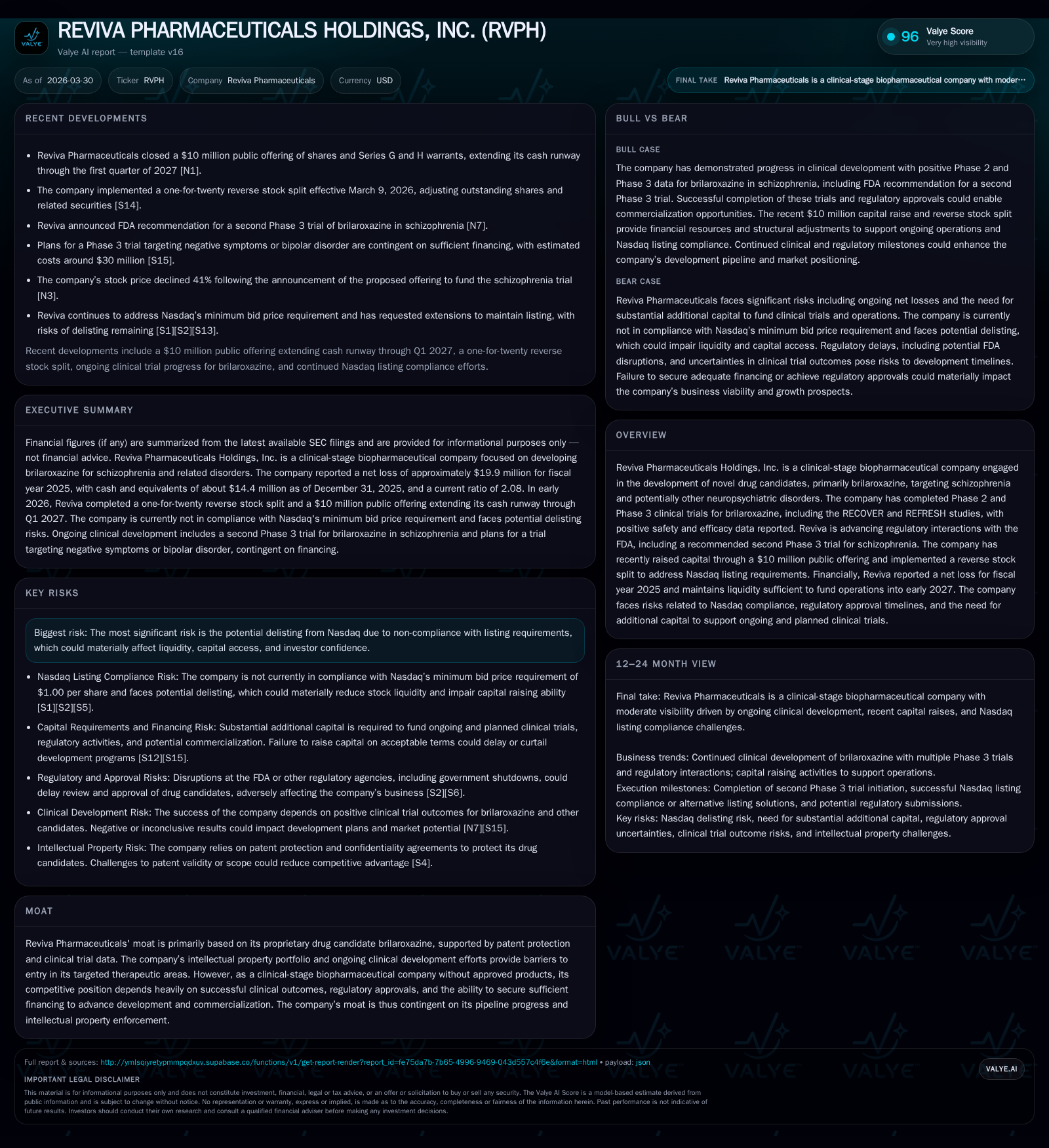

Reviva Pharmaceuticals’ Clinical Advances and Capital Dynamics in 2026

The clinical promise of brilaroxazine contrasts sharply with the company’s ongoing capital and listing challenges.

Reviva Pharmaceuticals is at a pivotal junction, advancing its lead candidate brilaroxazine through critical Phase 3 schizophrenia trials backed by positive safety and efficacy data. Despite encouraging clinical milestones, the firm continues to face significant liquidity constraints and Nasdaq compliance hurdles that threaten its public listing and operational runway. Recent capital raises and a reverse stock split have extended its cash runway into early 2027, but the necessity for further funding remains a dominant risk factor. Monitoring regulatory interactions alongside financial discipline will be key for Reviva’s near-term trajectory.

From Losses to Clinical Milestones: Historical Performance Review

Reviva Pharmaceuticals has experienced a multi-year pattern of substantial negative operating income as it pursues late-stage clinical development for its drug candidates. In fiscal year (FY) 2025, operating losses narrowed to approximately -$20.2 million, a significant improvement compared to -$30.8 million in FY 2024 and -$39.5 million in FY 2023 [F1]. This represents roughly a 34.4% year-over-year reduction in operating loss. Similarly, the net loss improved by about 33.6% in FY 2025 to just under -$19.9 million [F1].

Operating cash flow (CFO), while remaining negative due to aggressive R&D spend, also showed a marked improvement from -$33.5 million in FY 2024 to -$24.6 million in FY 2025, representing a 26.7% year-over-year improvement [F1]. This trend indicates tighter operational management despite intensified clinical activity.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -20 | -25 | -20 | +33.6% |

| 2024 | -30 | -34 | -31 | +23.8% |

| 2023 | -39 | -28 | -40 | -61.3% |

| 2022 | -24 | -19 | -24 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -229.7 |

| 2024 | -3682.0 |

| 2023 | -686.5 |

| 2022 | -197.6 |

Source: SEC companyfacts cache [F1].

The company's current ratio stood at approximately 2.08 as of December 31, 2025, indicating adequate short-term liquidity relative to liabilities [F1]. Equity rebounded from near depletion at $0.8 million in FY 2024 to $8.6 million in FY 2025, largely reflecting recent equity raises [F1].

This financial snapshot encapsulates Reviva’s transition from deeper losses toward better profitability metrics while reinforcing the imperative of continued financing to sustain its R&D-intensive pipeline.

Innovating Neuropsychiatric Care: The Promise of Brilaroxazine

Reviva's lead candidate, brilaroxazine (RP5063), exemplifies next-generation therapeutic development driven by a chemical genomics platform aimed at multiple central nervous system disorders [S1]. Its therapeutic scope includes schizophrenia, bipolar disorder, major depressive disorder, ADHD, behavioral and psychotic symptoms associated with dementia (BPSD) and Alzheimer's disease, as well as Parkinson’s disease psychosis.

The molecule notably carries Orphan Drug Designations granted by the FDA for pulmonary arterial hypertension (PAH) and idiopathic pulmonary fibrosis (IPF), underscoring its potential wider utility beyond neuropsychiatry [S1]. These orphan statuses offer regulatory incentives such as market exclusivity that bolster commercial viability.

Brilaroxazine has progressed through pivotal Phase 2 and Phase 3 clinical trials—primarily the RECOVER and REFRESH studies—which reported favorable safety profiles alongside efficacy endpoints aligned with symptomatic relief in schizophrenia [N3], [S1]. These data produced sufficient confidence for FDA dialogue recommending a second Phase 3 trial to reinforce efficacy assertions prior to New Drug Application (NDA) submission—a crucial regulatory milestone [S11].

Composition of matter patents secured across major jurisdictions including the U.S., Europe, and select international markets provide backbone intellectual property protection against generic competition [S1]. However, ongoing patent office proceedings coupled with potential oppositions represent litigation risks typical within biopharma innovation cycles [S8].

Capital Drive: Public Offerings and Nasdaq Compliance Challenges

Despite robust scientific progress, Reviva has grappled with market perception amplified by compliance struggles on Nasdaq’s minimum bid price rule requiring shares trade above $1 per share [S2], [S7]. Receipt of deficiency notices from Nasdaq triggered a mandated corrective timeline culminating in an implemented reverse stock split of one-for-twenty shares effective March 9, 2026 [S13], [S18].

This reverse split was intended to elevate trading prices artificially to meet listing thresholds without diluting existing shareholder percentage interests but carries inherent market risks including potential liquidity diminishment post-adjustment [S18]. Notably, announcements surrounding such corporate actions drove volatility with share price plunges exceeding 40% amid fundraising news releases reflecting investor dilution concerns triggered by warrant issuances bundled with equity offerings [N2], [N3].

The company’s $10 million public offering finalized in March 2026 successfully replenished working capital sufficient to fund operations through Q1 2027 [N1], mitigating immediate liquidity threats but underscoring dependency on additional financing rounds for sustained development activities.

Preserving Nasdaq listing is strategically important both for institutional investor accessibility and maintaining secondary market liquidity essential for future capital raises [S16], though uncertainty remains around ultimate compliance status — an existential risk that permeates planning.

Clinical Development Roadmap: Upcoming Trials and Regulatory Interactions

Following FDA feedback on earlier trial results for brilaroxazine targeting schizophrenia treatment, Reviva plans initiation of RECOVER-2—a recommended second pivotal Phase 3 trial intended to bolster confirmatory efficacy evidence required for NDA submission approval consideration [S11], [N1].

Regulatory communications have explicitly emphasized generating comprehensive safety/efficacy datasets encompassing acute symptom control alongside maintenance-phase benefits—both critical endpoints in chronic neuropsychiatric disorder treatments where relapse prevention commands premium market valuation multiples.

While exact trial start dates remain subject to sequencing approvals influenced by capital availability and operational readiness assessments, de-risking via FDA engagement reduces binary outcome uncertainty relative to earlier stages but does not fully eliminate usual biotech timeline variability risks typical within extended clinical development pathways [S11], [S3].

Management's expressed intent centers on expedited initiation of RECOVER-2 followed by timely NDA filing contingent upon positive completion outcomes—events constituting key catalysts warranting close investor scrutiny despite intrinsic clinical and regulatory execution uncertainty.

Cash Flow and Capital Allocation: Navigating an Extended Runway

Reviva held approximately $14.4 million cash and equivalents as of the end of FY2025 providing an operational runway into early calendar year 2027 given prevailing burn rates from ongoing R&D intensity centered on brilaroxazine's late-stage clinical programs [F1], [S17], [N1].

Notwithstanding this cushion enabled by recent equity raise completion, operating cash flows continue materially negative at nearly -$24.6 million annually consistent with aggressive trial expenditures impacting financial sustainability without further funding infusions [F1]. The absence of dividends or share buybacks aligns logically given the company's life-cycle stage prioritizing resource allocation toward pipeline advancement over returns distribution [S10], [S12].

Capital allocation reflects prioritization toward patent maintenance costs, personnel expansion tailored for clinical development expertise acquisition, technology infrastructure investments supporting regulatory submission preparations alongside post-trial commercialization readiness contingencies [S4], [S20].

Liquidity management remains delicate given variability inherent in trial cost escalations and potential unforeseen expenses requiring dynamic capital strategy adjustments incorporating potential future offerings or partnerships as conditions evolve.

Risks to Watch: Delisting Threats and Funding Dependencies

A paramount risk facing Reviva derives from potential delisting from Nasdaq triggered by failure to maintain the minimum required trading price—a scenario that could drastically reduce stock liquidity, impair investor confidence, curtail capital access avenues, and hinder long-term corporate viability if unmitigated [S2], [S8], [S14].

While board-approved reverse stock splits provide a tactical lever mitigating immediate compliance threats temporarily through March-end extensions granted by Nasdaq’s Hearings Panel proceedings, permanent resolution hinges on sustainable trading price recovery supported by demonstrable clinical progress or strategic transactions enhancing shareholder value perception [S16], [S21].

Additional operational risks from potential regulatory delays induced by external factors such as government shutdowns affecting FDA review capacity or protracted patent disputes compound uncertainties enveloping timeline adherence critical for value realization trajectories discussed previously ([S9]).

Failure to secure additional financing adequate for pipeline progression threatens required trial initiation timing creating cascading effects delaying NDA submissions risking increased burn without commensurate milestones achieved—a classic catch-22 scenario within biopharmaceutical development cycles necessitating calibrated balancing acts by management.

Disclosure: This analysis utilizes information solely derived from publicly filed SEC documents ([F1], [S#]) and credible news sources ([N#]). All forward-looking observations are qualified based on available data as of the report date without speculative extrapolation beyond provided disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments