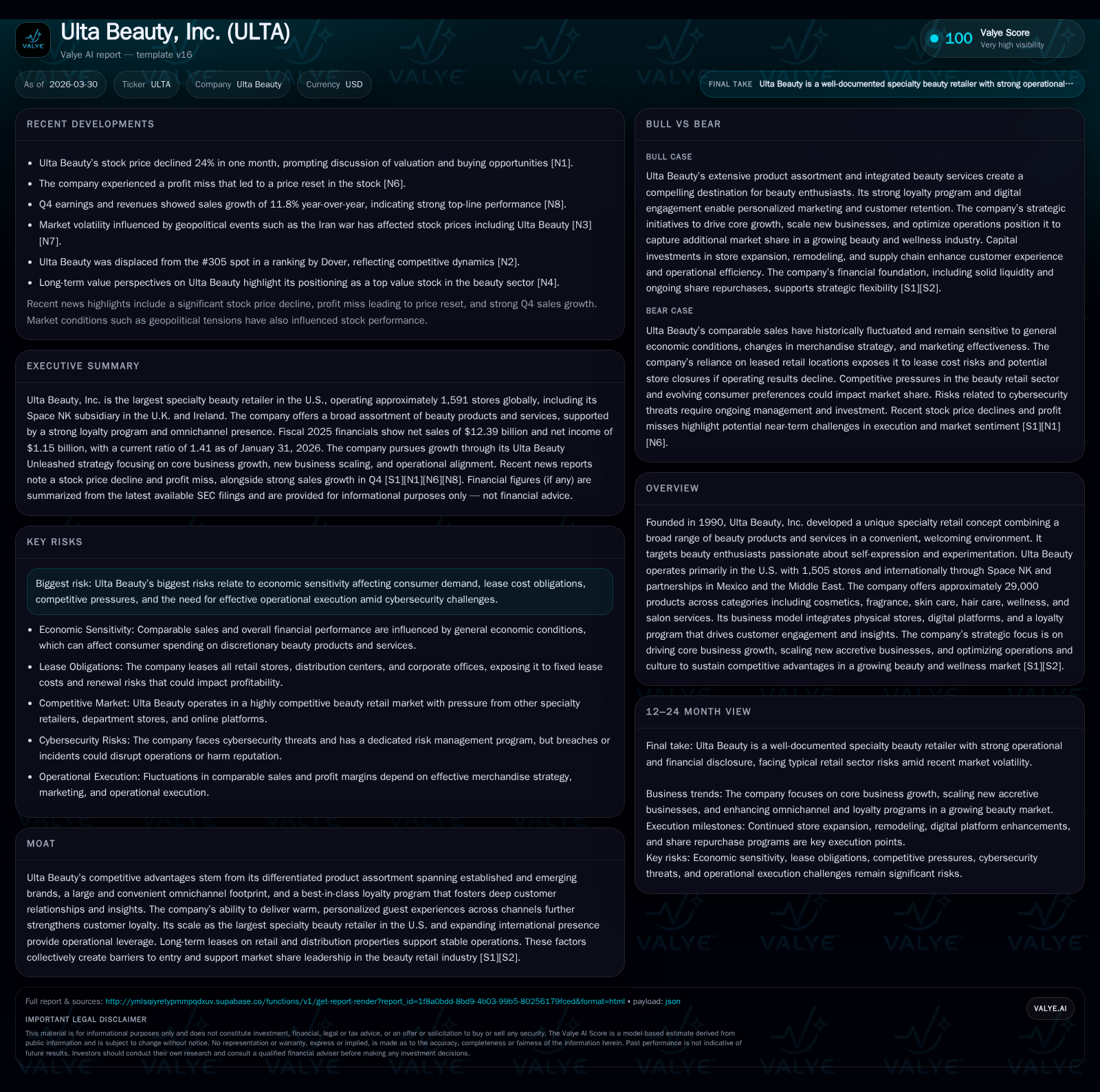

Ulta Beauty's Growth Moderates with Strategic Omnichannel Expansion and Robust Cash Flow

Ulta Beauty sustains market leadership by leveraging its differentiated beauty retail model amidst evolving consumer and operational dynamics.

Ulta Beauty, Inc. remains the largest specialty beauty retailer in the U.S., operating over 1,500 stores and an expanding international footprint through Space NK and partnerships. The company reported near $12.4 billion in revenue for fiscal 2025, reflecting a 9.7% sales growth year-over-year, but operating income saw a slight decline amid higher costs. Ulta’s strategic focus on enhancing its omnichannel capabilities, loyalty program, and expanding new business lines underpins prospects for sustained market share gains. Strong operating cash flows have supported aggressive share repurchases and capital investments, though economic sensitivity and competitive pressures present ongoing risks.

Company Overview and Historical Performance

Founded in 1990, Ulta Beauty has carved out a distinctive position within specialty beauty retailing by combining a broad assortment of prestige and mass-market brands with salon services under one roof. As of January 31, 2026, Ulta operated approximately 1,505 stores primarily across the United States and extended its reach internationally through its luxury beauty retailer subsidiary Space NK in the U.K. and Ireland, alongside partnerships in Mexico and the Middle East [S1][S5].

For fiscal year (FY) ended January 31, 2026 (FY2025), Ulta posted revenues of $12.39 billion—an increase of nearly 10% compared to $11.30 billion in FY2024—reflecting both comparable store sales gains and new store openings as part of organic expansion [F1]. Operating income declined marginally by about 2% year-over-year to $1.53 billion from $1.56 billion in FY2024 due primarily to elevated selling, general & administrative expenses (SG&A), rent commitments related to long-term leases in prime retail locations, and investments supporting omnichannel growth strategies [F1][S19]. Net income dropped roughly 4% to $1.15 billion from $1.20 billion previously owing to these increased costs despite robust top-line performance [F1].

The company's financial health remains solid with liquidity supported by $424 million cash and equivalents at year-end and a current ratio around 1.41, underscoring adequate short-term asset coverage over liabilities [F1]. Despite accessible revolving credit facilities totaling up to $1 billion (and £40 million separately for Space NK), Ulta had no balance on its primary credit line as of January 31, 2026 [S7][S10], signaling strong operational cash flow sufficiency.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 12.4 | 1153 | 1503 | 1533 | +9.7% | -4.0% |

| 2024 | 11.3 | 1201 | 1339 | 1565 | +0.8% | -7.0% |

| 2023 | 11.2 | 1291 | 1476 | 1678 | +9.8% | +3.9% |

| 2022 | 10.2 | 1242 | 1482 | 1639 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 901 | 1068 | 41.1 |

| 2024 | 1003 | 964 | 48.3 |

| 2023 | 996 | 1041 | 56.6 |

| 2022 | 900 | 1170 | 63.4 |

Source: SEC companyfacts cache [F1].

Table: Key Financial Metrics (FY) - Rounded values from SEC filings [F1]

Business Model Nuances and Drivers

Ulta’s category-spanning assortment encompasses around 29,000 SKUs across cosmetics, fragrance, skincare, hair care, wellness products, alongside full-service salons within most stores—a notable differentiation factor relative to many peers focused exclusively on product or service segments separately [S13][S14]. This ‘one-stop’ experiential model furthers customer engagement through tactile interaction plus personalized salon services driving repeat visitation.

The company’s omnichannel platform integrates physical stores with online sales channels secured via its website and mobile apps while underpinning customer targeting with one of retail’s largest loyalty programs—boasting millions of active members who accrue points on both product purchases and salon services that fuel customer insight analytics for merchandising precision [S13][S14].

Historically strong comparable store sales have been volatile but positive drivers alongside strategic store expansions in high-traffic power centers have contributed materially to growth dynamics evident over recent years culminating in near double-digit overall revenue growth for FY2025.

Forward Growth Prospects

Ulta emphasizes growth through three core pillars within its "Ulta Beauty Unleashed" strategy: driving core business growth via operational excellence; scaling new accretive businesses including international expansion; and optimizing the underlying organizational culture for sustained competitive strength [S5].

Emerging initiatives target further digital engagement enhancements—such as immersive online try-on tools—and enriched personalization fueled by loyalty program data analytics that augment guest experience consistency across online and offline touchpoints.

Internationally, Space NK adds luxury segment exposure supporting incremental revenue outside the U.S., while joint ventures extend brand reach into Mexico and the Middle East targeting diverse demographic cohorts adaptable to evolving beauty trends globally.

Key growth confines revolve around economic sensitivity given discretionary nature of beauty products/services—where inflationary pressures or recessionary dips can dampen consumer spend—alongside escalating lease obligations from long-term property contracts that limit expense flexibility during downturns [S24][S25]. Competitive intensification especially from digitally native brands encroaching on market share necessitates continuous innovation.

Financial Capital Allocation & Returns

Cash flow generation is a standout strength; Ulta generated over $1.5 billion in operating cash flow for FY2025—a notable increase versus prior periods—providing ample resources for capital investment while sustaining considerable shareholder returns [F1][S15]. Capital expenditures rose modestly by ~16% to about $435 million primarily allocated toward new store openings, renovations, technology systems upgrades, and supply chain logistics improvements aimed at faster inventory turns during peak seasons (e.g., holidays) [F1][S15].

Share repurchases remain aggressive with ~$900 million deployed over FY2025 under ongoing authorization programs initiated since early-2020s; such buybacks underscore management’s confidence in intrinsic value while offsetting dilution effects from stock-based compensation plans [F1][S11]. Importantly dividends are nominal per earlier disclosures possibly reflective of preference for reinvestment paired with buybacks.

Approximate return on equity based on latest net income relative to equity stands robust around ~41%, an indicator pointing towards efficient capital deployment despite margin pressure headwinds stemming from expense inflations [F1].

Operational & Strategic Risks

Economic volatility poses principal risk given Ulta’s anchoring in discretionary consumer categories where demand elasticity can be pronounced amid inflation or recession fears—with attendant impacts on comparable sales fluctuations identified explicitly by management as significant exposure factors [S24]. Lease commitments comprise another substantial fixed-cost element given most stores occupy high-demand power center locations under decade-plus leases with extension options reinforcing cost rigidity even during softer demand cycles [S1][S22].

Cybersecurity constitutes a continuously evolving risk vector addressed through a dedicated executive governance model involving cross-functional oversight by the Board's Audit Committee supplemented by specialized leadership ensuring proactive monitoring of threat landscapes alongside incident response preparedness—a critical focus given increasing reliance on digital retail infrastructure integrated with customer data ecosystems [S1].

Competitive pressures derive not only from traditional brick-and-mortar rivals but also digital-native disruptors offering niche or direct-to-consumer models requiring persistent innovation across merchandising mix as well as experiential service differentiation complemented by technological responsiveness that reduces friction throughout shopping journeys [N2][N3].

What To Watch Next: Analyst Perspective

Although explicit forward guidance was not provided in available disclosures for FY2026 or subsequent periods beyond routine commentary on strategic priorities ([N2]), salient indicators include quarterly comparable sales performance amidst macroeconomic shifts; margin trend stability particularly related to SG&A control; cadence of new store openings versus remodels; progression of international ventures; loyalty member engagement metrics; capital allocation updates especially share repurchase pace; as well as any material developments on cybersecurity front or supply chain disruption risks.

Monitoring management commentary around promotional elasticity effects post-holiday season or impact from shifting consumer preferences will provide timely insight into how well Ulta navigates prevailing economic uncertainty while sustaining differentiated guest experiences central to its core value proposition.

Conclusion

Ulta Beauty’s entrenched position as America’s leading specialty beauty retailer is underpinned by a multi-dimensional strategy balancing product breadth, service integration via salons, digital omni-channel capabilities including mobile platforms plus a robust loyalty ecosystem generating rich consumer data insights—all sustained through meaningful capital reinvestment and shareholder returns via buybacks.

The recent fiscal performance highlights steady revenue acceleration tempered somewhat by margin pressures amid inflationary costs yet mitigated overall by disciplined cash flow management fostering strategic agility.

Going forward growth hinges critically on execution excellence across store expansions combined with evolving digital innovations responsive to consumer trends domestically alongside measured international scale-up efforts. Concurrently management must prudently navigate enduring risks embedded in lease commitments fluctuations alongside intensifying competition exacerbated by macroeconomic headwinds challenging discretionary spending patterns. This blend keeps Ulta poised for continued relevance while demanding purposeful operational focus.

Disclaimer: This report is intended solely for informational purposes based on publicly available data as of March-April 2026 without any investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments