Vivani Medical's Clinical Progress and Capital Challenges Shape Growth Trajectory

Vivani Medical advances GLP-1 implant trials amid persistent cash burn and financing needs.

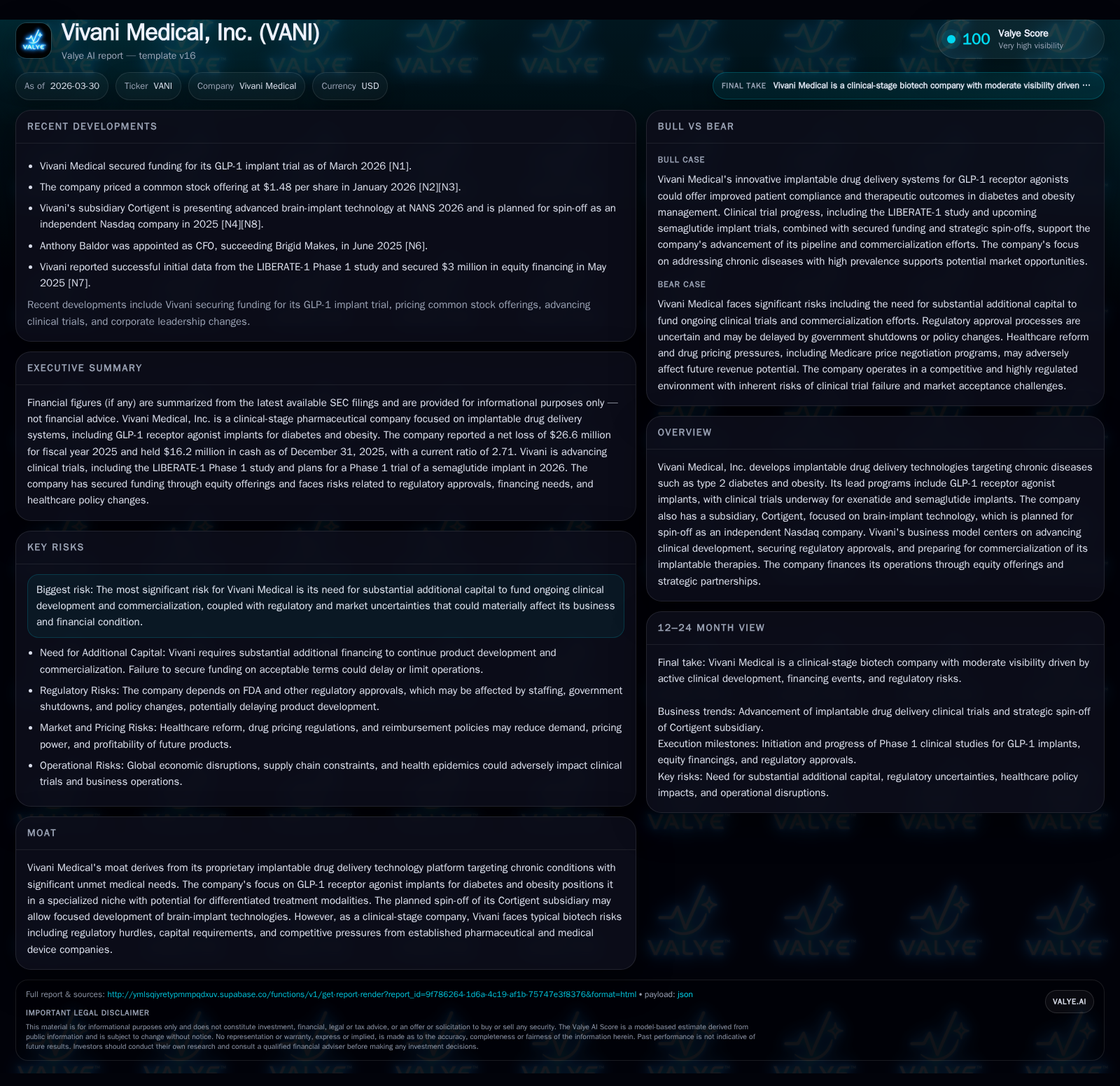

Vivani Medical, Inc. is a clinical-stage biotech focused on implantable drug delivery for chronic diseases like type 2 diabetes and obesity. Its key programs involve GLP-1 receptor agonist implants for exenatide and semaglutide, backed by ongoing clinical trials. The company continues to operate at significant net losses and negative cash flow, requiring frequent equity raises for funding its development activities. Future growth will hinge on successful regulatory approvals and commercialization milestones in an uncertain reimbursement and competitive environment.

Company Overview

Vivani Medical, Inc. specializes in developing implantable drug delivery technologies targeting chronic diseases such as type 2 diabetes and obesity. Its proprietary platform focuses primarily on delivering GLP-1 receptor agonists (notably exenatide and semaglutide) via subcutaneous implants designed to provide controlled and sustained release of peptide therapeutics. This approach aims to improve patient compliance compared to daily injections or oral therapies.

Alongside its lead diabetes/obesity pipeline, Vivani owns Cortigent, a subsidiary developing brain-implant technology to address neurological conditions; this unit is planned for spin-off as a separate Nasdaq-listed entity to enable focused development paths.

The company's business model revolves around advancing clinical development through regulatory approvals towards eventual commercialization, relying principally on equity financings and strategic partnerships to fund operations.

Historical Financial Performance

Revenues remain minimal and attributable mainly to research collaborations rather than any commercial product sales. The latest annual revenue figure stands at approximately $4.0 million as of FY2016—marking a steep decline of about 55% year-over-year compared to prior years where revenue peaked near $9 million [F1].

Operating losses have grown consistently due to expanded R&D activities associated with clinical trial expenses. FY2025 operating income shows a loss of about $27.6 million, worsening roughly 12% from the prior year. Net income followed similar trends with a negative $26.6 million reported for FY2025 [F1].

Operating cash flow trends mirror the income statement with persistent cash burn—CFO amounted to negative $24.3 million in FY2025—and accelerated CapEx spending (up to $1.17 million in FY2025) reflects investment in trial infrastructure and technology enhancements [F1].

Liquidity-wise, the company maintains around $16.2 million in cash and equivalents as of end-2025 with current assets exceeding current liabilities by a factor of approximately 2.7x—a useful short-term buffer but insufficient given ongoing negative free cash flow estimated at nearly $25.5 million [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -27 | -24 | -28 | 1173000 | -13.3% |

| 2024 | -23 | -21 | -25 | 556000 | +8.4% |

| 2023 | -26 | -24 | -27 | 887000 | -84.7% |

| 2022 | -14 | -19 | -21 | 338000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -25 | -169.2 |

| 2024 | -21 | -133.4 |

| 2023 | -25 | -123.6 |

| 2022 | -19 | -31.3 |

Source: SEC companyfacts cache [F1].

Note: Revenue data limited; major focus on R&D activity reflected in losses.

Recent Operational Developments and Trial Progress

Significant operational milestones over the last two years include the lifting of an FDA full clinical hold on the LIBERATE-1 Phase 1 study assessing NPM-119 (exenatide implant), initially imposed in August 2023 but resolved mid-2024 [S2]. Regulatory approvals were secured for revised studies both for exenatide implants involving obese/overweight patients in Australia starting late September 2024.

In August 2025, Vivani shifted focus strategically towards accelerating the development of its semaglutide implant program (NPM-139), reporting favorable data from the exenatide implant Phase 1 trial as part of this realignment [S2][S13][N1]. Initiation of the semaglutide implant Phase 1 trial is planned for H1 2026 pending necessary regulatory clearances [N1][S13].

Meanwhile, peripheral developments include plans to spin off Cortigent to pursue specialized brain-implant technologies independently—a move aimed at sharpening management focus and unlocking subsidiary value .

Industry Context & Competitive Environment (Analysis)

Within the broader medtech/pharma ecosystem, implantable drug delivery systems represent a niche intersection between sustained-release pharmaceuticals and minimally invasive medical devices—primed to address adherence challenges inherent to chronic conditions like diabetes and obesity.

GLP-1 receptor agonists have become foundational treatments due to their efficacy in glycemic control and weight management; however, traditional formulations rely heavily on frequent subcutaneous injections which can limit real-world adherence and outcomes.

Vivani’s platform targets this pain point by offering long-lasting implants that can deliver steady peptide doses over extended periods potentially transforming treatment paradigms if clinical safety/efficacy benchmarks are met.

The pathway toward commercialization faces multiple gatekeepers including rigorous FDA evaluation processes complicated by evolving drug pricing reforms—such as Medicare Drug Price Negotiation initiatives—that could materially affect expected revenue streams post approval [S9][S11][S12]. Competition is also intense from established pharmaceutical firms rapidly developing next-generation formulations or alternative delivery devices.

Future Growth Prospects & Constraints

Growth hinges critically on successfully navigating clinical development milestones—especially completing Phase 1 trials with safety signals favorable enough to advance into later stages—and securing regulatory approvals globally.

Potential catalysts include:

- Initiation/completion of Phase 1 semaglutide implant studies.

- Positive clinical data readouts validating sustained-release kinetics and safety.

- Regulatory clearances enabling marketing submissions.

- Realization of financial efficiencies via potential Cortigent spin-off unlocking shareholder value.

Constraints are considerable:

- Need for substantial ongoing capital infusions poses dilution risks amid market volatility [S7].

- Uncertainties surrounding drug pricing policies could compress theoretical pricing power.

- Competitive encroachment from both pharma incumbents scaling advanced biologics delivery technologies and device makers innovating alternative solutions.

- Trials carry typical biotech attrition risks including unforeseen adverse events or suboptimal pharmacokinetics impacting FDA review timelines.

Capital Allocation & Balance Sheet Considerations

Vivani operates without positive operating income or cash flow generation capabilities at present necessitating reliance on external funding sources primarily equity issuance programs disclosed through periodic private placements and registered offerings totaling roughly $15–16 million gross proceeds combined during late 2025 alone .

No dividends or share repurchase initiatives have been undertaken given negative earnings profiles point toward prioritizing capital conservation for research activities rather than shareholder distributions.

The company’s equity base has contracted over recent years from nearly $44 million in FY2022 down to about $15.7 million by end-FY2025 consistent with cumulative losses eroding net book value despite fresh financings [F1].

A rough calculated ROE based on latest annual net loss against shareholder equity approximates negative 169%, reflecting the immature stage of operations centered around pipeline development rather than profit generation currently [F1].

What To Watch Next (Analysis)

Key upcoming milestones that could materially influence Vivani’s trajectory include:

- FDA clearance initiation timing for NPM-139 phase 1 semaglutide implant study set for H1 2026.

- Interim clinical data releases demonstrating implant safety/tolerability profiles which will guide investor perception around technical feasibility.

- Progress updates regarding Cortigent spin-off execution schedule.

- Additional fundraising activities necessary to sustain multi-year pivotal trial phases ahead.

- Regulatory developments concerning healthcare reforms impacting pricing paradigms applicable once commercial launch becomes feasible.

Risk Factors Summary

Vivani faces layered risks typical of early-stage biotech firms: significant liquidity needs remain paramount amid increasing clinical expenditure commitments; regulatory delays or unfavorable trial outcomes could derail timelines resulting in protracted capital consumption cycles; healthcare policies targeting drug cost reductions create an unpredictable commercial environment post-launch; competitive pressures from larger integrated pharma-device players may challenge market entry.[S4][S8][S9]

Moreover, geopolitical instability affecting supply chains or government shutdowns influencing FDA processes further amplify operational uncertainties documented extensively across SEC filings.[S14][S15]

Conclusion

Vivani Medical’s current positioning reflects a high-risk/high-potential profile inherent among clinical-stage biotech players pioneering novel modalities such as GLP-1 receptor agonist implants targeting widespread metabolic disorders prevalent globally. Challenges around sustained financing alongside execution risks persist alongside a complex regulatory landscape fraught with evolving reimbursement dynamics reflecting macro-political-economic shifts alike. Yet advancements launching pivotal clinical programs paired with strategic corporate restructuring via its Cortigent spin-off hint at deliberate efforts to sharpen operational focus aligned toward eventual commercialization readiness across multiple therapeutic niches. Stakeholders should monitor forthcoming trial results closely alongside capital raising initiatives which will decisively shape Vivani’s medium-term growth outlook amid an intensely competitive innovation ecosystem within biotech-medtech interfaces.

This analysis summarizes publicly available information without expressing investment recommendations or forecasts beyond disclosed company statements and SEC filings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments