meeting SEC Rule 2a-7 criteria [S1][S11]. The segregation of IPO proceeds into this Trust Account is explicit SPAC structuring aiming at investor protection until deployment for an acquisition.

Operational Snapshot: Preliminary Activity and Cost Structure

As a SPAC devoid of operational businesses prior to the initial business combination, Indigo Acquisition Corp. has generated no operating revenues since inception through December 31, 2025 [S1]. Its net income reported for calendar year 2025 was $1.82 million driven predominantly by $2.3 million in interest income earned on the Trust Account securities balanced against operating expenses including formation costs ($368k), share-based compensation expense ($108k), and other administrative outlays [F1][S1]. For comparison, its brief operational period from incorporation mid-2024 through year-end resulted in a slight net loss of approximately $18.7k attributed almost entirely to formation expenditures.

Cash flow from operations reflected outflows consistent with these overhead activities: negative approximately $476k in full-year 2025 excluding investing inflows from the Trust Account interest accrual [F1]. These expense profiles align with typical public company compliance requirements such as legal filings, audits, financial reporting obligations and target due diligence efforts intrinsic to SPAC lifecycle stages prior to identifying an acquisition candidate.

Capital Structure and Trust Account Management

From a liquidity standpoint, current assets stood at roughly $760k versus current liabilities near $84k as of December 31, 2025 [F1], implying a robust current ratio exceeding nine times safety margin indicative mostly of liquid funds excluding trust investments explicitly held off-balance sheet outside working capital [S27]. These current liabilities entail routine accrued expenses including monthly administrative fees (around $10k/month) payable until either an acquisition occurs or liquidation is mandated [S5].

The capital structure comprises Ordinary Shares issued through IPO Units and Private Placement Units with Founder Shares held by Sponsor entities transferred from EBC Holdings at nominal cost near $0.002 per share underpinning Sponsor alignment [S1]. The Founder Shares carry restrictions such as waived redemption rights protecting public investors from dilution risk prior to transactional completion [S9][S16].

Redemption mechanics permit holders of Public Shares to redeem some or all shares at approximately $10 per share from Trust Account funds upon shareholder vote approving any proposed Business Combination or via tender offer settlement — ensuring liquidity alternatives that tether investor downside directly to IPO proceeds plus accrued interest [S11][S13]. Rights attached to each Unit offer fractional share consideration (“one-tenth ordinary share”) convertible only on consummation of the initial Business Combination; if unsuccessful by deadline these Rights expire worthless providing zero residual claim value [S6].

Growth Prospects Anchored on the Pending Business Combination

By design, Indigo Acquisition Corp.'s growth prospects depend exclusively on executing its initial business combination – currently targeted before April 2, 2027 — when failure triggers mandatory liquidation of assets held in trust and dissolution [S5]. Until then, no operating revenues exist nor are anticipated.

The Sponsor articulates an investment thesis focused on acquiring established profitable businesses demonstrating compelling growth potential without restrictions by sector or geography [S10]. This flexible mandate reflects broad market opportunity seeking with emphasis on enterprises possessing scalable operations that can leverage management’s expertise post-acquisition.

Prospective use of PIPE financing remains a possibility if purchase price exceeds available trust funds net of redemptions; this would supplement transaction funding alongside equity considerations from de-SPAC transaction structures [S10]. No working capital loans were outstanding as of latest filings though up to $1.5 million may be drawn with conversion features allowing issuance of private placement units post-combination if needed [S22].

Critical Risks and Regulatory Considerations

The paramount risk centers on Indigo’s inability or delay in consummating a suitable Business Combination within the defined statutory timeframe ending April 2, 2027 [S4][S26][S5]. This deadline places existential pressure on management's search efforts; any failure mandates liquidation distributing pro-rata amounts back to public shareholders with no residual operational enterprise value.

This timing constraint creates substantial doubt about going concern status acknowledged explicitly by management given lack of alternative revenue streams outside trust-generated interest income [S5]. Corporate governance provisions bind the Sponsor by waivers related to redemption rights for Founder Shares while regulatory compliance mandates transparent disclosure obligations throughout due diligence phases.

Legal risk exposure remains minimal with no material litigation pending against the company or its officers cited as of filing date March 26, 2026 [S4]. Contingent creditor claims could potentially reduce anticipated redemption values but are not currently material based on disclosures.

Historical Financial Summary

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: Net income includes interest earned on Trust Account securities offset by formation/operating costs; cash flows reflect operating expense outlays exclusive of investing returns.

Capital Allocation Philosophy and Investor Returns

Indigo’s capital allocation reflects typical SPAC economics where no dividends or stock repurchases occur until after completing a de-SPAC transaction given absence of operating cash flows [F1][S9][S16]. The Sponsor holds Founder Shares which provide economic incentive commonly known as 'promote' — this equity stake entails dilution risk but aligns interests toward successful closing and post-combination value accretion.

Financial stewardship focuses predominantly on safeguarding IPO proceeds within conservative low-risk investments earning modest but stable interest income augmented partially by deferred underwriting fee structures affecting initial net proceeds calculation [S19]. Current approximate negative return on equity (~ -54.8%) reveals inherent inefficiency attributable wholly to pre-revenue stage; this will normalize only upon earning profits following integration post-Business Combination completion [F1].

Given these design parameters stakeholders should regard value realization pathways dependent almost entirely on successful identification and consummation of attractive targets along with prudent post-merger integration rather than conventional dividend yield or buyback metrics common among operational enterprises.

This analysis encapsulates Indigo Acquisition Corp.’s trajectory as a newly minted SPAC navigating private capital formation protocols while positioning toward eventual de-SPAC execution subject to stringent timing constraints inherent in blank check companies. It integrates nuanced attention to governance safeguards embedded within sponsor-shareholder dynamics alongside comprehensive overview of financial substrate reflective only of early-stage organizational development consistent with regulatory framework governing such vehicles.

Disclaimer: This report is informational only and does not constitute investment advice or solicitation regarding Indigo Acquisition Corp., its securities or associated transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments