Spero Therapeutics' Strategic Shift Focuses on Tebipenem HBr Amid Pipeline Consolidation

Spero Therapeutics consolidates its antibiotic pipeline to prioritize tebipenem HBr development through its collaboration with GlaxoSmithKline, marking a key strategic inflection.

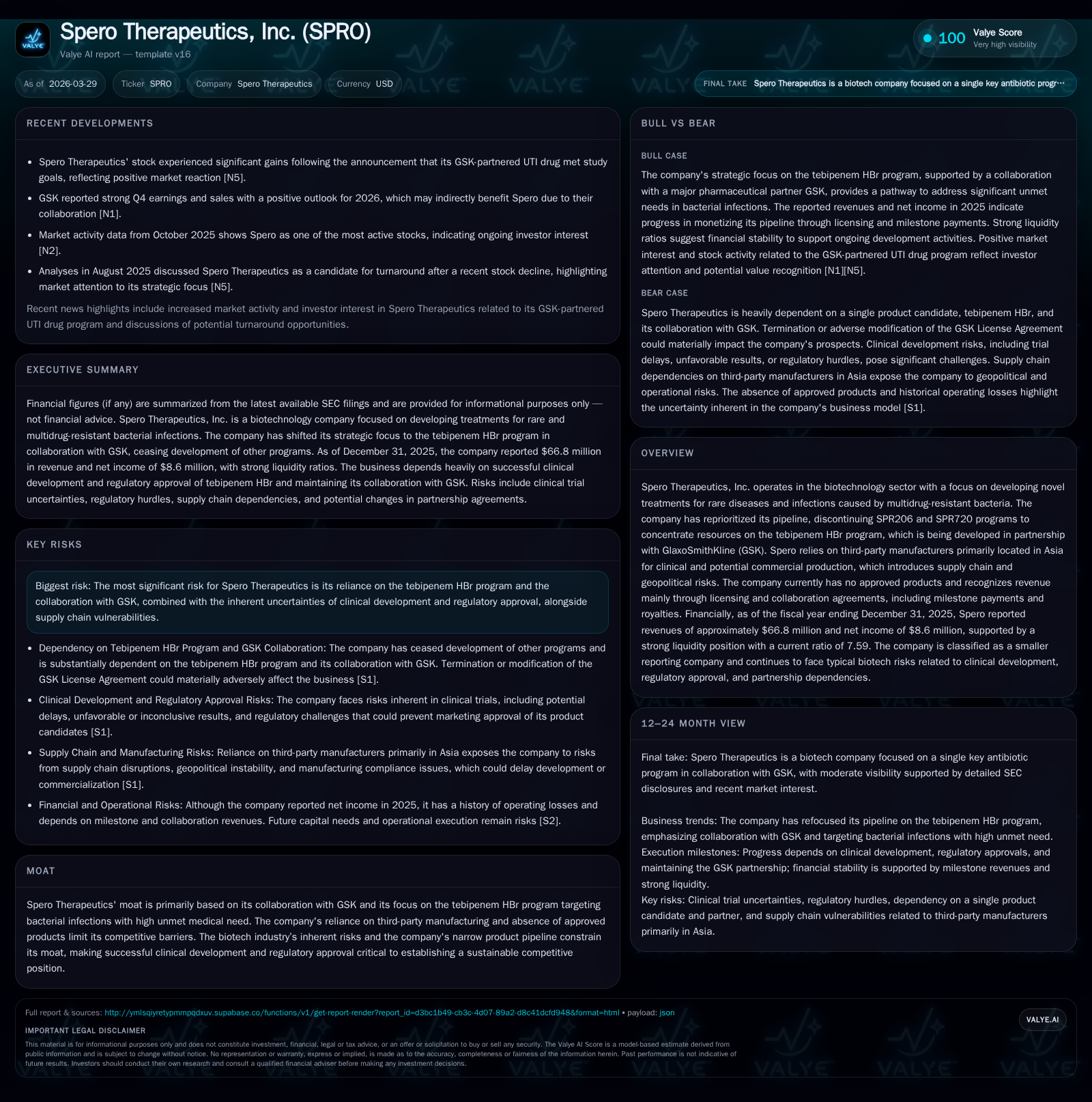

Following years of volatile financial performance and operational losses, Spero Therapeutics has refocused its strategy exclusively on the tebipenem HBr antibiotic program in partnership with GSK. This follows discontinuation of SPR206 and SPR720 programs, streamlining the company’s development efforts amid regulatory and clinical uncertainties. Financially, Spero returned to profitability in 2025, driven primarily by licensing revenues from GSK collaboration despite continued negative operating cash flow. Key risks remain tied to milestone dependencies on GSK, supply chain concentration in Asia, and ongoing regulatory and legal challenges.

Strategic Refocus and Historical Financial Performance

Spero Therapeutics has transitioned from a multi-program antibiotic developer to focusing exclusively on tebipenem HBr following cessation of SPR206 (March 2025) and SPR720 (November 2025) development programs [S1]. This strategic pivot concentrates resources on advancing tebipenem HBr, an oral carbapenem antibiotic candidate developed in collaboration with GlaxoSmithKline (GSK).

Financial results reflect this shift with revenue increasing by 39.2% from approximately $48.0 million in fiscal year (FY) 2024 to $66.8 million in FY2025 [F1]. Operating income improved substantially from a loss of $73.4 million in FY2024 to a profit of $6.3 million in FY2025 [F1]. Net income followed suit, moving from a loss of $68.6 million to positive $8.6 million over the same period [F1]. These improvements largely stem from recognition of milestone payments and collaboration revenue under licensing agreements rather than product sales, which remain absent given ongoing clinical development stages [S1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 67 | 9 | -13 | 6 | +39.2% | +112.5% |

| 2024 | 48 | -69 | -23 | -73 | -53.8% | |

| 2023 | 104 | -33 | 21 | +94.0% | ||

| 2022 | 54 | -8 | -42 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 14.5 |

| 2024 | -148.7 |

| 2023 | |

| 2022 |

Source: SEC companyfacts cache [F1].

Tebipenem HBr Collaboration and Contractual Risks

The tebipenem HBr program is central to Spero’s current strategy and is conducted under a license agreement with GSK that grants GSK commercial rights primarily for the U.S. market [S1]. Spero’s financial prospects depend heavily on milestone payments linked to clinical development progress and commercial milestones.

The license agreement allows GSK broad termination rights: at will upon notice, for material breaches by Spero or upon Spero’s bankruptcy [S1]. Additionally, if GSK exercises termination or assumes responsibility for U.S.-based development following certain triggers—including change-of-control events or breaches—milestone payments to Spero may be reduced or cease entirely [S1]. This contractual structure concentrates execution risk outside Spero’s direct control.

Regulatory approval by the FDA remains critical for commercial viability; delays or additional requirements could adversely impact partnership economics and timing [S1]. Tebipenem HBr targets complicated urinary tract infections caused by multidrug-resistant bacteria—a high unmet need area—potentially benefiting from expedited regulatory pathways but also facing stringent review standards.

Supply Chain Concentration and Regulatory Compliance Risks

Spero relies predominantly on third-party contract manufacturers based in Asia for active pharmaceutical ingredients and drug formulation [S7][S23]. While industry standard for cost efficiency, this concentration exposes the company to geopolitical tensions and trade policy uncertainties that could disrupt supply continuity.

Compliance with FDA current Good Manufacturing Practices (cGMP) is mandatory; failure to maintain quality standards risks regulatory actions including product recalls or import restrictions [S19][S4]. Ongoing post-marketing obligations such as adverse event reporting and manufacturing audits impose continuous operational demands.

Trade policy developments during early-to-mid-2025 introduced tariffs affecting pharmaceutical inputs; however exemptions for certain products have mitigated immediate tariff impacts [S8]. Broader drug pricing reforms present longer-term uncertainties that may affect future reimbursement landscapes post-approval [S14].

Financial Liquidity and Capital Allocation Analysis

At FY2025 year-end, Spero reported cash and equivalents of approximately $40.3 million against current liabilities near $8.9 million yielding a strong current ratio (~7.59x), indicating solid near-term liquidity [F1][S21]. Shareholders’ equity stood around $59 million.

Return on equity approximated 14.5%, calculated as net income relative to equity for FY2025 [F1], signaling modest profitability recovery albeit constrained by capital-intensive research and development expenditures characteristic of clinical-stage biopharmaceutical firms.

Despite accounting profitability gains ($8.6M net income), operating cash flow remained negative at about -$12.6 million due to ongoing investment in clinical programs without product-generated cash inflows [F1]. No dividends were distributed nor share buybacks executed consistent with reinvestment priorities during pre-commercial phases.

Legal Environment and Current Litigation Status

Previously disclosed securities class action lawsuits related to alleged misleading statements about tebipenem HBr’s FDA approval prospects were consolidated then dismissed with prejudice by October 2024 [S6][S12][S25]. Derivative suits were similarly dismissed or withdrawn.

An SEC investigation concluded without enforcement action against the company itself; cease-and-desist orders were issued only against certain former executives in early 2026 [S9][S26]. These legal developments reduce immediate litigation risk though underscore governance vigilance needs.

Outlook Considerations

Absent explicit forward-looking guidance tied directly to partner-driven milestones ([N#]/[S#] unavailable), key value drivers include:

- Progress toward FDA approval milestones for tebipenem HBr,

- Stability and continuation of the GSK license agreement without termination,

- Clinical trial advancements addressing complicated urinary tract infections,

- Maintenance of reliable supply chains amid geopolitical dynamics,

- Resolution or absence of further legal or regulatory impediments,

- Ability to scale manufacturing post-approval transitioning toward commercialization.

This strategic focus positions Spero for potential growth predicated upon successful clinical validation and partner execution amid inherent biotech sector risks.

This analysis integrates data from Spero Therapeutics’ SEC filings through March 26, 2026 alongside structured financial metrics disclosed by the company without extrapolation beyond documented evidence. It reflects the complex interplay between scientific development challenges, partnership dependencies, regulatory compliance demands, financial stewardship imperatives and legal considerations faced by emerging specialty antibiotic developers.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments