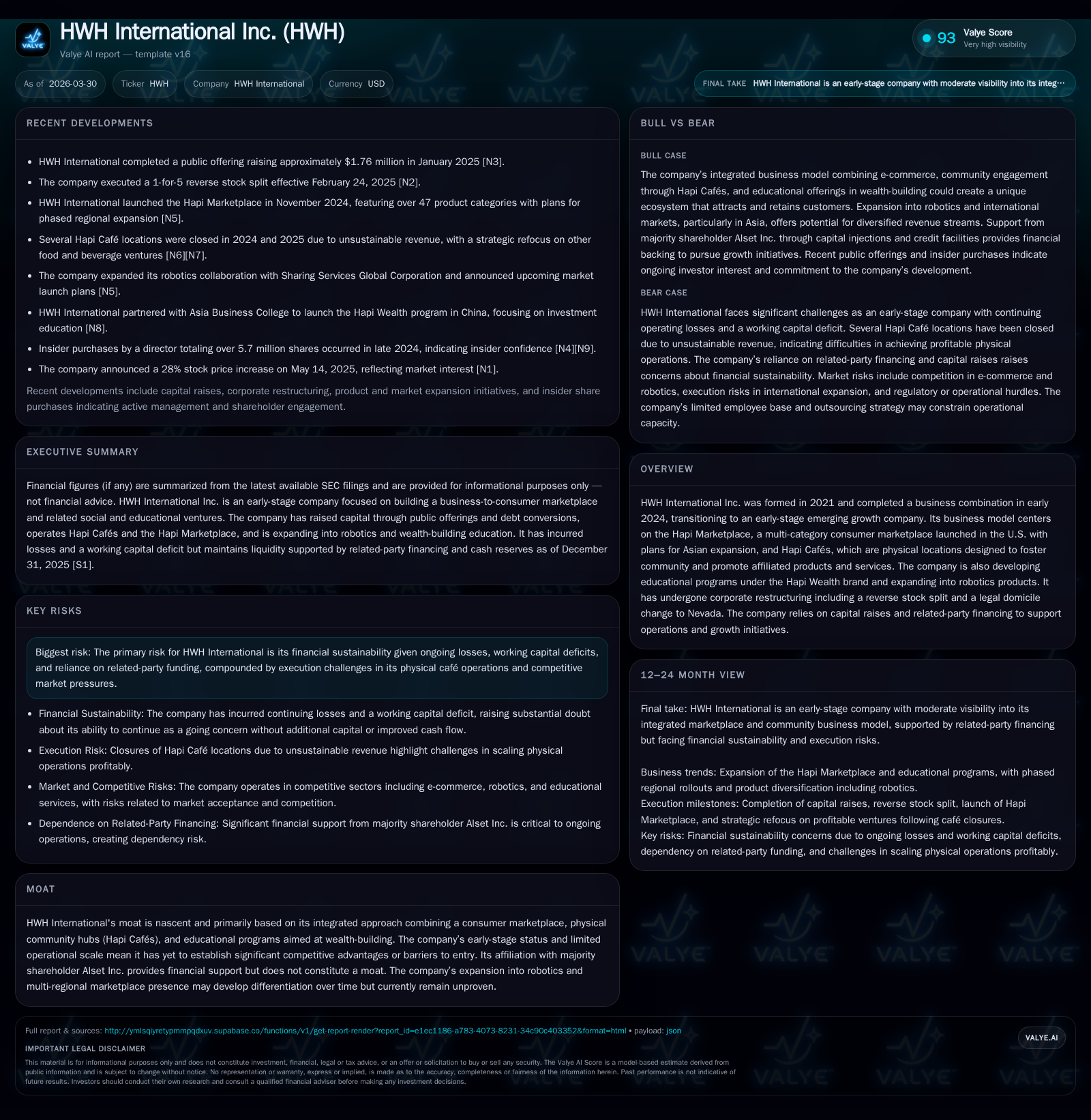

HWH International Inc. Faces Growth and Liquidity Challenges Managing Multi-Category Marketplace and Café Ventures

Emerging growth company balances expansion into online marketplaces, physical cafés, and educational services amid ongoing losses and funding reliance.

HWH International Inc., established in 2021 and publicly listed in early 2024, operates an evolving business model focused on the Hapi Marketplace and community-oriented Hapi Cafés. Despite launching its consumer marketplace with diverse categories, revenue remains minimal at under $1 million in 2025, while the company endures consistent net losses exceeding $2.6 million annually. Cash flow deficits and working capital shortfalls persist, mitigated primarily through related-party financing from majority owner Alset Inc. The firm’s ambitious plans include geographic expansions in Asia, educational programs under 'Hapi Wealth,' and robotics product lines, yet progress in these areas is nascent and fraught with execution risks. Capital raises and debt-to-equity conversions underpin financial operations currently, with no dividend or buyback programs reported.

Company Background and Historical Performance

HWH International Inc. was incorporated in Delaware on October 20, 2021, originally under the name Alset Capital Acquisition Corp., structured to effectuate a business combination which was consummated on January 9, 2024. Post-merger, it adopted its current name and began trading on the Nasdaq Global Market [S1]. It is recognized as an early-stage emerging growth entity facing typical developmental challenges.

The company's primary operational model centers around three pillars: the Hapi Marketplace, a U.S.-launched multi-category consumer marketplace including wellness, elderly care products, automotive accessories among over forty-seven product categories; physical Hapi Cafés designed as social venues intended to stimulate community engagement and drive awareness of affiliated offerings; and educational programming in wealth-building strategies branded as Hapi Wealth [S6][S12]. Plans for geographic expansion mainly target Asian markets including South Korea and Hong Kong.

From a financial perspective ([F1]), revenue generation remains embryonic with reported revenues of approximately $866,926 for fiscal year ended December 31, 2025 (FY2025). This reflects limited market traction since the platform launch was announced only in November 2024 [S6], combined with closures of some café locations due to underperformance [S12].

Net income has consecutively recorded losses exceeding $2.5 million in both FY2024 and FY2025 (-$2,590,731 and -$2,630,620 respectively), following modest profitability before public listing [F1]. These losses underscore ongoing scale-up expenses outpacing top-line growth.

Operating cash flow remains negative (-$1.75 million in FY2025), consistent with continued investment outlays required to foster marketplace development, café rollouts, and new product lines including robotics which had not launched by end-2025 [F1][S6]. Capital expenditures have been relatively low at approximately $19,464 in FY2025 compared to prior periods.

Key financial data summary:

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -3 | -1750290 | 19464 | -1.5% |

| 2024 | -3 | -1659999 | 30394 | -572.0% |

| 2023 | 1 | -1519474 | +383.4% | |

| 2022 | 0 | -514071 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($) | ROE% |

|---|---|---|---|

| 2025 | 21 | -1769754 | -100.4 |

| 2024 | 21 | -1690393 | -93.7 |

| 2023 | 68 | -23.3 | |

| 2022 | -5.6 |

Source: SEC companyfacts cache [F1].

- Full revenue data for FY2024 not disclosed explicitly but inferred minimal given early commercial stage.

The working capital situation exhibits some strain with a deficit reported (~$1.69 million) though the company maintains a current ratio of about 2.3x driven by short-term asset composition [F1][S4].

Future Growth Prospects

HWH’s growth strategy leans heavily on expanding the footprint of its marketplace beyond the U.S., rolling out phased implementations tailored by regional logistics such as payment gateways, licenses, banking relationships necessary for operation overseas notably South Korea and Hong Kong first [S1][S6]. However, concrete timelines remain fluid influenced by regulatory approvals and managerial bandwidth.

Expanding product lines into robotics aims at tapping nascent consumer/commercial demand segments yet this remains pre-launch as of late-2025 reporting [S6]. The company’s physical café concept has encountered execution obstacles evidenced by closures across Singapore and Korea operations which management attributes to unsustainable revenues warranting strategic realignment toward ventures with better growth profiles within their Food & Beverage verticals [S12].

Additionally, the planned launch of education programs targeting equity investment skills under Hapi Wealth during late-2026 could create incremental recurring revenue streams if successfully adopted by target demographics [S10]. The opening of a China-based headquarters for these initiatives emphasizes commitment but adds complexity.

Risk-wise, continuous net losses paired with working capital deficits raise execution risk compounded by dependency on related-party funding to bridge financing gaps [S9][S13]. Customer acquisition costs within competitive e-commerce spaces alongside consumer brand building for cafés amplify these uncertainties.

Forecasts And Key Milestones To Monitor (Analysis)

Explicit guidance or formal milestone schedules beyond announced launches are sparse publicly. Market watchers should focus on:

- Progress on implementing payment gateways and licenses facilitating international expansion;

- Revenue ramp trends from newly opened or reopened Hapi Cafés corresponding to growing customer base claims;

- Adoption metrics from Hapi Wealth educational program launch staged for late-2026;

- Development pace and initial sales reports from robotics product introductions;

- Reduction in operating losses or stabilization of cash burn signaling nascent scalability.

Returns And Capital Allocation

The company's return on equity has been negative near -100% due to persistent net losses relative to modest positive equity levels near $2.62 million at end-2025 [F1]. Operating cash flows consistently run negative reflecting ongoing investments exceeding operational inflows.

Capital allocation has been shaped heavily by external funding initiatives rather than internal generation. Noteworthy actions include:

- Multiple rounds of stock issuance including a public offering raising gross proceeds around $1.76 million early in 2025 post reverse stock split which adjusted share counts upwards materially [S1];

- Debt-to-equity conversions converting approximately $3.8 million of debt held by related parties into common stock shares increasing ownership dilution while reducing liabilities [S4][S8];

- Access to a $1 million unutilized credit facility from majority shareholder Alset Inc., along with binding letters of financial support ensuring at least twelve months coverage even if operating cash flows remain negative [S4][S7];

- No declared dividends or active share repurchase programs recently indicating focus on liquidity retention amid growth phase [F1][S10].

Corporate Developments And Governance Context

A significant corporate restructuring occurred mid-2025 when the Delaware parent merged into its Nevada subsidiary establishing Nevada as the legal domicile effective November 14, 2025 without operational disruptions but potentially positioning governance improvements or regulatory considerations [S1][S11][S29].

Executive leadership includes CEO Chan Heng Fai who maintains close ties with Alset via prior roles directing related entities reinforcing intertwined governance influence impacting potential conflicts of interest and funding decisions [S19][S25].

Sector Analysis (Contextual)

Emerging multi-category marketplaces aligned with community hubs face steep competition from digital-first platforms coupled with challenging unit economics for brick-and-mortar cafés especially within diverse international jurisdictions. Strategies integrating experiential retail with educational content can differentiate but require significant upfront investment fueling volatile earnings profiles typical for early-stage companies.

Robotics ventures add technological complexity demanding cross-disciplinary capabilities across software/hardware integration often lengthening time-to-market cycles beyond traditional consumer goods launches.

Summary

HWH International stands at a crossroads typified by foundational yet unproven business segments encompassing digital marketplaces interfaced with experiential cafés complemented by education services — ambitions somewhat tempered by financial constraints evident from continued substantial losses and heavy reliance on parent company funding resources.

Monitoring operational milestones around international market entries plus early traction in new verticals will be essential while accounting for structural risks related to liquidity sustainability amidst stiff sector competition.

This memorandum is based exclusively on publicly filed documents as of March 30, 2026 ([F1],[S#]) without speculative interpretations beyond stated facts. It does not constitute investment advice nor recommend any transaction.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments