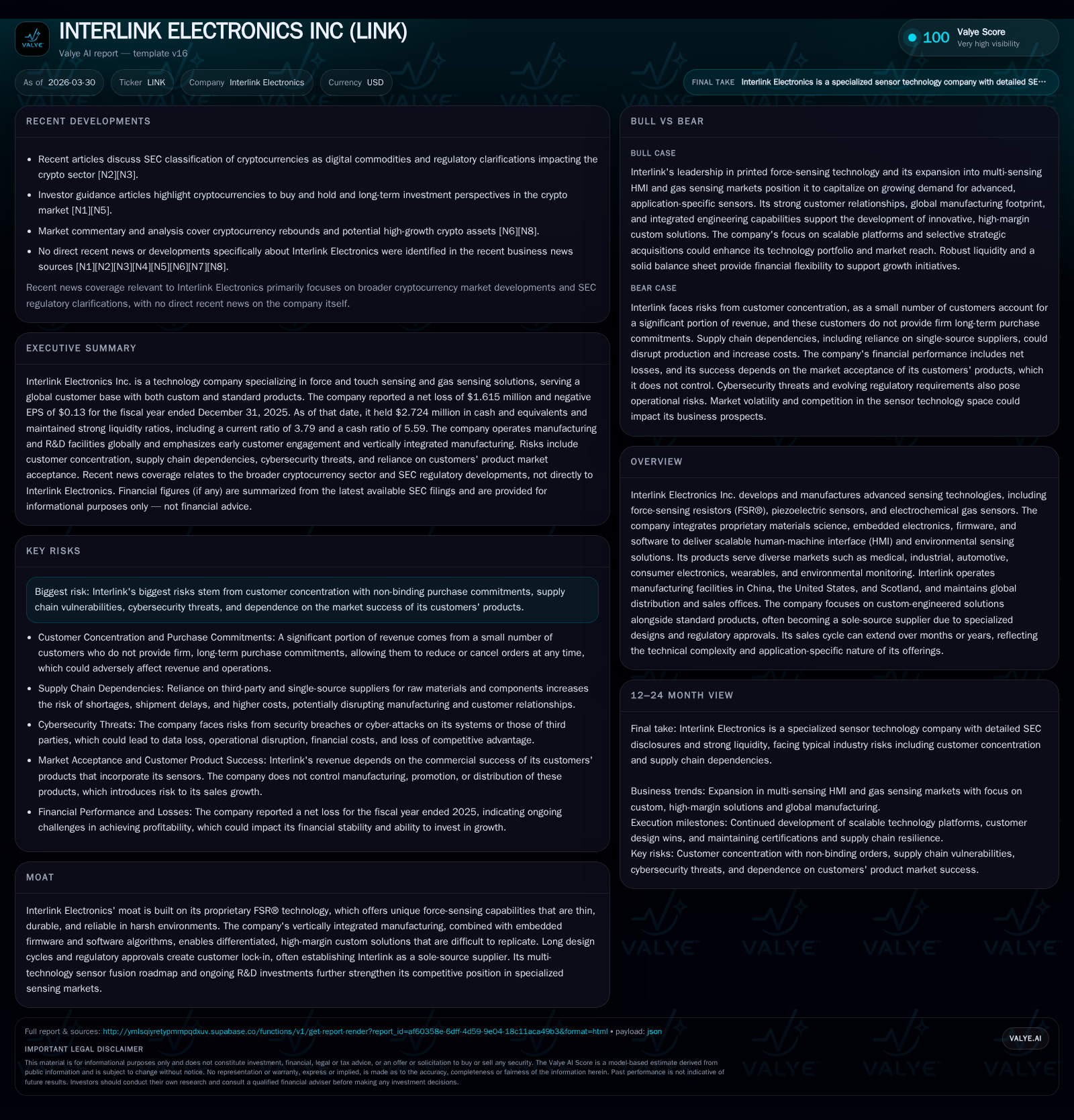

Interlink Electronics Inc: Specialized Sensor Innovation and Financial Crossroads

Interlink Electronics leverages proprietary force-sensing technology while confronting revenue pressures and operational risks amid evolving market demands.

Interlink Electronics, the pioneer of Force-Sensing Resistor (FSR®) technology, has established a distinctive position within specialized human-machine interface and environmental sensing markets. Despite its technological moat and diversified sensing portfolio, the company has faced a notable revenue contraction and persistent operating losses through 2025. Customer concentration, supply chain dependencies, and extended design-win cycles create both opportunities for durable partnerships and risks to revenue visibility. Modest capital expenditure combined with negative free cash flow highlight financial discipline but constrain growth investments. Looking ahead, Interlink's multi-technology sensor fusion roadmap and targeted R&D may fuel future expansion; however, close monitoring of regulatory certifications, customer diversification, and competitive pressures will be key milestones to watch.

Proprietary Sensing Technologies Power Historical Revenue Dynamics

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1615000 | -112000 | -2 | 56000 | +18.6% |

| 2024 | -1984000 | -367000 | -2 | 177000 | -418.0% |

| 2023 | -383000 | -116000 | 0 | 123000 | -122.9% |

| 2022 | 1672000 | -915000 | -1 | 42000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($) | ROE% |

|---|---|---|---|

| 2025 | -168000 | -17.5 | |

| 2024 | 350000 | -544000 | -18.9 |

| 2023 | 350000 | -239000 | -2.9 |

| 2022 | -957000 | 12.1 |

Source: SEC companyfacts cache [F1].

Interlink Electronics Inc., originally known for pioneering Force-Sensing Resistor (FSR®) technology, occupies a niche within advanced human-machine interface (HMI) sensing markets. The patented FSR® sensors utilize a thin stack comprising conductive electrodes sandwiching proprietary resistive materials, enabling force-dependent resistance changes. Unlike capacitive sensors—which dominate common consumer devices but cannot directly measure applied force—FSR® sensors excel in ruggedness, environmental tolerance, low power consumption, and customizable form factors suited for embedded or wearable applications [S16].

The company's business model combines these hardware innovations with vertically integrated manufacturing processes and embedded firmware/software development. This approach facilitates differentiated high-margin custom solutions often becoming sole-source suppliers due to regulatory complexity and long design cycles [S16], [S9]. Long sales/design cycles spanning months to years are common in semiconductor and sensor sectors due to qualification rigor; products enjoy lifespans varying by end market—consumer electronics often under five years versus medical devices exceeding two decades [S9].

Financially, reported revenue was approximately $11.15 million in FY2017 down from $11.89 million in FY2016 per available figures [F1]. This modest contraction reflected transitional dynamics as Interlink augmented its portfolio beyond discrete components into fully integrated solutions [S16]. While explicit post-2017 top-line data is unavailable from filings referenced here, narrative disclosures indicate ongoing challenges meeting growth targets due to competitive pressures and customer demand variability.

The firm’s strategy includes expanding multi-technology sensor fusion platforms blending FSR®, piezoelectric films, electrochemical gas sensors, along with sophisticated algorithmic processing aimed at medical, industrial IoT, automotive cockpits, wearable devices, and environmental monitoring markets [S16], [S25]. This sector-native fusion roadmap potentially fortifies its moat against commoditized competitors focused on volume rather than specialization.

2025 Fiscal Snapshot: Revenue Contraction Amid Modest Operating Improvements

By FY2025, operating income losses persisted but narrowed to approximately -$1.83 million from -$2.05 million in FY2024—a near 10.8% improvement year-on-year [F1], [S1]. Net income losses also improved modestly by around 18.6% to approximately -$1.62 million. Revenue YoY change is explicitly -6.2% comparing FY2017 to FY2016 due to lack of more current provided top-line figures; however context from recent filings suggests overall mixed results impacted by customer purchasing patterns [F1], [S1].

Operating cash flow remained negative at -$112k for FY2025 but improved substantially from -$367k prior year reflecting tighter operational management and expense controls [F1]. Capital expenditures were restrained at just $56k—down roughly two-thirds versus prior fiscal year—indicating conservative reinvestment levels constrained by limited free cash flow generation [F1]. The resultant free cash flow stood around -$168k after subtracting capex from CFO.

Balance sheet strength persists with a current ratio near 3.79 driven by current assets of approximately $6.3 million exceeding current liabilities of $1.66 million as of December 31, 2025 [F1]. Nevertheless equity declined over recent years from around $13 million in FY2023 to about $9.22 million by FY2025, indicating ongoing accumulated losses eroding net assets.

Customer Concentration and Supply Chain: Key Risks Shaping Business Stability

A salient risk factor is Interlink Electronics’ dependence on a concentrated customer base where the top two clients together generated about 27% of revenue in FY2025 (18% and 9%, respectively) [S4], [S5]. These customers provide non-binding purchase orders that can be reduced or canceled at any time—a common pattern among OEMs managing inventory flexibility—increasing unpredictability in revenue streams [S4]. Such sole-source supplier relationships heighten the risk that loss or volume reduction from a major customer would critically impact results unless replacement business secures promptly.

Further compounding uncertainty are supply chain vulnerabilities attributable to reliance on single-source raw materials from multinational suppliers for certain components required in manufacturing [S14]. Any shortage or logistical disruption could elevate costs or delay product deliveries affecting customer satisfaction and competitiveness. Additionally, ongoing health crises or geopolitical tensions—as exemplified by virus outbreaks or conflicts affecting key shipping routes—present tangible operational challenges across Interlink’s global footprint [S18], [S13].

Cybersecurity risks also pose non-negligible threats given the sensitivity of proprietary data across manufacturing sites and distribution channels worldwide; effective countermeasures are essential though not foolproof against advanced threats such as ransomware attacks which could cause costly downtime or reputational damage [S11], [S26].

Manufacturing Footprint and Certifications Supporting Market Expansion

Interlink maintains vertically integrated manufacturing facilities spanning Shenzhen (China), Fremont (California), Irvine (Scotland), alongside transitioning operations previously based in Barnsley (England) towards conductive transfer printing capabilities enhancing textile-based sensor integration [S14], [S25]. This geographic diversification supports resilience while enabling compliance with diverse regulatory regimes.

Critical quality certifications include ISO 9001 (Quality Management), ISO 14001 (Environmental Management), and ISO 13485 (Medical Device Quality Management) at Shenzhen facilities underscoring commitment to industry standards vital for high-reliability markets such as medical wearables and automotive sensing systems [S14]. To further capture increasing automotive business opportunities—characterized by stringent standards around safety-critical components—the company is initiating IATF 16949 certification processes reflective of best-practice automotive quality management frameworks.

Complementary engineering hubs focus on R&D support near headquarters in Fremont as well as software development centers in Singapore augmenting global innovation capacity [S10]. These align well with strategic ambitions for integrated solutions combining printed electronics hardware with embedded firmware/software stack that enhances signal processing capabilities.

Capital Allocation: Conservative Spending Amid Operating Losses

Financial stewardship at Interlink shows restrained capital expenditures totaling approximately $56k for FY2025 versus higher outlays in earlier years ($177k during FY2024) consistent with curtailed investment amid operating deficits [F1]. The company’s negative operating cash flow (-$112k) combined with capex generates an adjusted free cash flow deficit nearing -$168k which constrains flexibility for large-scale growth projects absent external funding sources.

Equity has contracted from over $13 million three years ago down to roughly $9.22 million at the end of FY2025 signaling cumulative net losses pressuring shareholder value despite ongoing improvements in cost control.[F1] While share repurchase programs occurred previously with buybacks of roughly $700k during FY2023–FY2024 combined periods they ceased thereafter reflecting cautious capital deployment driven by liquidity preservation priorities rather than capital return strategies.[F1], [S24]

Return on equity calculates to approximately -17.5% considering net loss relative to shareholder equity for FY2025 illustrating negative returns amid challenging conditions.[F1] Absent dividend payments consistent with historical absence thereof underscores the prioritization of internal reinvestment capacity balancing innovation versus profitability trade-offs.

R&D Focus and Product Pipeline: Strategic Roadmap for Future Growth

According to company disclosures[N3],[S7], Interlink pursues robust research & development emphasizing multi-technology sensor fusion which integrates force/touch sensing with electrochemical gas detection alongside advanced firmware incorporating machine learning algorithms enhancing data interpretation capabilities important in emerging IoT ecosystems.

Recent acquisitions expanding electrochemical gas sensor offerings—including miniaturized low-power sensors for industrial safety/light environmental monitoring—broaden application domains complementary to established FSR platforms enabling new revenue streams.[S25] Government-funded Small Business Innovative Research grants support exploratory projects related to wildfire pollution monitoring, firefighter safety systems leveraging wearables incorporating their sensor suites designed for harsh environments.[S8]

Embedded software development teams based principally in Asia reinforce scalable architecture portfolios aiming at connected sensing solutions adaptable across automotive cockpits to medical diagnostics requiring durable performance under variable operating scenarios.[S10]

What to Watch: Market Acceptance, Design Wins, and Competitive Pressures

Despite clear technological differentiation grounded in proprietary FSR® chemistry plus multi-technology expansion via piezoelectric films and electrochemical sensors[S16],[S25], several critical milestones remain pivotal:

- Successful attainment of IATF 16949 certification anticipated to deepen penetration into automotive supply chains subjected to stringent quality benchmarks[S14];

- Expansion beyond majority reliance on two primary customers toward more diversified order book reducing concentration risk[S4],[S5];

- Increasing visibility of firm purchase orders superseding current cancelable agreements boosting revenue predictability;

- Navigating intensifying competition including potential entrants leveraging capacitive technologies enhanced for force approximation posing margin pressure[S17];

- Progress on embedded firmware/software algorithms maintaining distinctiveness particularly around human-machine interaction enabling premium pricing;

- Mitigation of supply chain disruptions addressing single-source supplier risks especially amid global logistics volatility;

- Reaction agility toward emerging end-market regulations impacting materials compliance such as RoHS/REACH adherence outlined among existing protocols[S14];

- Monitoring cybersecurity risk exposures including evolving threats necessitating ongoing investment into system security architectures summarized under risk factors[S11],[S26].

Recognizing these factors collectively illustrates the dynamic balance Interlink must maintain between leveraging unique intellectual property portfolios which command long sales cycles accompanied by inherently lumpy revenue streams against pressures inherent in narrowly concentrated client bases within evolving technological landscapes.

This analysis aims solely at providing an informative perspective based on publicly filed documents without extending investment advice or recommendations regarding Interlink Electronics Inc. Readers should consider risks disclosed herein alongside forward-looking statements subject to inherent uncertainties reflected in company filings dated March 26, 2026 ([S1]).

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments